Finance Bill 2026 Kenya: How the New Bank Insurance Ban Saves You Money

Navigating Kenya’s Finance Bill 2026: Your Wallet, Your Choice, and the End of Forced Insurance — The financial landscape in Kenya is undergoing a massive shift. Between the high-stakes clauses of the Finance Bill 2026 and the groundbreaking new Draft Financial Consumer Protection Framework, the rules governing your money are changing fast. While the Finance Bill introduces new tax pressures that will affect your daily expenses, the new consumer protection framework hands you a powerful weapon to fight back against predatory financial bundling.

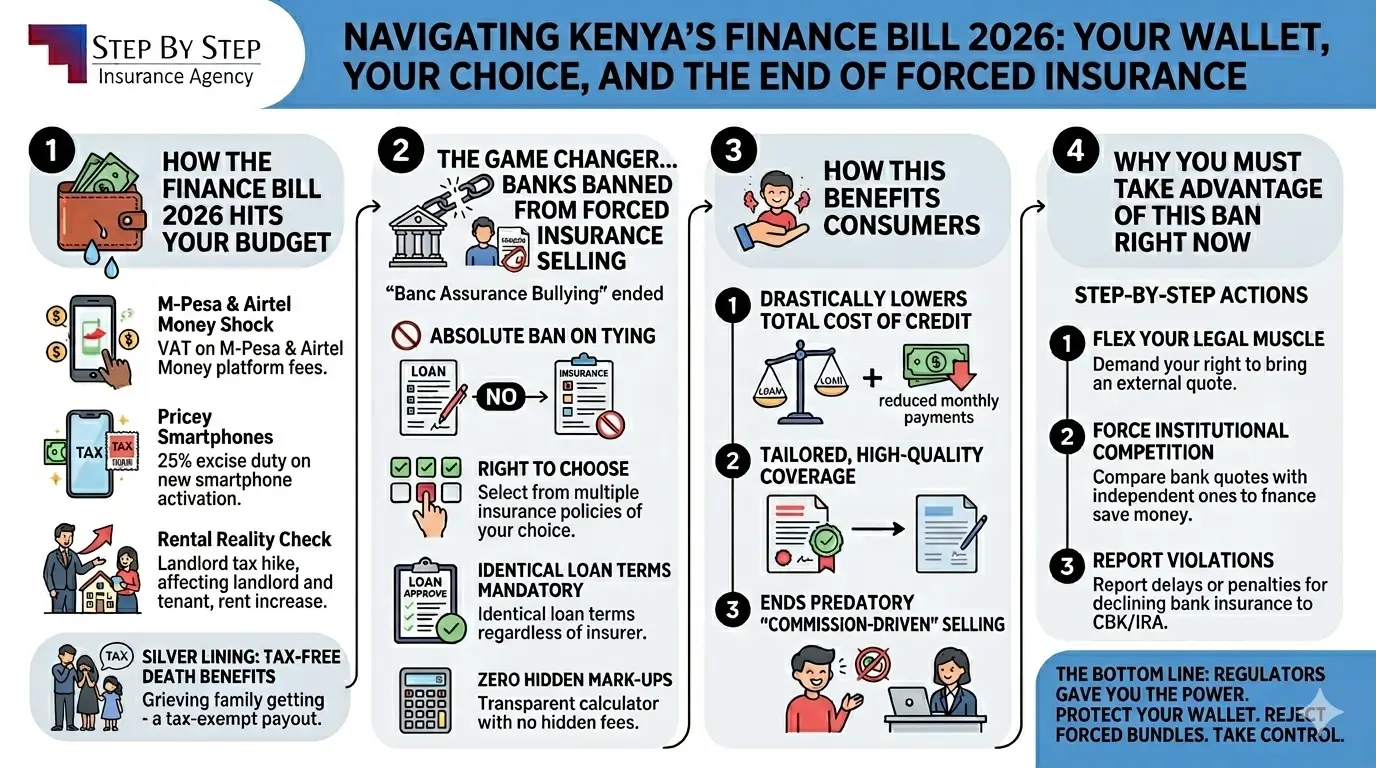

Here is everything you need to know about how these changes affect your wallet, how banks have been banned from forcing insurance on you, and why you must take advantage of this new economic freedom today.

📌 Key Takeaways

- Forced insurance ban: Banks can no longer make loan approval conditional on buying their in-house insurance.

- Right to choose: You can pick any independent provider – identical loan terms, no hidden penalties.

- Finance Bill 2026: 16% VAT on mobile money fees, 25% smartphone duty, rental tax hike to 10% – protect your cash flow by cutting loan costs.

- Savings opportunity: Shopping around for credit life or asset insurance drastically lowers total monthly repayments.

- Legal power: Report any bank intimidation to CBK or IRA – the law is on your side.

📑 Table of Contents

Get real-time updates on consumer rights, loan savings, and insurance news.

📊 Part 1: How the Finance Bill 2026 Hits Your Daily Budget

The National Treasury’s latest tax proposals directly target digital services, mobile connectivity, and housing. While the government aims to expand the tax bracket, economists warn that these costs will inevitably trickle down to the everyday consumer.

- The M-Pesa & Airtel Money Shock: The bill removes the VAT exemption on digital financial platform fees, slapped with a 16% VAT on top of the existing 20% excise tax. Telecommunications companies warn this will inflate overall mobile money transaction fees by up to 18.4%.

- Pricey Smartphones: A 25% excise duty will be collected the moment a new smartphone is activated on a local network, immediately driving up the cost of digital access.

- The Rental Reality Check: Landlords face a residential rental income tax hike from 7.5% back to 10%. Expect landlords to pass this 2.5% increase directly onto tenants in the form of higher rent.

- The Silver Lining (Tax-Free Death Benefits): In a rare win for consumers, any death benefits paid out from registered pension funds or individual retirement schemes will now be completely exempt from income tax, safeguarding grieving families from KRA deductions.

⚡ Part 2: The Game Changer—Banks Banned from Forced Insurance Selling

For years, Kenyan consumers seeking loans, mortgages, or logbook financing faced a frustrating roadblock: bancassurance bullying. To get your loan approved, banks routinely forced you to buy an expensive insurance policy directly from their preferred, in-house insurance partner. The Draft Financial Consumer Protection Framework 2026—jointly released by the Central Bank of Kenya (CBK) and the Insurance Regulatory Authority (IRA)—has officially ended this predatory practice. Here are the strong regulatory pointers that protect you under the new law:

- The Absolute Ban on Tying: Financial institutions are legally prohibited from making purchasing their own insurance policy a mandatory condition for loan approval.

- The Right to Choose: Lenders must inform you in writing of your absolute right to select an independent insurance provider of your own choice.

- Identical Loan Terms Mandatory: If you reject the bank’s internal insurance option, the bank cannot punish you. They are legally required to offer you the standalone loan product on identical terms, processing speeds, and interest rates.

- Zero Hidden Mark-ups: Banks are explicitly banned from inflating insurance premium prices or tacking on hidden “management fees” for handling external policies.

🔐 Your right to choose independent coverage is now law.

This means when applying for a loan, always request a standalone quote and compare with external providers like StepByStep Insurance. You can request a quote online or speak to our experts.

✅ Part 3: How This Benefits Consumers

This regulatory crackdown represents a massive victory for consumer rights and financial freedom in Kenya.

1. Drastically Lowers the Total Cost of Credit

When banks bundle their own insurance, they often charge premium rates well above the market average because they hold a monopoly over your loan approval. By breaking this monopoly, you can shop around for the most affordable credit life or asset insurance on the market, significantly reducing your total monthly loan repayment amounts.

2. Tailored, High-Quality Coverage

Bank-mandated insurance policies are typically “one-size-fits-all” cookie-cutter products designed to protect the bank’s money, not your specific needs. Now, you can consult an independent broker to choose a policy that offers better terms, lower deductibles, and superior critical illness or asset coverage for your family.

3. Ends Predatory “Commission-Driven” Selling

Bank tellers and credit officers have historically been incentivized by heavy internal commissions to aggressively push bundled insurance products onto unsuspecting borrowers. The new framework forces transparency, wiping out these conflicts of interest and ensuring you are treated fairly.

📋 Essential Internal Resources

| Guide / Resource | Description | Access Link |

|---|---|---|

| NTSA e-logbooks Kenya 2026 Guide | Digital logbooks, asset registration & insurance compliance | Read Guide → |

| Kenya Insurance Q2 2026 Report | Market trends, premium insights & regulatory updates | View Report → |

| Request a Quote | Compare insurance offers | Get Quote → |

| Contact Our Advisory Team | Speak with us about your rights under new framework | Contact Page → |

🚀 Part 4: Why You Must Take Advantage of This Ban Right Now

With inflation and new taxes from the Finance Bill 2026 squeezing disposable income, you cannot afford to leave money on the table. Taking advantage of the forced-insurance ban is one of the easiest ways to actively protect your cash flow.

- Flex Your Legal Muscle: The next time you apply for a personal loan, asset finance, or a mortgage, do not blindly sign the attached insurance paperwork. Demand your right to bring an external quote.

- Force Institutional Competition: Use this law to make institutions compete for your business. Take the bank’s insurance quote, walk into independent insurance firms, and ask them to beat it. You will surprise yourself with how many thousands of shillings you save.

- Report Violations: If a credit officer hints that your loan processing will delay, or that your interest rate will go up because you declined their insurance policy, they are breaking the law. Armed with this framework, you can confidently report them to the CBK or the IRA.

🔗 External References & Official Sources

- Finance Bill 2026 Memorandum — VAT exemption removal on insurance & financial services (Official Draft)

- Central Bank of Kenya (CBK) — Draft Financial Consumer Protection Framework 2026 summary

- Insurance Regulatory Authority (IRA) — Consumer rights guidelines on bancassurance

📢 StepByStep Insurance — Independent advice for Kenyan consumers. Need a quote? Compare insurance plans today and save on loan protection.