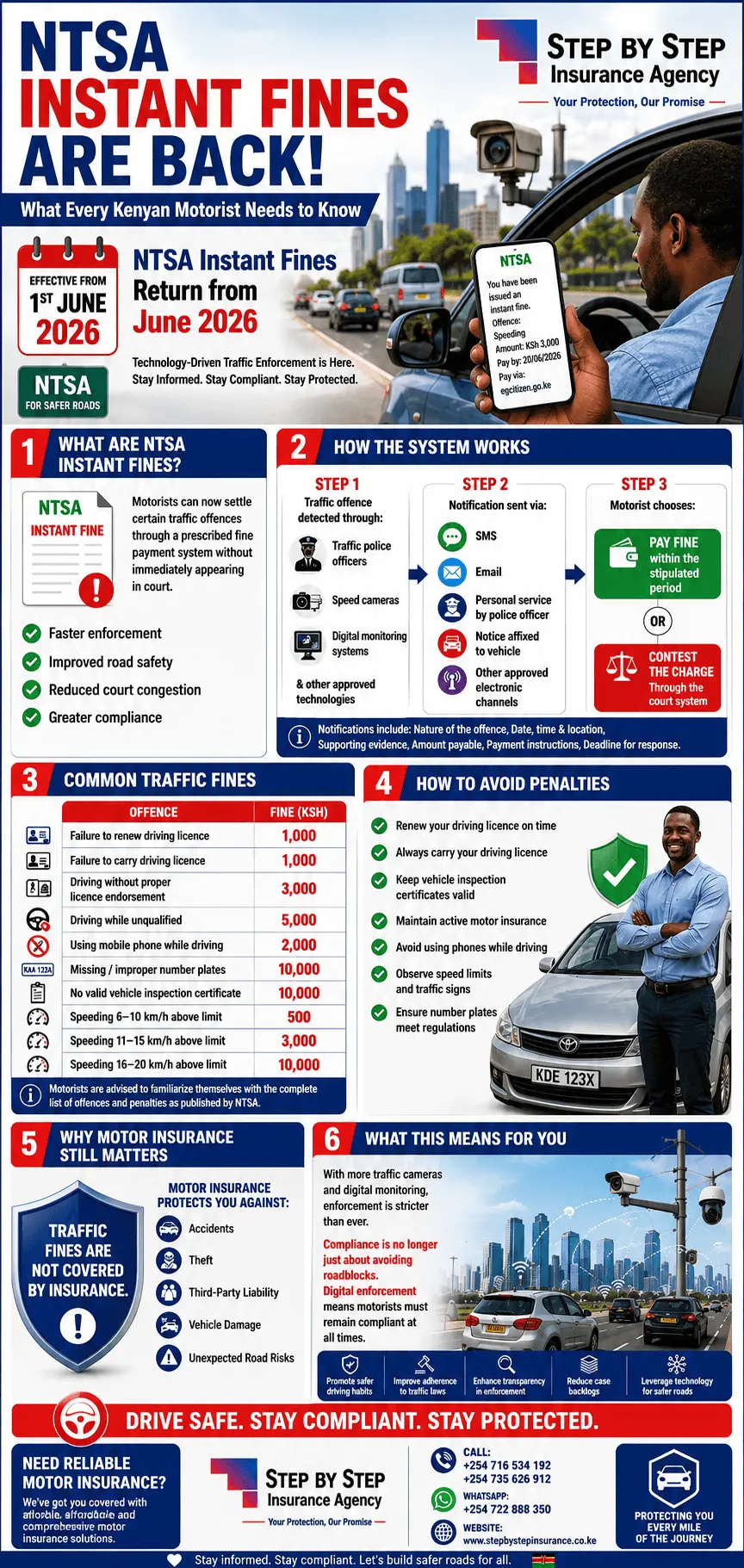

NTSA Instant Fines Are Back: What Every Kenyan Motorist Needs to Know

The National Transport and Safety Authority (NTSA) has reintroduced the Instant Traffic Offences and Fines System, marking a significant shift in how minor traffic offences are handled in Kenya. Effective from 1st June 2026, motorists who commit certain traffic violations may no longer be required to appear in court immediately. Instead, they can settle prescribed fines through a streamlined notification and payment process.

Stay informed with the latest insurance news, industry trends, and regulatory updates in Kenya — straight to your phone. Join a growing community of people who care about staying protected and making smart insurance decisions.

Instant fines are monetary penalties issued for specific traffic offences. The system allows motorists to admit liability and pay a prescribed fine without undergoing lengthy court processes for minor offences.

The initiative aims to enhance road safety, improve compliance with traffic regulations, and reduce congestion in traffic courts. According to Business Daily Africa, motorists will still retain the option to contest fines through the court system should they dispute a charge.

📷 How Does the System Work?

Traffic offences may be detected through a variety of methods:

🚶 Detection Methods

Traffic police officers on patrol

Speed cameras and automated traffic monitoring systems

Other approved digital enforcement technologies

📩 How You Will Be Notified

Once an offence is detected, the motorist may receive a notification through:

SMS

Email

Personal service by a police officer

A notice affixed to the vehicle

Other approved electronic communication channels

📌 What the Notification Includes:

The nature of the offence

Date, time, and location of the offence

Supporting evidence where available

Amount payable and payment instructions

Deadline for response

As reported by Kenyans.co.ke, the system is designed specifically to handle minor offences efficiently, reducing the burden on both motorists and the courts.

⚖️ What Are Your Options?

Upon receiving a notification, a motorist can take one of two paths:

✅ Option 1: Pay the Fine

If the motorist accepts responsibility, they can pay the prescribed fine within the stipulated period through the designated payment channels. This resolves the matter without a court appearance.

⚖️ Option 2: Contest the Charge

If the motorist believes the offence was wrongly issued, they have the right to challenge it through the court system and request access to supporting evidence. It is important to act within the stated response window to protect this right.

💷 Examples of Common Traffic Fines

Below are some of the commonly publicized fines under the system. Motorists are advised to familiarize themselves with the complete published list from the relevant authorities:

⚠️ Offence

💷 Fine (KSh)

Failure to renew driving licence

1,000

Failure to carry driving licence

1,000

Driving without proper licence endorsement

3,000

Driving while unqualified

5,000

Using a mobile phone while driving

2,000

Missing or improper number plates

10,000

No valid vehicle inspection certificate

10,000

Speeding 6–10 km/h above the limit

500

Speeding 11–15 km/h above the limit

3,000

Speeding 16–20 km/h above the limit

10,000

🌟 Benefits of the New System

The government and NTSA expect the system to deliver tangible improvements in road safety and enforcement efficiency:

✅ Promote safer driving habits across Kenya

✅ Improve adherence to traffic laws

✅ Enhance transparency in enforcement processes

✅ Reduce case backlogs in traffic courts

✅ Leverage technology to improve road safety outcomes

🚘 What This Means for Motorists

With increased use of traffic cameras and digital monitoring, motorists should expect stricter and more consistent enforcement of traffic regulations. Compliance is no longer just about avoiding roadblocks — it is about ensuring your vehicle, documents, and driving habits meet legal requirements at all times.

Understanding the connection between traffic compliance and your insurance standing is equally important. Read our article on the 7 benefits of the NTSA e-Logbook for car insurance in Kenya to see how digital documentation now plays a central role in your overall compliance picture.

📋 Tips for Staying Compliant

Avoiding penalties under the new system comes down to consistent, proactive compliance. Here are the key actions every motorist should take:

📄 Ensure your driving licence is valid and renewed on time.

📄 Always carry your driving licence when driving.

🚗 Keep vehicle inspection certificates up to date.

🛡️ Verify that your motor insurance policy is active.

📵 Avoid using mobile phones while driving.

🚲 Observe all speed limits and traffic signs.

🚗 Ensure your vehicle registration plates comply with regulations.

For a deeper look at how NTSA’s digital systems interlink with your driving and insurance records, see our comprehensive NTSA e-Logbooks Kenya 2026 guide.

🛡️ The Role of Motor Insurance

While traffic fines cannot be covered by insurance, maintaining a valid motor insurance policy remains a legal requirement and an essential financial protection tool. Comprehensive motor insurance can protect you against:

Accidental damage to your vehicle

Theft and attempted theft

Third-party liabilities

Other unforeseen risks on the road

📌 Important Reminder: Driving without valid motor insurance is itself a traffic offence and can attract fines under the new system. Ensure your policy is always in force and your cover document is current.

At Step by Step Insurance Agency, we are committed to helping motorists stay protected through reliable and affordable motor insurance solutions. Whether you drive a private saloon, a commercial vehicle, or manage a fleet, we have the right cover for you.

🚗 Ensure Your Motor Cover Is Up to Date

Don’t let an expired or inadequate policy add to your compliance challenges. Get a quick, no-obligation motor insurance quote today.

The return of NTSA instant fines signals a new era of technology-driven traffic enforcement in Kenya. Whether you are a private motorist, commercial driver, or fleet owner, understanding the rules and staying compliant will help you avoid unnecessary penalties and contribute to safer roads for everyone.

For professional advice on motor insurance and risk management, contact Step by Step Insurance Agency today. Our team is ready to help you stay protected every mile of the journey.

How the NTSA e-Logbook Will Affect Your Car Insurance in Kenya (2026)

Kenya’s motor vehicle landscape is undergoing its most significant transformation in decades. On June 10, 2026, the National Transport and Safety Authority (NTSA) officially phases out physical paper logbooks and replaces them with digital e-Logbooks — a move that will ripple far beyond vehicle registration. If you own a car in Kenya, you need to understand exactly how this shift affects your car insurance: from how insurers verify your vehicle, to how quickly your policy gets processed, to what happens if you’re stopped at a police roadblock.

This guide breaks it all down in plain language.

Key Takeaways

The NTSA e-Logbook launches June 10, 2026, replacing physical paper logbooks via the eCitizen platform.

Insurers will verify your vehicle instantly via QR code — eliminating reliance on paper documents that are easy to forge.

Automated reminders will notify you before your insurance lapses, directly through your eCitizen account.

Traffic police will have live access to insurance validity and ownership records at every roadblock.

Ownership transfers will now happen entirely online — removing grey periods that previously caused insurance complications.

Reduced fraud industry-wide could lead to more competitive premiums for honest motorists over time.

Action required before June 10: verify your eCitizen account, update contact details, and confirm your insurance is correctly registered.

💬 Stay Ahead of Insurance News in Kenya

Join our WhatsApp community of Kenyan motorists, brokers, and insurance enthusiasts. We share the latest insurance industry updates, regulatory changes, tips, and market news — no spam, no clickbait.

The NTSA e-Logbook is a fully digital vehicle registration certificate that replaces the traditional paper logbook Kenyan motorists have relied on for decades. Accessible through the government’s eCitizen platform, it stores all vehicle ownership records in a secure, real-time digital database.

NTSA Director General Eng. Nashon Kondiwa announced the rollout during the 3rd Annual Regulatory Authorities and Agencies Conference at South Eastern Kenya University in May 2026, describing it as a shift from “a reactive, paper-based registry that is prone to fraud, delays, and errors” to “a proactive, real-time digital system with strong integrity controls and automated lifecycle management.”

In simple terms: your vehicle’s ownership history, inspection records, insurance validity, and transfer details will all live in one secure, instantly accessible digital record — and your insurer, your bank, and the traffic police will be able to read it with a single scan.

June 10

2026 Rollout Date

100%

Digital & Paperless

Real-Time

Insurer Verification

*352#

Verify Insurance USSD

7 Key Ways the NTSA e-Logbook Affects Your Car Insurance in Kenya

1. 🔍 Insurers Can Now Verify Your Vehicle in Seconds

One of the most direct impacts on car insurance is the speed and accuracy of vehicle verification. Under the old system, insurance underwriters had to rely on physical logbooks — documents that were frequently forged, damaged, or out of date. This created significant fraud risk for insurance companies, delays during the underwriting process, and ultimately higher premiums for honest policyholders.

The e-Logbook changes this fundamentally. Each digital certificate contains a dynamic QR code embedded with encrypted vehicle data. Insurance companies can scan this QR code to instantly confirm:

The registered owner’s identity

Whether the vehicle has any active liens or financing encumbrances

The vehicle’s inspection history

Any previous insurance claims or stolen vehicle flags

NTSA has confirmed that “buyers, insurers, and financial institutions can scan to verify authenticity and ownership instantly.” For you as a policyholder, this means less paperwork when taking out a new policy, faster claim processing, and — over time — potentially lower premiums as insurers gain confidence in the data they are working with.

2. 🔔 Automated Insurance Renewal Reminders

Driving an uninsured vehicle in Kenya is both illegal and financially devastating if you are involved in an accident. Yet thousands of Kenyan motorists find themselves lapsing on insurance renewal — often simply because they forgot or didn’t receive a timely reminder.

The e-Logbook system directly addresses this through automated alerts. NTSA has confirmed that the platform will send vehicle owners timely notifications before their insurance coverage expires, alongside reminders for inspection deadlines and other compliance requirements. The Star reported that “vehicle owners will receive notifications for insurance renewals, inspection deadlines and other compliance requirements,” with NTSA framing this as a tool to “help motorists remain compliant and reduce cases of uninsured or unroadworthy vehicles on Kenyan roads.”

⚡ What this means for you: Set up your eCitizen account and ensure your contact details — phone number and email address — are current. These automated reminders will be delivered through the platform, so an outdated contact means you may miss them.

3. 🚔 Real-Time Insurance Validity Checks at Roadblocks

Currently, traffic police officers rely on physical insurance stickers on windscreens and paper certificates to verify a vehicle’s insurance status at roadblocks. Fake insurance documents have been a persistent problem in Kenya, with some motorists purchasing fraudulent certificates from informal brokers.

Under the e-Logbook system, this loophole closes significantly. NTSA has confirmed that “police and inspection units will have live access to vehicle ownership records, insurance validity, stolen vehicle status and inspection history.” An officer will be able to scan your e-Logbook QR code on a smartphone or connected device and see, in real time, whether your insurance is valid — not just whether you have a sticker on your windscreen.

⚠️ Practical implication: If you purchased insurance through an unregistered broker or have a fraudulent policy, you are at serious risk of being flagged at any roadblock. This is the moment to confirm with your insurer that your policy is registered with the Insurance Regulatory Authority (IRA) and visible in the national insurance database. You can currently verify your motor insurance validity using the USSD code *352#, the AKI app, or the Bima Yangu app.

4. 📋 Faster and More Secure Claims Processing

Filing a car insurance claim in Kenya has traditionally involved a mountain of paperwork: submitting certified copies of your logbook, police abstracts, and ownership documents — all to confirm that the vehicle being claimed for is genuinely yours. Any mismatch between documents could stall or derail your claim entirely. If you’ve experienced this before, our guide on why motor insurance claims delay in Kenya explains the structural reasons behind it.

With the e-Logbook, your ownership record is immutable and real-time. An insurance assessor processing your claim can access the NTSA system directly to confirm vehicle details without waiting for physical documents. This should significantly reduce the time between filing a claim and receiving a payout — a persistent complaint among Kenyan motorists.

Additionally, the encrypted nature of the e-Logbook makes it much harder for fraudsters to submit claims for vehicles they do not own. This reduction in insurance fraud is expected to have a long-term downward pressure on premiums across the market.

5. 🏦 Comprehensive Cover and Logbook Financing — A Cleaner Connection

Many Kenyan motorists use their logbook as collateral to access vehicle financing through banks and SACCOs. Under the old system, lenders had to call NTSA, visit offices, or rely on physical copies to confirm that a logbook was genuine and unencumbered. This process was slow and sometimes manipulated, with some borrowers pledging the same vehicle to multiple lenders simultaneously.

NTSA has directly addressed this: “Banks and SACCOs can directly verify ownership and lien status via the NTSA system, reducing the need for physical file copies and speeding up loan approvals for vehicle financing.” For motorists with comprehensive insurance policies — which many lenders require as a condition for vehicle financing — this integration means lenders can verify both your ownership and your insurance cover through a single digital channel.

📌 If you are currently servicing a car loan: your lender will have much clearer visibility into your vehicle’s status. Lapses in comprehensive insurance (often required under loan agreements) will be more immediately visible to your financing institution, potentially triggering earlier intervention.

Insurance fraud in Kenya has long been a costly problem. Fake logbooks enabled criminals to insure stolen vehicles, submit inflated claims, or take out policies against vehicles they did not legally own. This cost had to be absorbed somewhere — and it ended up in higher premiums for every policyholder in the market.

The e-Logbook system’s digital encryption and secure hashing technology make document forgery dramatically more difficult. NTSA has stated that “the e-Logbook system uses digital encryption and secure hashing technology to protect vehicle owners from forgery and fraud commonly associated with paper documents.”

As fraud-related losses decline across the insurance industry, insurers will have less reason to inflate premiums to cover these losses. While premium reductions are not guaranteed or immediate, the structural conditions that kept them artificially high will begin to change. Motor vehicle insurers in Kenya who adopt the e-Logbook verification system into their underwriting processes will be able to price risk more accurately — rewarding clean, verifiable vehicle histories with more competitive rates. Learn more about how the IRA regulates motor insurance pricing in Kenya.

7. 🔄 What Happens to Your Insurance When Ownership Transfers

Buying or selling a second-hand car in Kenya has always come with insurance complications. If you buy a vehicle and the ownership transfer takes weeks to process, there is a grey period during which the insurance policy is technically under the previous owner’s name. This creates genuine risk for the new buyer.

The e-Logbook eliminates this ambiguity. Ownership transfers will now be completed entirely online via the eCitizen platform, with no need to visit NTSA offices or wait for manual stamping. Ownership records update in real time the moment a transfer is accepted. This means:

New buyers can immediately apply for insurance in their own name

There is no grey period of uncertain ownership

Insurers can confirm the new owner’s status instantly before issuing a policy

If you are currently in the process of buying or selling a vehicle, ensure both parties complete the eCitizen transfer process before the June 10 rollout so your insurance records align with the new digital system from day one.

Step-by-Step: What You Need to Do Before June 10, 2026

Here is a practical checklist for every Kenyan car owner to ensure your insurance situation is clean under the new e-Logbook system:

Access Your eCitizen Account

Log in at ecitizen.go.ke and confirm your vehicle appears under your profile. If you have never set up an eCitizen account, do so now — this is the gateway to your e-Logbook.

Verify Your Contact Details Are Current

Update your phone number and email on the eCitizen platform. Automated insurance renewal reminders and compliance alerts will be sent to these contacts.

Confirm Your Insurance Is Registered Correctly

Use *352# (USSD), the AKI app, or the Bima Yangu app to verify your current motor insurance policy is registered and showing as genuine in the national database. If it shows invalid or not found, contact your insurer immediately.

Update Your Insurer With the Correct Vehicle Details

Confirm that your insurance certificate reflects the same vehicle details that appear in your NTSA record — registration number, make, model, year, and engine capacity. Any mismatch could create complications during claims processing once insurers begin querying the e-Logbook system.

If You Have Recently Bought or Sold a Vehicle, Complete the Transfer

Incomplete logbook transfers create insurance complications. Ensure the NTSA TIMS transfer process is finalised so insurance records align with actual ownership.

Collect Any Pending Physical Logbooks

NTSA has noted that thousands of logbooks remain uncollected at their offices. If you have applied for a new or replacement logbook, collect it before June 10. Physical logbooks remain valid during the transition period, but you want your records complete before the digital switchover.

Attend or Watch NTSA’s Sensitisation Sessions

NTSA has scheduled public education forums from June 2 to June 4, 2026, conducted virtually. These sessions are designed for motorists, insurers, dealers, and financial institutions. Attend to understand how the system will work in practice.

What About Your Physical Logbook?

A common question among Kenyan motorists is whether they need to discard their existing physical logbooks immediately. NTSA has been clear on this: physical logbooks remain valid registration certificates and should be kept safely during the transition period. They will continue to be used alongside e-Logbooks until the full switchover is complete. In some cases, however, you may be asked to surrender the physical copy during replacement or conversion processes.

For insurance purposes, keep your physical logbook until your insurer explicitly confirms they are operating solely on the e-Logbook verification system.

The Bigger Picture: A Safer, More Transparent Insurance Market

The NTSA e-Logbook is more than a paperwork upgrade. It represents a fundamental shift in how vehicle identity and ownership are established in Kenya — with direct consequences for the entire motor insurance ecosystem.

For insurers, it means access to accurate, tamper-proof vehicle data that they can query in real time. For motorists, it means fewer fraudulent competitors inflating premiums, faster claims processing, and less bureaucratic friction when taking out or renewing a policy. For law enforcement, it means the ability to confirm insurance validity, ownership, and inspection status at any roadblock — removing the last refuge of the fraudulent insurance sticker.

Kenya’s motor insurance market has long been complicated by information asymmetry: insurers not trusting the documents they receive, motorists not trusting the process, and fraudsters exploiting every gap. The e-Logbook, when fully implemented, narrows those gaps substantially.

The transition begins June 10, 2026. The question is not whether it will affect your car insurance — it will. The question is whether you will be prepared.

Frequently Asked Questions

Your existing policy remains valid until its expiry date. However, your insurer will increasingly verify vehicle details through the e-Logbook system when you renew or make changes to your policy. It’s wise to ensure your records are aligned well before renewal.

Contact both NTSA and your insurer immediately to reconcile the records. Mismatches can delay claims processing and cause complications at roadblocks. Don’t wait until you need to make a claim to discover the discrepancy.

Police can flag insurance discrepancies they find through the system. If your insurance appears expired or invalid in the digital database, you may face enforcement action even if you have a physical certificate. Always verify your policy status using *352# or the AKI/Bima Yangu apps.

Visit the nearest NTSA office, the NTSA Help Desk at Huduma Kenya Centres, or email info@ntsa.go.ke. You can also visit ecitizen.go.ke directly and follow the registration steps online.

🚗 Ready for Kenya’s New Digital Vehicle Era?

Need to review or update your motor insurance policy ahead of the e-Logbook rollout? Speak to a licensed insurance advisor today to ensure your cover is correctly registered and compliant.

NTSA E-Logbook Kenya 2026: Complete Guide for Vehicle Owners | Step By Step Insurance

Kenya is officially entering a new era of digital vehicle ownership after the National Transport and Safety Authority (NTSA) announced the rollout of electronic logbooks, commonly known as e-logbooks. The move is expected to transform how vehicle ownership, transfers, financing, and verification are handled across the country. (Citizen Digital )

For many Kenyans, the announcement has raised several questions: Are physical logbooks still valid? How do e-logbooks work? Will vehicle transfers now happen online? What does this mean for motor insurance and car financing?

In this guide, we break down everything Kenyan motorists need to know about NTSA’s new digital logbook system and what it means for vehicle ownership in 2026.

Key Takeaways

Physical logbooks remain valid during the transition — no need to panic or rush.

E-logbooks will be issued through the NTSA/eCitizen platform digitally.

Vehicle transfers, ownership verification, and insurance checks will move online.

The system uses QR codes and digital encryption for secure verification.

The change could significantly reduce vehicle fraud and speed up motor insurance processing.

Vehicle owners should only use official NTSA and eCitizen channels to avoid scams.

Stay informed with the latest insurance trends, industry news, and expert tips — shared directly to your phone. No spam, just value for people who care about staying covered and informed.

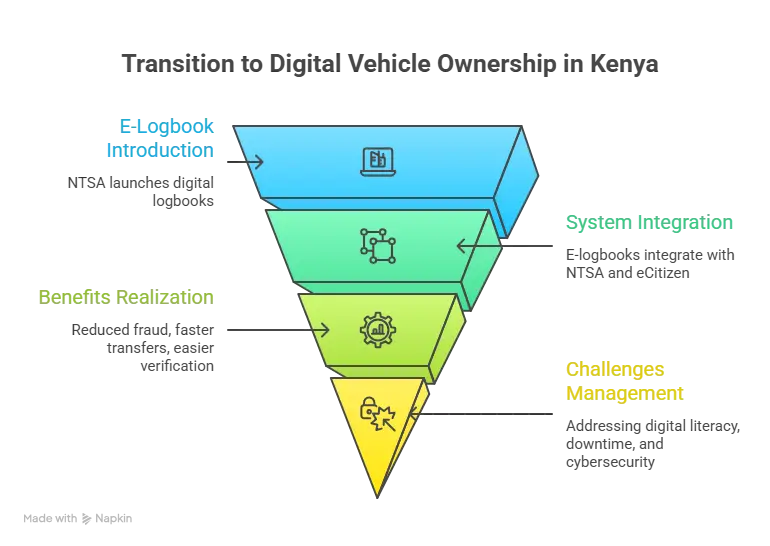

An e-logbook is a digital version of the traditional vehicle logbook issued by NTSA through the eCitizen platform. Instead of relying on a physical paper document, vehicle ownership details will now be stored digitally within NTSA’s system. The new platform is designed to allow real-time verification of vehicle ownership and improve the efficiency of vehicle-related services in Kenya.

According to NTSA, the system aims to:

Reduce fraud and fake logbooks

Improve transparency across the board

Speed up ownership transfers significantly

Improve verification processes for all parties

Digitize motor vehicle records in Kenya

The rollout marks one of Kenya’s biggest transport digitization reforms in recent years and is expected to have wide-reaching effects on vehicle ownership, financing, and the motor insurance sector.

Are Physical Logbooks Still Valid in Kenya?

Yes. Existing physical logbooks are still valid.

NTSA clarified that motorists who already possess physical logbooks should continue using them during the transition period. This means vehicle owners should not panic or rush to replace their current logbooks immediately.

Physical and digital logbooks will coexist temporarily

Vehicle owners should safely keep their current logbooks

Migration to e-logbooks may happen progressively

This clarification came after confusion among motorists who feared physical logbooks would instantly become invalid.

How the New NTSA E-Logbook System Works

The e-logbook system will be integrated into NTSA’s systems and the eCitizen platform. Vehicle ownership information will be stored digitally and can be verified electronically in real time.

The system is expected to include:

Digital encryption for data security

QR code verification for instant authenticity checks

Secure ownership validation protocols

Real-time updates across all connected systems

This will make it easier for buyers, sellers, insurance companies, banks, SACCOs, and law enforcement agencies to confirm vehicle ownership instantly — reducing the room for fraud or manipulation.

Kenya’s transition to digital vehicle ownership — NTSA E-Logbook rollout 2026

Benefits of NTSA E-Logbooks in Kenya

Reduced Vehicle Fraud

Secure QR verification and digital validation make it significantly harder for fraudsters to manipulate vehicle ownership documents or create fake logbooks.

Faster Vehicle Transfers

Transfers may happen entirely online, cutting processing time from days to hours — with no physical paperwork required in many cases.

Easier Insurance Verification

Insurers can verify vehicle ownership, financing status, and registration records in real time — improving policy processing and reducing fraudulent claims.

Better Security for Buyers

Second-hand vehicle buyers can verify ownership, undisclosed loans, and stolen vehicle status before completing any transaction — increasing market trust.

Bank & SACCO Integration

Financial institutions benefit from faster ownership verification, easier lien registration, and better tracking of financed vehicles in their portfolios.

At Step By Step Insurance, we believe digital verification systems could meaningfully improve the overall customer experience when purchasing or renewing motor insurance policies in Kenya.

What Challenges Could Come With the New E-Logbook System?

While the transition offers many advantages, there are still some concerns that vehicle owners and stakeholders should be aware of.

Digital Literacy

Some Kenyans may struggle with online systems, eCitizen navigation, and digital verification — particularly users in areas with limited digital access.

System Downtime

NTSA platforms occasionally experience delays. Heavy reliance on digital systems means service interruptions could temporarily affect transfers or verifications.

Cybersecurity Risks

As ownership records move online, users must avoid fake NTSA websites, use only official platforms, and protect login credentials against scammers.

Warning: Only use official NTSA channels or the eCitizen platform. Scammers may create fake websites to exploit the transition period. Always verify URLs carefully before submitting personal information.

What This Means for Motor Insurance in Kenya

The e-logbook system could significantly reshape Kenya’s insurance industry in several important ways. The digitization of vehicle records aligns well with how modern underwriting practices are evolving in the Kenyan market.

Faster Insurance Processing

Insurance agencies may process motor insurance applications, renewals, and ownership confirmations more efficiently through digital verification — without requiring the physical presentation of documents.

Reduced Fraudulent Claims

Fraudulent ownership claims and fake vehicle records may reduce significantly due to improved verification systems. This could positively impact claims processing, risk assessment, and policy pricing accuracy across the board.

Easier Ownership Confirmation

Motor insurance providers often require proof of ownership before issuing comprehensive cover. The e-logbook system may simplify this verification step considerably.

Looking for Reliable Motor Insurance in Kenya?

Step By Step Insurance offers personalized options for private cars, commercial vehicles, and first-time car owners.

Important Tips for Vehicle Owners During the Transition

As Kenya transitions to e-logbooks, motorists should take the following steps to stay protected and informed.

Keep Your Physical Logbook Safe Your current logbook is still valid unless NTSA officially replaces it. Store it securely just as you would any important ownership document.

Use Official Platforms Only Always use official NTSA channels and the official eCitizen platform. Avoid third-party intermediaries or unofficial apps that claim to process e-logbooks.

Verify Vehicle Ownership Carefully When Buying If purchasing a used vehicle, confirm ownership, verify records, and conduct proper due diligence before making any payment.

Ensure Your Motor Insurance Is Up to Date Digital verification systems may make compliance checks easier. Ensure your insurance policy is active, ownership records are accurate, and vehicle details match NTSA records.

Further Reading: Explore our Comprehensive Motor Insurance Guide in Kenya for detailed guidance on choosing the right cover, understanding policy types, and what documents you need for claims.

Frequently Asked Questions (FAQs)

Is the NTSA e-logbook mandatory?

NTSA is progressively transitioning toward digital logbooks, but existing physical logbooks remain valid during the transition period. The rollout is expected to be gradual rather than immediate.

Can I still use my physical logbook?

Yes. NTSA has confirmed that physical logbooks remain valid for now. Motorists should continue using their current logbooks without panic or urgency to replace them.

Will vehicle transfers now happen online?

Yes. The new system is expected to support online vehicle transfers with significantly faster processing times compared to the traditional physical process.

Can insurance companies verify e-logbooks?

Yes. The system is designed to improve real-time verification capabilities for insurers, banks, SACCOs, and law enforcement agencies — making the process faster and more reliable.

Is the e-logbook safer than the physical logbook?

The digital system introduces enhanced security features such as encryption and QR code verification, which may significantly reduce fraud risks compared to physical documents that can be forged or replicated.

Final Thoughts

NTSA’s transition to e-logbooks represents a major milestone in Kenya’s digital transformation journey. The new system could improve transparency, reduce fraud, speed up transfers, simplify verification, and enhance efficiency across both the insurance and transport sectors.

However, vehicle owners should remain cautious during the transition and continue using official NTSA channels only. As digital vehicle ownership becomes more common in Kenya, having proper and updated motor insurance will remain essential for protecting yourself financially on the road.

At Step By Step Insurance Agency, we continue helping Kenyan motorists choose affordable, reliable, and personalized motor insurance solutions tailored to their needs. Read our full motor insurance guide or get a free quote today.

Why Your Motor Insurance Claim Was Delayed in Kenya (And How to Fix It Fast) | Step by Step Insurance

You’ve been in an accident. The car is damaged. You might be injured. And now your motor insurance claim feels stuck.

If you’re wondering why your claim is taking so long, you’re not alone. Motor claim delays are one of the biggest frustrations for Kenyan drivers — and they happen more often than they should.

The truth? Most delays happen because one step in the process is missed, misunderstood, or slowed down. This guide walks you through how motor claims actually work in Kenya — and, more importantly, how you can fix delays fast.

Are you interested in staying up to date with the latest insurance trends and news in Kenya? Join our WhatsApp group and connect with other Kenyans who are passionate about making smarter insurance decisions. No spam — just genuine, useful insights.

🚗 How Motor Insurance Claims Really Work in Kenya (Step by Step)

Before you can fix a delay, you need to understand the full process. Here is how a standard motor claim works on Kenyan roads:

1

Accident Happens

If the accident occurs on the road, police assess the scene. Your vehicle may be towed to a police station or safe holding yard. Anyone injured is taken to hospital for first aid and treatment.

2

⚡ Call Your Insurance Agent Within 48 Hours

This step is critical. You must notify your insurance agent within 48 hours of the accident. Late reporting can immediately delay — or even risk — your claim. Even if you don’t yet have documents, make the call first. This applies whether you hold comprehensive or third-party cover.

3

Obtain a Police Abstract

You’ll need an official police abstract showing the date and place of the accident, vehicles involved, and basic accident details. Without this document, your claim cannot proceed.

4

Fill the Claim Form & Attach Required Documents

You’ll need to submit: a filled claim form, copy of National ID, valid driving licence, and photos of the accident scene and vehicle damage. Missing even one item pauses your entire claim.

5

Insurance Acknowledges & Assesses the Vehicle

Once documents are received, the insurer acknowledges your claim and appoints an assessor. This assessment determines whether the claim is admissible and how repairs will be handled.

6

Repair Options: Garage Repairs or Cash in Lieu (CIL)

If the claim is admissible, you choose one of two paths:

✅ Option A: Garage Repairs

Your car is referred to an approved garage

Repairs are carried out

The insurer reinspects the vehicle

A release letter is issued

You collect your car — claim complete

✅ Option B: Cash in Lieu (CIL)

You repair the vehicle privately

Submit ETR receipts and repair documents

The insurer processes your refund

Refund timelines: 14–30 working days (varies by underwriter)

Now that you understand the process, here are the most common causes of delays in Kenya:

❌ Late Reporting

Failing to notify your agent within 48 hours raises red flags and slows everything down immediately.

❌ Missing Documents

No police abstract, no claim form, no licence copy — no progress. Claims only move forward when everything is submitted.

❌ Delayed Assessments

If garages or assessors take long to submit their reports, approvals stall with them.

❌ Liability Investigations

When another vehicle is involved, insurers must confirm who caused the accident before approving any repairs.

❌ Outstanding Premiums

If your policy isn’t fully paid, your claim freezes immediately. This is one of the most overlooked causes.

❌ Poor Follow-Up

Many drivers wait quietly instead of checking progress. Active follow-up makes a huge difference.

According to the Insurance Regulatory Authority (IRA) ↗, insurers are expected to settle claims within reasonable timelines once documentation is complete. Understanding these timelines helps you identify when to escalate.

📅 How Long Should Motor Claims Take in Kenya?

These timelines assume all documents are in order and submitted promptly. Use them as a benchmark to measure whether your claim is on track:

📌 Claim Type

⏱ Expected Timeline

Key Condition

Simple vehicle repairs

14–21 working days

Full documents submitted; no liability dispute

Accident claims with liability

21–45 working days

Fault determination may extend the timeline

Cash in Lieu (CIL) refunds

14–30 working days

ETR receipts and repair docs submitted

If your claim is significantly beyond these ranges, it’s time to take action — or ask your broker to escalate on your behalf.

🔧 How to Fix a Delayed Motor Claim Fast

If your claim feels stuck, work through this checklist systematically:

🔍

Confirm exactly what’s pending. Ask directly: “What exact document or approval is holding my claim?” Don’t accept vague answers.

📂

Submit everything at once. Avoid sending documents in pieces. Compile all required items and submit in a single batch.

📅

Follow up every 3–5 working days. Keep your claim reference number and all communication records for escalation.

🤝

Use your insurance agent. A good agent can track assessments, follow up with garages, push approvals, and escalate stalled files. Clients working alone usually struggle to reach the right people.

📣

Escalate when necessary. Ask for written updates or claims supervisors if delays drag on beyond the expected timelines shown above.

🏢 How Step by Step Insurance Helps Speed Up Motor Claims

At Step by Step Insurance, we don’t stop at selling motor cover. We stay with you through the entire claims journey — from the moment of impact to when you’re back on the road.

🚨 Immediate post-accident guidance

📄 Document organisation

📞 Follow-up with insurers and garages

🔎 Assessment tracking

⚡ Delay escalation

📬 Regular progress updates

Instead of chasing insurers yourself, we manage the entire process for you. Our clients don’t sit in the dark — they get answers, updates, and results.

Prevention is always better than cure. Build these habits now to protect yourself if an accident happens:

Call your agent immediately after any accident

Take clear, timestamped photos at the scene

Keep digital copies of all documents

Ensure your premiums are fully paid and up to date

Never repair the vehicle before getting approval

Always consult your agent before making any decisions

For a comprehensive overview of your rights and responsibilities as a motor insurance policyholder in Kenya, see our detailed Motor Insurance Kenya Guide 2026. You can also visit the IRA Kenya official website ↗ for regulator guidelines on claims timelines.

⚡ Need Help With a Delayed Motor Claim?

If your motor claim is stuck — or you’re tired of chasing garages and insurers — let Step by Step Insurance handle it. We’ll guide you from the accident scene to car release or your Cash in Lieu refund, so you can get back on the road sooner.

Third-Party vs Comprehensive Car Insurance in Kenya – A Clear Guide

Car insurance in Kenya isn’t just about complying with the law — it’s about protecting your finances, your vehicle, and your peace of mind.

The Insurance Regulatory Authority (IRA) requires every vehicle on Kenyan roads to have at least Third-Party insurance. But beyond meeting the legal requirement, many drivers find themselves asking:

Should I choose Third-Party only… or invest in Comprehensive cover?

Let’s break it down clearly and simply so you can make a confident, informed decision.

Key Takeaways

Third-Party is the minimum legal requirement and covers damage you cause to others, but not your own vehicle.

Comprehensive covers both third-party liabilities and damage or loss to your own car from accidents, theft, fire, and natural disasters.

The right choice depends on your car’s value, budget, driving habits, and personal risk tolerance.

Professional guidance can help you navigate options and find the most suitable and cost-effective cover for your specific situation.

Are you interested in staying updated on insurance trends, news, and insights in Kenya? Join our dedicated WhatsApp group to connect with a community of like-minded individuals. Share experiences, ask questions, and stay informed.

Third-Party insurance is the minimum legal requirement in Kenya.

✅ What it covers:

Injuries caused to other people

Damage to other people’s vehicles or property

Legal liability arising from an accident

❌ What it does not cover:

Damage to your own vehicle

Theft of your vehicle

Fire or flood damage

Your own medical expenses

In simple terms, Third-Party protects you against claims from others — but it does not protect your own car.

It is a cost-conscious option for drivers who mainly want to meet legal requirements while keeping premiums manageable.

What Is Comprehensive Car Insurance?

Comprehensive insurance provides broader protection. It includes Third-Party cover and also protects your own vehicle.

✅ Typically covers:

Accidental damage to your car (even if you are at fault)

Theft or attempted theft

Fire damage

Natural disasters such as floods or storms

Third-party injuries and property damage

Many Comprehensive policies also allow optional add-ons such as:

Windscreen cover

Roadside assistance

Towing services

Personal accident benefits

In short, Comprehensive cover protects both you and other road users.

Comprehensive vs Third-Party: Quick Comparison

Feature

Third-Party Only

Comprehensive

Legal requirement

Yes

Yes

Covers damage to others

Covers your own car

Theft & fire

Natural disasters

Premium cost

Lower

Higher

Peace of mind

Basic

High

Pros and Cons at a Glance

Third-Party Insurance

Pros

More affordable premiums

Meets legal requirements

Suitable for drivers seeking basic liability protection

Cons

No protection for your own vehicle

Repair costs come out of your pocket

No cover for theft, fire, or natural disasters

Comprehensive Insurance

Pros

Protection for your own vehicle

Covers theft, fire, floods, and accidents

Optional add-ons for additional security

Greater financial protection

Cons

Higher premiums

May not always be cost-effective for very old vehicles

How Do You Decide What’s Right for You?

Choosing between Third-Party and Comprehensive depends on your personal situation. Here are the key factors to consider:

1. Your Car’s Value

If your vehicle is new or has significant market value, Comprehensive cover may offer better financial protection.

If your car has a lower value, Third-Party may be a practical option.

2. Your Budget

If unexpected repair or replacement costs would significantly affect your finances, Comprehensive cover offers added financial security.

3. Your Driving Environment

Frequent driving in busy cities, highways, or high-traffic areas increases the likelihood of accidents. Broader protection may be worth considering.

4. Your Risk Tolerance

Ask yourself: If something happens to my car tomorrow, would I be financially prepared to handle it?

Your answer can guide your decision.

Real-Life Scenarios

New car owner in Nairobi: Comprehensive cover is often recommended due to higher traffic risk and vehicle value.

Older vehicle used occasionally: Third-Party may provide adequate protection while keeping costs low.

Family or business vehicle: Comprehensive cover can offer important financial stability in case of unexpected events.

How Step by Step Insurance Helps You Choose

At Step by Step Insurance, we believe insurance decisions should be informed — not rushed.

Instead of offering one-size-fits-all solutions, we take time to understand:

Your vehicle type and value

Your budget

How and where you drive

Your personal risk level

Here’s how we support you:

We compare multiple insurers to help you get competitive value

We explain policy details in simple, clear language

We help you choose meaningful add-ons — not unnecessary extras

We assist you through the claims process from start to finish

We give honest advice — even when a lower-cost option makes more sense

Our goal is straightforward: to match you with insurance that truly protects you — not just something that looks affordable on paper.

Frequently Asked Questions

Can I upgrade from Third-Party to Comprehensive later?

Yes. In many cases, you can upgrade during renewal or mid-term, subject to vehicle inspection and insurer approval.

Is Comprehensive always better?

Not necessarily. The right choice depends on your vehicle’s value, financial position, and comfort with risk.

Does Third-Party cover passengers?

It may cover third-party passengers, but cover for your own injuries typically requires personal accident benefits, which are usually an add-on or part of a Comprehensive policy.

Final Thoughts

There is no universal “best” car insurance in Kenya.

Third-Party offers legal compliance and basic liability protection. Comprehensive provides broader financial protection and greater peace of mind.

The right choice depends on your car, your budget, and your lifestyle.

If you’re unsure, that’s exactly where professional guidance makes a difference.

Ready to Choose the Right Cover?

Talk to Step by Step Insurance today for a free consultation and personalized quote. We’ll walk with you — step by step — until you’re confidently protected.

Motor Insurance in Kenya (2026): The Complete Step-by-Step Guide

Motor insurance is one of the most essential covers in Kenya. It protects you from major financial loss when your vehicle is involved in an accident, theft, fire, or third-party claim.

But many people buy motor insurance without fully understanding:

what it covers

what it doesn’t cover

how claims work

why excess matters

how insurers calculate payouts

This guide explains everything clearly, step-by-step.

Key Takeaways

Motor insurance in Kenya comes in three main types: Comprehensive, Third Party Fire & Theft, and Third Party Only

Comprehensive cover protects both your vehicle and third-party liabilities, making it ideal for newer or high-value cars

Understanding excess (the amount you pay during claims) is crucial to avoid surprises

Underinsurance can significantly reduce your payout – always insure at market value

Immediate accident reporting and proper documentation are essential for smooth claims processing

Optional add-ons like windscreen cover and excess buyback can provide valuable additional protection

Stay updated with the latest insurance trends, news, and expert insights. Join our WhatsApp community of insurance enthusiasts and professionals in Kenya.

✅ If the vehicle is declared a total loss, the maximum payable is based on the vehicle’s value just before the accident.

B) Market Value (How Your Car Payout Is Calculated)

If your car is written off, the payout is based on your car’s pre-accident market value, not sentimental value.

Tip: Review your value every year so you don’t underinsure.

C) Recovery and Towing (After an Accident)

If your vehicle cannot be driven after an accident, your cover may help pay for:

towing/recovery

moving the vehicle to the nearest repairer

moving the vehicle to a safe place

⚠️ Note: This benefit usually has a limit, so it’s not “unlimited towing.”

D) Small Repairs (Authorized Repair Limit)

Some motor covers allow minor repairs without long approvals—up to a specific limit.

This helps in cases like:

minor bumper repairs

small panel work

small parts replacement

✅ You still must send repair costs quickly to the insurer to avoid claim issues.

4) What Motor Insurance Covers for Third Parties

Even if you don’t have comprehensive, third party cover is essential because it protects you from expensive legal liability.

Third party cover can pay for:

✅ Third Party Bodily Injury/Death

Example: you hit a pedestrian or boda boda rider.

✅ Third Party Property Damage

Example: you hit another car, a gate, a wall, or shop property.

Important: Limits Apply

Many policies have limits such as:

maximum payout per person injured

maximum payout per accident/event

maximum payout for property damage

✅ Always confirm your third party limits when choosing a policy.

5) Emergency Medical Expenses (If Included)

Some motor covers provide a small medical expense benefit for injuries resulting from the accident.

This can cover reasonable emergency medical costs for:

the insured

the authorized driver

passengers (depending on policy wording)

✅ It helps especially for minor emergency treatment after accidents.

6) Car in Garage / Service Provider Custody

If your vehicle is at a garage for repairs or servicing, some policies still protect you under certain conditions.

This is helpful because accidents and loss can happen even when the car is not with you physically.

7) What Motor Insurance Does NOT Cover (Common Exclusions)

Even with comprehensive cover, insurers may not pay for certain events.

Exclusion Type

What It Means

Example

Wear and Tear

Normal deterioration over time

Old tyres wearing out naturally

Mechanical Breakdown

Engine/electrical failure not from accident

Engine failure without collision impact

Consequential Loss

Indirect losses from being unable to use car

Loss of business income while car is off road

Contents Damage

Items inside the vehicle

Laptop, phone, cash stolen from car

Overloading

Carrying excessive weight/passengers

Carrying cargo above vehicle capacity

DUI (Driving Under Influence)

Driving while intoxicated

Accident while driver was drunk

Prohibited Use

Using car for purposes not covered

Uber/Taxi without commercial cover, racing

Common exclusions include:

❌ Wear and tear – Example: old tyres wearing out.

❌ Mechanical or electrical breakdown – Example: engine failure without accident impact.

❌ Consequential loss – Example: loss of business income because your car is off the road.

❌ Damage to contents inside the vehicle – Example: laptop, phone, cash, or goods stolen from the car (unless separately insured).

❌ Overloading or strain – Example: carrying cargo above capacity.

❌ Driving under alcohol/drugs – Insurance may reject claims if the driver was intoxicated.

❌ Using the car for prohibited purposes – Example: hire and reward (Uber/Taxi) if not insured for it, racing, commercial delivery if not covered under limitations.

Important: This is why “limitations as to use” is critical.

8) Excess (Deductible): What You Pay During a Claim

An excess is the amount you contribute when a claim occurs.

Common excess types in motor insurance:

Excess Type

When It Applies

Typical Amount

Own Damage Excess

When your car is damaged

Percentage of value + min/max amounts

Third Party Property Damage Excess

When third party property is damaged

Fixed amount (e.g., Ksh 5,000-15,000)

Theft Excess

When vehicle is stolen

Varies based on security devices installed

Young Driver Excess

Driver under certain age (usually 25)

Additional amount on top of regular excess

Why Excess Matters

You can have a valid claim, but still pay part of the cost because excess applies.

Example:

If repairs cost Ksh 200,000 and your excess is Ksh 15,000

➡️ insurer pays Ksh 185,000 (subject to approval)

9) Underinsurance (Average Clause) — Very Important

If your vehicle market value is higher than what you insured it for, insurers can apply the average clause.

Meaning: ✅ they reduce your payout proportionately because you underinsured the car.

Example (simple):

Your car market value: Ksh 1,000,000

You insured it at: Ksh 500,000

➡️ insurer may pay only about 50% of the repair cost.

Complete Guide to Motor Commercial General Cartage Insurance in Kenya | Step by Step Insurance

Running a transport or logistics business in Kenya is both an opportunity and a challenge. Whether you operate one delivery van or an entire fleet of lorries, you deal with risks every day—accidents, cargo damage, theft, liability claims, breakdowns, and operational delays. These risks can disrupt business continuity or cause financial losses that take years to recover.

That is where Motor Commercial General Cartage insurance comes in. This specialized insurance is designed for vehicles that transport goods on behalf of clients (hire and reward). Unlike private motor insurance, the risks involved in general cartage operations are higher—making tailored coverage essential.

At Step by Step Insurance Agency, we help transporters, logistics companies, SMEs, independent transporters, and corporates secure the right level of protection — ensuring every vehicle on the road has comprehensive, dependable coverage backed by Kenya’s top underwriters.

💡 Key Takeaway

Motor Commercial General Cartage Insurance is essential for any business transporting goods for others in Kenya. It protects against vehicle damage, cargo loss, third-party liabilities, and operational risks that standard insurance doesn’t cover. Partnering with an experienced broker ensures you get coverage tailored to your specific routes, cargo, and risk profile.

Interested in staying updated with the latest insurance trends, news, and insights in Kenya? Join our dedicated WhatsApp group to connect with professionals, business owners, and individuals passionate about insurance matters.

1. Understanding Motor Commercial General Cartage Insurance

What It Is

Motor Commercial General Cartage insurance is a comprehensive policy for vehicles used to transport goods that do not belong to the vehicle owner. This includes:

Delivery vans

Pickups

Light trucks

Medium and heavy commercial trucks

Lorries used for courier or distribution work

Corporate vehicles used to transport client goods

This insurance class is specifically tailored for general cargo movement, which exposes vehicles to frequent stops, heavy loads, long-distance routes, and unpredictable roads.

Who Needs It

You need this cover if you operate:

A courier company

A logistics or distribution company

A moving company

A fleet offering transport services to clients

An independent transporter

A business that delivers products to customers using company vehicles

In short, if you transport goods for someone else — you need Motor Commercial General Cartage insurance.

2. Why Motor Commercial General Cartage Insurance Is Essential

Transporting goods exposes your business to a range of risks. Every kilometre travelled comes with potential hazards. The right insurance protects your business from:

⚠️ Risk Category

🛡️ How Insurance Protects You

1. Financial Losses Road accidents can cause damage worth hundreds of thousands of shillings

2. Legal Liabilities Injury to people or damage to third-party property

Handles compensation claims and legal expenses

3. Cargo Damage Risks Goods damaged in transit due to accidents, fire, or theft

Compensates for client goods, maintaining business relationships

4. Operational Downtime Vehicle breakdowns or accidents causing delays

Provides towing, recovery, and alternative transport support

5. Compliance Requirements Kenyan law requires commercial vehicles to be insured

Ensures legal compliance, avoiding fines and penalties

6. Business Continuity Unexpected incidents disrupting operations

Keeps your business running through financial protection

3. Core Benefits of Motor Commercial General Cartage Insurance

Motor Commercial General Cartage insurance provides several layers of protection. Here is a breakdown of what you typically get:

A. Protection Against Vehicle Damage

This covers:

Accidental damage

Collision damage

Damage from overturning

Damage during loading/unloading

Fire-related damage

Theft or attempted theft

Vandalism

Commercial vehicles are constantly on the move, often under high operational strain. Having an insurance plan that covers accidental and non-accidental damage gives peace of mind and ensures fast recovery after unexpected incidents.

B. Third-Party Liability Cover

This is one of the most critical components. It covers:

Bodily injury to third parties

Death

Damage to third-party property

For example: If your truck hits another vehicle, damages a perimeter wall, or injures someone, the liability is handled through your insurance.

C. Liability for Goods (Cargo)

Cargo liability ensures that if goods you are transporting on behalf of clients are lost or damaged due to insured risks, compensation is provided. This builds customer trust and protects you from costly disputes.

D. Cover for Accessories and Spare Parts

Vehicles may have:

Tracking devices

Tarpaulins

Customized storage equipment

Additional lighting

Reinforced bodies

These are expensive. Good commercial policies include cover for these accessories.

E. Towing, Recovery, and Emergency Assistance

Commercial vehicles often operate far from urban centers. Towing and recovery services ensure the vehicle is safely brought to a garage or secure location when needed.

F. Medical Expenses for Driver and Crew

In case of an accident, policies may cover emergency medical expenses for the driver and loader/assistant — minimizing financial strain.

4. What Motor Commercial General Cartage Insurance Does Not Cover

Understanding exclusions helps you avoid surprises at claim time. Common exclusions include:

🚫 Exclusion

💡 Recommendation

Mechanical breakdown or wear and tear

Consider separate mechanical breakdown cover

Damage caused by intoxicated driving

Implement strict driver sobriety policies

Using the vehicle outside declared use

Always update insurer on any change of use

Overloading

Adhere to manufacturer’s weight limits

Loss caused by unlicensed drivers

Verify all driver licenses regularly

Unapproved modifications

Get insurer approval before modifications

Avoiding these risks ensures smooth claims and policy validity.

5. Why Choosing a Broker Matters — The Step by Step Advantage

Insurance policies can be complicated, but working with Step by Step Insurance Agency simplifies everything. As a trusted, experienced broker in Kenya, we deliver the following key benefits:

A. Personalized Advisory

No two businesses operate the same way. We take time to understand:

The nature of your cargo

Routes you cover

Number and type of vehicles

Your risk exposure

Your budget

We then match you with the most suitable policy options.

B. Access to Policies From Kenya’s Leading Underwriters

Instead of being limited to one insurer’s terms, we give you access to a wider selection of top-rated underwriters. This gives you:

✅ Advantage

📊 Benefit to Your Business

Competitive pricing

Lower premiums without compromising coverage

Better cover limits

Higher protection limits for cargo and liability

More options for add-ons

Customizable coverage for specific needs

Improved claims handling

Faster claim processing with reputable insurers

Better value for money

Optimal coverage per shilling spent

C. Fast, Hassle-Free Insurance Processing

We assist you at every step:

Document preparation

Vehicle valuation (where needed)

Policy issuance

Endorsements

Renewal reminders

Our goal is to ensure you are always covered — without delays or lapses.

D. Claims Support and Follow-Up

Filing and following up on claims can be stressful. We handle:

Claim initiation

Documentation guidance

Coordination with assessors

Follow-up with the insurer

Ensuring you get fair compensation

This is one of our strongest value propositions because our clients never navigate claims alone.

6. The Step-by-Step Process of Getting Motor Commercial General Cartage Insurance

The process is simple, structured, and efficient.

🔄 Step

📝 Actions

⏱️ Timeline

Step 1: Share Vehicle Details

Provide vehicle type, tonnage, usage, cargo type, driver details, routes

1-2 hours

Step 2: Submit Documentation

Logbook, company registration, driver licenses, KRA PIN, ID copies

1 day

Step 3: Receive Tailored Quotes

Compare multiple options, coverage details, premiums, and add-ons

1-2 days

Step 4: Payment & Policy Issuance

Complete payment, receive certificate and policy documents

24 hours

Step 5: Renewal & Continuous Support

Get renewal reminders, policy reviews, and ongoing claims support

Ongoing

7. Key Considerations When Choosing a Motor Commercial General Cartage Insurance Policy

To ensure you get the right cover, think about:

Type of Cargo You Transport – Fragile or high-value goods require expanded cargo liability cover.

Driver Experience and Training – Experienced drivers = lower risk and potentially lower premiums.

Route Risk Exposure – Urban routes differ from long-distance or rural routes. Insurance needs shift accordingly.

Frequency of Use – High-frequency vehicles need comprehensive protection.

Vehicle Value and Condition – Newer vehicles may need broader cover; older ones may require specific endorsements.

Budget vs. Risk Appetite – Balance affordability with sufficient coverage to avoid underinsurance.

8. Why Step by Step Insurance Is Your Trusted Partner

We have built our name on:

Professionalism

Customer-first service

Fast processing

Expert policy interpretation

Long-term client relationships

Our clients include:

🏢 Client Type

🛡️ Insurance Solutions Provided

SMEs

Cost-effective, essential coverage for growing businesses

Large logistics companies

Fleet policies with centralized management

Manufacturing distributors

Goods-in-transit focused coverage

Fleet owners

Bulk discount arrangements

Independent transporters

Flexible, single-vehicle policies

Corporate delivery departments

Integrated risk management solutions

We help each one find the right Motor Commercial General Cartage insurance based on individual needs.

9. Our Commitment: Partnering With Kenya’s Best Underwriters for Tailored Solutions

At Step by Step Insurance Agency, we collaborate with Kenya’s top underwriters — ensuring you receive the best, most reliable, and most competitively-priced insurance solutions.

We do all the heavy lifting:

Comparing quotes

Reviewing coverage options

Explaining complex terms

Recommending the best value

Handling documentation

Supporting claims

Our partnerships allow us to tailor insurance solutions that align exactly with your business requirements.

10. How to Get Started — Contact Us Today

Secure your fleet. Protect your cargo. Safeguard your business.

📞 Get Your Tailored Insurance Solution

Ready to protect your transport business with comprehensive Motor Commercial General Cartage Insurance? Our team is here to guide you through every step.

Motor Commercial General Cartage insurance isn’t just a requirement — it’s a strategic investment that protects your business, strengthens trust with clients, and ensures consistent operations. With the rising risks in transport and logistics, having tailored, reliable coverage is essential.

By partnering with Step by Step Insurance Agency, you gain:

Tailored policies

Professional guidance

Access to Kenya’s best underwriters

Strong claims support

Long-term protection

Your business deserves more than a generic policy — it deserves a trusted insurance partner who understands your operations and provides customized solutions built for real-world challenges.

Let’s protect your journey, your cargo, and your future — step by step.

Private Motor Insurance in Kenya: Complete Step-by-Step Guide | Step by Step Insurance

Owning a private vehicle in Kenya goes beyond driving convenience — it’s a commitment to safety, compliance, and financial security. The right motor insurance ensures that when accidents, theft, or damage occur, you’re not alone in handling the costs. With guidance from Step by Step Insurance Agency, you can navigate the process confidently — securing tailored coverage that fits your needs, lifestyle, and budget.

📋 Key Takeaways

Motor insurance is legally mandatory in Kenya under the Insurance Act

Three main types: Third-Party Only, Third-Party Fire & Theft, and Comprehensive

Premium costs depend on vehicle value, usage, claim history, and add-ons selected

Step by Step Insurance partners with AA Kenya for enhanced roadside assistance

Expert guidance ensures you get the right coverage without overpaying

Driving without insurance in Kenya is illegal. According to the Insurance (Motor Vehicles Third Party Risks) Act (Cap 405), every vehicle owner must have at least Third-Party Liability Cover to operate legally on public roads. But compliance isn’t the only reason. Insurance is your financial shield — protecting you, your car, and others in case of accidents, fire, or theft.

Reason

Why It Matters

Legal Requirement

Mandatory under Cap 405 Laws of Kenya

Financial Security

Covers losses from accidents, theft, or fire

Third-Party Protection

Pays for injuries or property damage caused to others

Peace of Mind

Lets you drive confidently knowing you’re protected

Choosing the right plan means balancing legal compliance with real-world protection — and that’s where expert guidance comes in.

II. Step 1: Understand the Three Types of Motor Insurance

Private motor insurance in Kenya comes in three main types. The coverage you choose determines your level of protection and premium cost.

1. Third-Party Only (TPO)

Minimum legal requirement for driving in Kenya.

Covers: Injury, death, or property damage caused to third parties.

Does Not Cover: Damage to your own car, theft or fire, accidental damage.

Feature

Covered by TPO?

Third-Party Liability

Yes

Theft or Fire Damage

No

Accidental Damage (Own Car)

No

Legal Driving Requirement

Yes

Best for: Owners of older or low-value vehicles who want to meet legal requirements at minimal cost.

2. Third-Party, Fire & Theft (TPFT)

An upgraded version of TPO that includes additional protection.

Covers: All TPO benefits, loss or damage due to theft, attempted theft, or fire.

Does Not Cover: Accidental or collision damage to your own car.

Feature

Covered by TPFT?

Third-Party Liability

Yes

Theft or Fire Damage

Yes

Accidental Damage (Own Car)

No

Legal Requirement

Yes

Best for: Drivers seeking more protection than TPO offers, especially in high-risk theft areas.

3. Comprehensive Cover

The most complete and recommended form of protection.

Covers: All TPFT and TPO benefits, accidental damage to your own vehicle, natural disasters (floods, storms, earthquakes), malicious damage and vandalism.

Feature

Covered by Comprehensive?

Third-Party Liability

Yes

Theft or Fire Damage

Yes

Accidental Damage (Own Car)

Yes

Natural Disasters & Vandalism

Yes

Personal Accident Benefits

Optional

Best for: Newer or higher-value vehicles and anyone who relies on their car for work or family use.

III. Step 2: Explore Additional Features and Add-Ons

A strong policy doesn’t stop at basic protection. Comprehensive plans often include built-in benefits and optional add-ons that enhance convenience and value.

Built-In Benefits

Benefit

Description

Accidental Damage

Covers repair or replacement costs for your car after a collision.

Theft & Fire

Compensates you if your car is stolen or damaged by fire.

Third-Party Liability

Covers injury or property damage to others.

Emergency Medical Expenses

Covers reasonable medical costs after an accident.

Towing & Roadside Assistance

Pays for towing if your car breaks down or is involved in an accident.

Windscreen Cover

Covers repair or replacement of broken windscreens.

In-Car Entertainment System

Provides protection for audio, video, and navigation systems installed in your vehicle. Some insurers offer this as part of comprehensive cover or as an add-on for high-end entertainment systems.

Optional Add-Ons

Add-On

Purpose / Benefit

Excess Protector

Waives or reduces the amount you pay out-of-pocket per claim.

Loss of Use / Courtesy Car

Provides compensation or a temporary car while yours is under repair.

Political Violence & Terrorism (PVT)

Extends cover to include riots, strikes, or terrorism-related damage.

Personal Accident Cover

Offers compensation for death or disability of the driver and passengers.

These features turn a standard policy into a customized protection plan, tailored to your lifestyle and risk exposure.

IV. Step 3: Understand What Affects Your Premium

Insurance premiums are based on risk assessment. Knowing what influences your cost helps you plan better and avoid surprises.

Factor

Impact on Premium

Vehicle Value, Make, and Model

High-value or rare vehicles attract higher premiums.

Vehicle Age

Older cars may have higher repair costs or limited coverage.

Usage Type

Private-use vehicles cost less to insure than commercial ones.

Claim History

Frequent past claims can raise your premium.

Add-Ons Selected

Each optional feature increases the premium slightly.

Excess Amount

Higher excess lowers the premium but increases your payment during a claim.

Tip: A trusted agent can help you balance premium costs with coverage needs — ensuring you don’t overpay or underinsure.

V. Step 4: Our Partnership with AA Kenya for Enhanced Road Safety

At Step by Step Insurance Agency, we’re committed to keeping our clients safe on and off the road. That’s why we’ve partnered with AA Kenya, the country’s most trusted roadside assistance provider, to offer our clients exclusive rescue and towing benefits.

Key Road Rescue Benefits

Service

Description

24/7 Availability

Road rescue services are available around the clock, every day of the year.

Emergency Roadside Assistance

Includes jump-starting dead batteries, tyre changes, fuel delivery (fuel cost excluded), key retrieval, and minor repairs.

Towing Services

If the vehicle cannot be fixed on the spot, it’s towed safely to a repair shop.

Free Towing

Members receive a set free towing distance (e.g., Signature: 10 km, Classic: 40 km).

Discounted Rates

Reduced towing and recovery fees for longer distances or accident recovery.

Accident Recovery

Reliable, discounted accident towing and recovery nationwide.

Safety and Reliability

All towing and recovery are handled at AA’s risk to ensure vehicle safety.

Personal Accident Protection

Some AA Kenya membership tiers also include or allow you to add Personal Accident Cover, providing:

Accidental death benefits

Permanent or temporary disability compensation

Hospital cash and medical expense coverage

Funeral and last expense benefits

These benefits are accessible through your AA Kenya membership, available to Step by Step Insurance clients. The goal is simple — to keep you moving safely and confidently, no matter what happens on the road.

VI. Step 5: Partner with Experts for the Right Policy

Finding the ideal motor insurance policy is about fit, not just price. At Step by Step Insurance Agency, we go beyond selling policies — we focus on understanding your needs and ensuring every aspect of your protection plan adds real value. Our process is built around expert assessment, transparency, and trusted partnerships that guarantee peace of mind on and off the road.

Our Expertise

What You Get

Tailored Assessment

We analyze your car, budget, and driving habits to match the right policy.

Clear Guidance

We simplify complex terms and explain what each policy truly covers.

Trusted Partnerships

We work with top Kenyan underwriters and service partners like AA Kenya to ensure reliability and prompt claims.

Transparent Pricing

You understand exactly what you’re paying for and why.

VII. Step 6: Take Action — Secure Your Protection Today

Your car is more than a machine — it’s a part of your daily life and financial security. Don’t wait until an accident or theft happens to realize the value of proper insurance. Take the next step with Step by Step Insurance Agency — your trusted road partner. We’ll help you select, customize, and secure a plan that ensures peace of mind on every journey.

📞 Contact Us

Ready to get the right motor insurance coverage? Reach out to our expert team today.

2025 Motor Insurance Pricing in Kenya: What You Need to Know

Comprehensive guide to the proposed changes affecting all vehicle owners

Kenya’s roads are about to see a significant shift—not just in the vehicles themselves, but in how we insure them. The proposed 2025 motor insurance pricing structure is set to impact private car owners, commercial operators, PSV drivers, motorcycle riders, tuk tuk owners, and fleet managers alike. If you’re planning to buy, renew, or adjust your motor insurance policy, understanding these changes is crucial. Let’s break down what’s new, what’s changing, and what it means for you.

Key Takeaways

New insurance bands based on vehicle value with rates ranging from 3.00% to 4.00%

PSVs face higher premiums due to increased risk exposure

Flexible add-ons now available for customized coverage

Age restrictions: 15 years max for private vehicles, 20 for commercial

Documentation requirements tightened for all policies

TPO remains the most affordable legal option but offers limited protection

Insurance is more than a legal requirement; it’s a financial safety net for millions of Kenyans. The 2025 pricing update comes at a time of evolving road usage, rising vehicle values, and increased risk factors. The Insurance Regulatory Authority, alongside industry stakeholders, has pushed for a review to ensure that premiums reflect current realities—balancing affordability with sustainability for insurers.

2. Private Motor Insurance: New Bands, New Rates

For private vehicle owners, the new pricing is structured around the sum insured—essentially, the value of your car. Here’s how the new basic rates break down:

Private Vehicle Insurance Rates

Sum Insured (KES)

Basic Rate (%)

500,000 – 1,500,000

4.00

1,500,001 – 2,000,000

3.75

2,000,001 – 2,500,000

3.50

Over 2,500,000

3.00

Minimum basic premiums also apply, ensuring that even lower-value vehicles contribute to the risk pool.

Add-Ons and Customization

Add-ons are becoming more flexible and transparent. You can now tailor your cover with options like:

Excess Protector (0.5% of sum insured, minimum KES 5,000)

Political Violence & Terrorism (PVT) (0.35% of sum insured, minimum KES 3,500)

Loss of Use

Windscreen and Radio Cover

These extras can make a big difference in the event of a claim, especially in unpredictable times.

3. Commercial Motor Insurance: Reflecting Real-World Risk