How to Balance SHA and Private Cover Without Overpaying

Let’s face it: navigating healthcare in Kenya right now feels like a balancing act. With the Social Health Authority (SHA) and its 2.75% mandatory deduction fully active, your monthly paycheck is already contributing to the government’s universal healthcare pool.

But if you already have a private health insurance policy — or your employer provides one — you might be asking yourself a critical question: “Am I paying twice for the exact same thing?”

The short answer is no. But you could be overpaying if you don’t know how to make them work together. Here is how to strategically balance SHA and your private cover so your family gets maximum protection without draining your wallet. For a broader look at the health insurance landscape, see our Kenya Insurance Q2 2026 industry update.

- SHA’s 2.75% mandatory deduction already covers baseline, emergency, and chronic illness costs — you don’t need to duplicate this in your private policy.

- Restructuring your private insurance as a top-up or co-pay model can significantly reduce your monthly premiums.

- Route routine and outpatient care through SHA to keep your private claims ratio low and control renewal costs.

- Use private cover strategically for specialist access, private rooms, and faster diagnostics — not everyday care.

- SHA and private insurance are partners, not competitors — understanding this distinction saves you money.

Join Our Insurance Community on WhatsApp

Get real-time updates, tips, and discussions on insurance trends and news in Kenya — straight to your phone. No spam, no sales pressure. Just a community of people who want to stay informed.

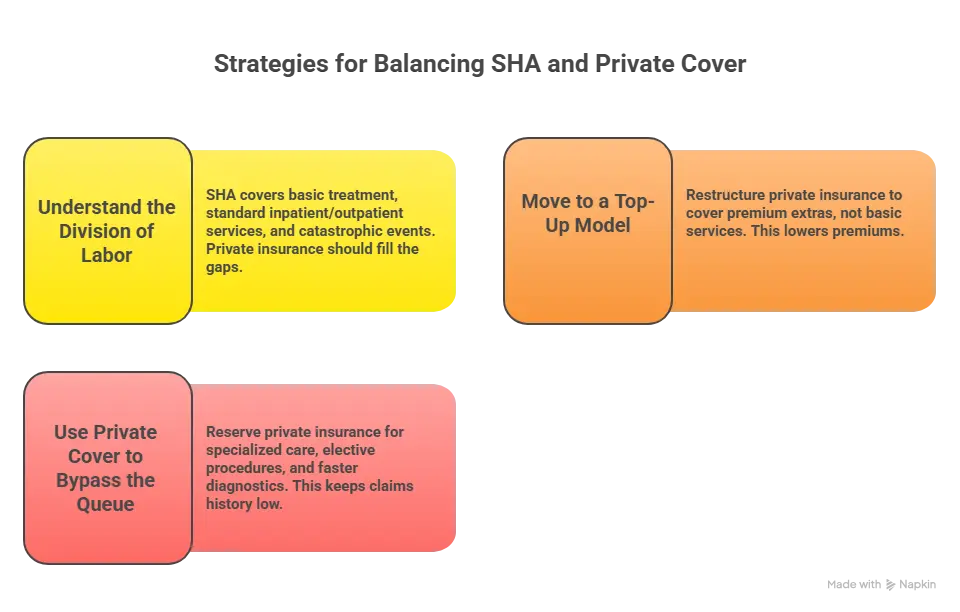

🏥 1. Understand the Division of Labor: Who Pays for What?

To avoid overpaying, you first need to stop looking at SHA as a competitor to private insurance — and start treating it as your first line of defense.

SHA is structured around three distinct funds, each designed to cover a different layer of healthcare need. Understanding how these SHA fund structures work is key to making smarter private insurance decisions:

| SHA Fund | What It Covers | Facility Level |

|---|---|---|

| 🏠 Primary Healthcare Fund | Free basic treatment — everyday walk-in care, general consultations | Level 1–3 dispensaries & community health centers |

| 🏨 Social Health Insurance Fund (SHIF) | Standard inpatient & outpatient — scheduled admissions, routine surgeries, specialist consultations | Accredited referral public hospitals |

| 🚨 Emergency, Chronic & Critical Illness Fund | Catastrophic events — ICU care, major accidents, cancer treatment, kidney dialysis | All accredited facilities |

📊 2. Move Your Private Insurance to a Top-Up or Co-Pay Model

If you are buying private insurance for yourself, your family, or your business, it is time to review your policy limits and structure. Because SHA is mandatory and covers a baseline of inpatient costs, your private insurance should no longer be treated as the sole payer.

Instead, it should act as the premium layer that fills the gaps SHA does not cover. This is especially relevant for SMEs managing group medical cover — where restructuring can yield significant savings across an entire employee pool.

How the top-up model works in practice:

| Step | Who Pays | What It Covers |

|---|---|---|

| 1️⃣ First Layer | SHA (SHIF) | Hospital admission, bed charges, basic diagnostics |

| 2️⃣ Second Layer | Private Insurance | Private room upgrades, high-end specialists, medication not on SHA essential list |

This is one of the most underutilised strategies for Kenyan individuals and SMEs managing group medical covers right now. If you are unsure whether your current policy already reflects this structure, a quick consultation with our team can clarify exactly where your money is going.

⏱️ 3. Use Private Cover to Bypass the Queue

While SHA’s vision is universal and commendable, the reality of public health infrastructure means that access to certain facilities, specialists, and turnaround times can be limited — especially during high-demand periods.

This is exactly where your private insurance earns its keep.

The strategic split:

| Use SHA For… | Use Private Insurance For… |

|---|---|

| Routine, predictable healthcare needs | Specialized or elective procedures |

| Managed chronic conditions | Faster diagnostic turnaround |

| Basic maternity care | Access to specific private hospitals not in SHA network |

| Standard lab tests at public facilities | Preferred specialist consultations |

| General outpatient visits at fully empaneled facilities | Premium accommodation upgrades |

It’s also worth ensuring your vehicle documentation is in order if you’re managing a fleet or driving to medical facilities regularly — our 2026 NTSA e-Logbooks guide is a useful parallel read for comprehensive personal risk management.

🤝 The Bottom Line: SHA and Private Cover Are Partners, Not Competitors

The smartest approach to health insurance in Kenya today is not choosing between SHA and private cover. It is understanding how they complement each other — and structuring your private policy to fill the specific gaps that SHA does not address.

✅ Strategy Summary

- Let SHA handle your baseline and emergency coverage as your mandatory first layer.

- Restructure your private policy as a top-up cover to avoid paying twice for the same benefits.

- Route routine care through SHA facilities to preserve your private limits and control your renewal premiums.

Done right, this approach can reduce your private insurance costs while actually improving the overall quality of cover your family has access to. For more context on how insurance sectors are evolving in Kenya, read our piece on why life insurance is overtaking general insurance in 2026.

If you or a family member has a pending compensation claim — for example through PCF — our PCF compensation claim guide for KUSCCO, Corporate, and Trident policyholders explains the exact steps to follow.

📚 Related Reading

Explore more from the Step by Step Insurance resource library:

| Topic | Category | Read Now |

|---|---|---|

| NTSA e-Logbooks Kenya 2026: Complete Guide | Motor | Read → |

| Kenya Insurance Q2 2026 Industry Update | Industry | Read → |

| How to Claim Your PCF Compensation (KUSCCO, Corporate & Trident) | Claims | Read → |

| Why Life Insurance Is Overtaking General Insurance in Kenya (2026) | Trends | Read → |

🔍 Not sure how your current policy compares to what SHA already covers?

The team at Step by Step Insurance can review your existing cover, identify where you are duplicating benefits, and recommend a right-sized policy that works alongside SHA — not against it.

Step by Step Insurance is a licensed insurance intermediary in Kenya, helping individuals, families, and businesses navigate health cover with clarity and confidence. This article is for informational purposes only and does not constitute financial or legal advice. Please consult a qualified insurance professional for personalised guidance.