Imagine waking up to news that your insurance provider has suffered a major cyberattack, and your personal data—perhaps even your financial information—might be at risk. In today’s hyper-connected world, such scenarios are no longer the stuff of fiction. As cyber threats escalate in complexity and frequency, regulatory bodies worldwide are stepping up to safeguard consumers and ensure industry accountability.

Key Takeaway

The IRA’s new directive mandates 24-hour disclosure of major cybersecurity breaches, aiming to enhance transparency, protect policyholders, and align Kenya’s insurance sector with global standards. This move is expected to improve cyber hygiene and market confidence while positioning Kenya as a regional leader in regulatory practices.

The IRA’s directive isn’t a vague suggestion—it’s a binding requirement that applies to every licensed insurance company operating within Kenya’s borders. But what exactly qualifies as a “major” cybersecurity breach? While the specifics may evolve, the focus is on incidents that could compromise sensitive customer data, disrupt critical operations, or have a material impact on policyholders and the insurer’s reputation.

Scope of Disclosure

Think of breaches that expose thousands of customer records, ransomware attacks that paralyze claims processing, or unauthorized access to confidential underwriting data. These are the kinds of incidents that must be reported, and the threshold is intentionally set to prioritize events with the greatest potential for harm.

Reporting Timeline

Time is of the essence in the digital age. The IRA’s 24-hour disclosure window reflects the urgency required to contain threats and protect stakeholders. Insurers are now required to notify the regulator within a single day of detecting a qualifying breach. This tight deadline is designed to prevent cover-ups, minimize damage, and enable swift regulatory intervention.

Reporting Channels

To streamline the process, the IRA has established secure, official communication platforms for incident reporting. Insurers must submit detailed reports outlining the nature of the breach, the systems and data affected, the potential impact on policyholders, and the steps being taken to contain the fallout.

Objectives and Rationale

This isn’t just a bureaucratic exercise. The information provided enables the IRA to assess systemic risks, coordinate industry-wide responses if necessary, and provide guidance or support to affected companies. It also sets the stage for public communication, when warranted, to keep consumers informed and empowered.

Enhancing Transparency

Transparency is the lifeblood of trust in the insurance industry. When customers entrust their personal and financial information to insurers, they expect honesty and openness—especially when things go wrong. The new breach disclosure rule is a direct response to this expectation, ensuring that both regulators and the public are promptly informed of significant cyber incidents.

Protecting Policyholders

At its core, insurance is about protection—shielding individuals and businesses from unforeseen risks. But what happens when the insurer itself becomes the source of risk? Cyberattacks can expose sensitive data, disrupt claims processing, and even lead to financial losses for customers.

Regulatory Oversight

Effective regulation requires timely, accurate information. By mandating immediate breach disclosure, the IRA enhances its ability to monitor emerging threats, investigate incidents, and enforce compliance. This proactive stance positions the regulator as a guardian of the sector’s integrity, rather than a passive observer.

Alignment with Global Best Practices

It also creates a feedback loop: as more breaches are reported and analyzed, the IRA can identify patterns, issue sector-wide guidance, and refine its regulatory approach to stay ahead of evolving cyber risks.

International Standards

Kenya’s move is not happening in a vacuum. Around the world, regulators are tightening breach notification requirements to keep pace with the digital threat landscape. The European Union’s General Data Protection Regulation (GDPR), for example, requires data controllers to report personal data breaches to supervisory authorities within 72 hours. Several U.S. states have enacted similar laws, with some mandating even shorter timelines for financial institutions.

Promoting Robust Cybersecurity Frameworks

Breach disclosure is just one piece of the puzzle. To comply with the new directive, insurers must invest in robust cybersecurity frameworks, including advanced threat detection, incident response protocols, and ongoing staff training. The regulation acts as a catalyst, pushing companies to move beyond basic compliance and embrace a culture of continuous improvement.

Risk Management and Sector Resilience

The insurance sector is uniquely exposed to cyber risk—not just as a target, but also as a provider of cyber insurance products. By raising the bar for breach disclosure and incident response, the IRA is encouraging insurers to “walk the talk” on risk management. This, in turn, enhances sector-wide resilience and reduces the likelihood of systemic crises triggered by cyber incidents.

Expected Impact on Kenya’s Insurance Sector

This shift is especially important as cyber threats become more sophisticated. From phishing attacks to supply chain compromises, the tactics used by malicious actors are constantly evolving. Insurers that invest in resilience today will be better equipped to withstand the challenges of tomorrow.

One of the most immediate effects of the new rule will be a marked improvement in cyber hygiene across the industry. Insurers will be motivated to conduct regular security audits and vulnerability assessments, implement multi-factor authentication and encryption for sensitive data, develop and test incident response plans, and foster a culture of cybersecurity awareness among employees.

Market Confidence

Trust is the currency of the insurance industry. When customers believe that their data is safe and that companies will be honest about incidents, they are more likely to purchase and retain policies. The mandatory disclosure rule sends a clear signal that the Kenyan insurance sector is committed to transparency and accountability.

Regulatory Benchmarking

Kenya’s move positions it as a regional leader in insurance regulation and digital risk management. As neighboring countries grapple with similar challenges, the IRA’s approach may serve as a blueprint for others seeking to modernize their regulatory regimes.

Real-World Scenarios: What Does This Look Like in Practice?

To bring these concepts to life, let’s consider a hypothetical scenario:

Scenario: A major Kenyan insurer detects unauthorized access to its customer database late on a Friday evening. Within hours, the company’s IT team confirms that sensitive data—including names, ID numbers, and policy details—may have been compromised.

Challenges and Considerations

No regulation is without its challenges. Insurers may worry about the reputational impact of disclosing breaches, especially in a highly competitive market. There are also practical concerns—such as ensuring that incident detection systems are robust enough to identify breaches quickly, and that reporting channels are secure and efficient.

The Road Ahead: Building a Safer Digital Future

The mandatory 24-hour breach disclosure rule is not an endpoint—it’s a starting point for a broader transformation of Kenya’s insurance sector. As digitalization accelerates, the risks and rewards of technology will only grow. Insurers that embrace transparency, invest in resilience, and prioritize customer protection will be best positioned to thrive in this new landscape.

Conclusion

Kenya’s new mandatory cybersecurity breach disclosure rule marks a watershed moment for the country’s insurance sector. By prioritizing transparency, regulatory oversight, and alignment with global best practices, the IRA is laying the foundation for a safer, more resilient digital future.

In an era where digital transformation is revolutionizing business operations across Kenya, the threats that come with this shift have also evolved rapidly. From small businesses in Nairobi to tech startups in Mombasa and financial institutions across the country, no sector is immune to the menace of cybercrime.

Whether it’s data breaches, ransomware attacks, phishing schemes, or online identity theft, Kenyan enterprises are increasingly vulnerable to cyber threats that not only disrupt operations but can also cause irreversible financial and reputational damage.

Unfortunately, many businesses still consider cybersecurity as purely an IT department issue, overlooking the fact that cyber incidents can have profound legal, regulatory, and financial repercussions. This mindset has left a gap in protection, one that cybercrime insurance is uniquely designed to fill.

Cyber insurance, also known as cyber liability insurance, is an essential risk management tool that provides coverage against the fallout of cyberattacks and digital threats. Yet, many Kenyan entrepreneurs and executives are unaware of its existence or importance. That’s why the Step By Step Insurance Agency is taking the lead in educating and equipping businesses with expert advice and customized cyber insurance solutions to help them stay secure in a connected world.

Key Takeaways

Cybercrime is rising in Kenya, affecting businesses of all sizes.

Online breaches like phishing, ransomware, and BEC are common and costly.

Cyber insurance covers data recovery, legal fees, PR, and ransom payments.

Step By Step Insurance Agency offers expert guidance and tailored cyber insurance policies.

Every business should assess its risk and secure a cyber insurance cover today.

Kenya’s rapid digitization and growing reliance on mobile money, internet banking, and cloud computing have unfortunately made it a ripe target for cybercriminals. According to the Communications Authority of Kenya, over 200 million cyber threat events were detected in Kenya in 2023 alone. This marks a dramatic increase compared to previous years, highlighting the urgent need for robust cybersecurity frameworks and insurance solutions.

SMEs, which make up over 90% of businesses in Kenya, are particularly vulnerable due to limited resources, outdated IT infrastructure, and poor awareness of cyber risks. These businesses often lack the capacity to recover quickly from attacks, making them soft targets for hackers. The cost of recovery can be crippling, with some businesses losing millions and even closing shop after serious breaches.

Back of hacker, person and dark computer for cybersecurity, ransomware and data password for crime. Error, thief and spy coding pc software for scam, phishing and hacking online firewall with malware

Common Types of Online Breaches Affecting Kenyan Businesses

Cyber threats are multifaceted and constantly evolving. Below are some of the most prevalent online breaches affecting businesses in Kenya:

Phishing Attacks:

Fraudsters trick employees into revealing sensitive information like passwords or bank details through fake emails or websites.

Ransomware:

Malicious software locks critical data or systems until a ransom is paid. Kenyan hospitals and schools have been victims of such attacks.

Data Breaches:

Unauthorized access to confidential customer or business data. This is a serious concern for banks, SACCOs, and ecommerce platforms.

Business Email Compromise (BEC):

Hackers impersonate company executives or suppliers to trick employees into transferring funds or data.

Insider Threats:

Disgruntled or careless employees who intentionally or accidentally compromise company systems.

These breaches not only lead to financial losses but can also attract penalties under data protection laws and severely damage a company’s brand.

What Is Cyber Insurance

Cyber insurance is a type of coverage that protects businesses and individuals from losses related to cyber incidents.

It typically covers:

Data recovery costs after a breach

Business interruption losses during a cyber incident

Legal fees for dealing with lawsuits or regulatory investigations

Notification costs to inform affected customers

Reputation management and PR services

Ransom payments in the case of ransomware attacks

The goal is to help organizations recover quickly and efficiently while minimizing financial and reputational damage. As cyberattacks become more sophisticated and frequent, having cyber insurance is no longer a luxury but a necessity.

Kenya’s business ecosystem is becoming more digitized, and the threats are more real than ever.

Here are key reasons why cybercrime insurance is vital:

Financial Protection:

The cost of responding to a breach can run into millions. Cyber insurance ensures your business isn’t wiped out by a single attack.

Regulatory Compliance:

With Kenya’s Data Protection Act in place, non-compliance after a breach can attract hefty fines. Insurance helps cover these liabilities.

Peace of Mind:

Knowing you’re covered allows you to focus on your core business operations without constant fear of cyber threats.

Customer Trust:

Demonstrating that your business is protected by cyber insurance boosts credibility and trust among clients and partners.

Rapid Recovery:

With insurance support, businesses can recover quicker through expert intervention and financial aid.

Step By Step Insurance Agency: Your Trusted Cyber Insurance Partner

At Step By Step Insurance Agency, we understand that digital threats require strategic solutions. That’s why we offer tailored Cyber Insurance policies backed by top underwriters in Kenya. Our role goes beyond just selling insurance policies — we educate, advise, and walk with our clients step by step in identifying their cyber risks and securing comprehensive coverage.

Our team provides:

Free consultation and cyber risk assessment

Policy comparison and customization

Claims support and advisory

Ongoing updates on cyber threat trends in Kenya

Whether you’re running a small business, an NGO, or a large corporate, Step By Step Insurance ensures you have the tools and cover you need to face cyber threats with confidence.

How to Choose the Right Cyber Insurance Policy

Not all cyber insurance policies are created equal. Here are tips for choosing the right one for your business:

Assess Your Risk Profile:

Consider your industry, data sensitivity, and technology use. A fintech company will have different needs from a retail store.

Understand Coverage Options:

Ensure the policy covers all aspects of a breach, including legal liabilities, business interruption, and third-party claims.

Check Limits and Exclusions:

Review what’s not covered, and make sure limits are sufficient to handle worst-case scenarios.

Work With an Expert Broker:

Engage with professional advisors like Step By Step Insurance Agency to get unbiased recommendations.

Regularly Review and Update:

Cyber threats evolve, so your coverage should too. Conduct annual reviews of your insurance plan.

Conclusion: Stay Secure, Stay Insured

Cyber threats are not a question of if but when. As Kenya continues to digitize, the risks will only grow in scale and complexity. Cyber insurance is no longer a futuristic concept — it is a present-day necessity that could determine the survival of your business after a cyber incident.

Step By Step Insurance Agency is committed to empowering Kenyan businesses with knowledge, tools, and tailored cyber insurance solutions to weather the storm of digital threats. Don’t wait until a breach cripples your operations or drains your finances. Secure your future now.

Ready to protect your business from cyber threats? Talk to Step By Step Insurance Agency today for a free consultation and let’s secure your digital journey — one step at a time.

In today’s digital landscape, where technology plays an integral role in business operations, the threat of cyberattacks looms larger than ever. Cyber insurance has emerged as a critical tool for small businesses in Kenya, providing essential protection against the financial repercussions of data breaches and cyber incidents.

As the reliance on digital infrastructure grows, so does the need for robust risk management strategies, making understanding how small businesses in Kenya benefit from cyber insurance more important than ever.

What is Cyber Insurance?

Cyber insurance, also known as cyber liability insurance, is a type of coverage designed to protect businesses from financial losses resulting from cyberattacks or data breaches. This insurance can cover a variety of incidents, including malware attacks, phishing scams, ransomware incidents, and denial-of-service attacks. For small businesses in Kenya, where digital transactions and online services are increasingly common, having a cyber insurance policy can mean the difference between recovery and financial ruin following a cyber incident.

The increasing frequency of cyberattacks is alarming. According to data from the Central Bank of Kenya (CBK), hacking incidents targeting financial institutions rose nearly three-fold to 444 million in the year ending June 2022. This surge highlights the urgent need for small businesses to safeguard their operations through effective risk management solutions like cyber insurance.

Overview of Increasing Cyber Threats

Small businesses are particularly vulnerable to cyber threats due to limited resources and cybersecurity expertise. A report by Kaspersky indicates that small businesses in Kenya experienced a 47% increase in cyberattacks in 2022. Unfortunately, many business owners remain unaware of the risks they face; over 90% reportedly do not recognize their exposure to growing cyber threats. This lack of awareness can lead to devastating consequences when an attack occurs.

By investing in cyber insurance, small businesses can not only protect themselves financially but also enhance their overall cybersecurity posture through access to risk management services often included in these policies. This introduction sets the stage for understanding how small businesses in Kenya benefit from cyber insurance by defining key terms and highlighting the relevance of this coverage in the context of increasing cyber threats.

The Importance of Cyber Insurance for Small Businesses

Why Do Small Businesses Need Cyber Insurance?

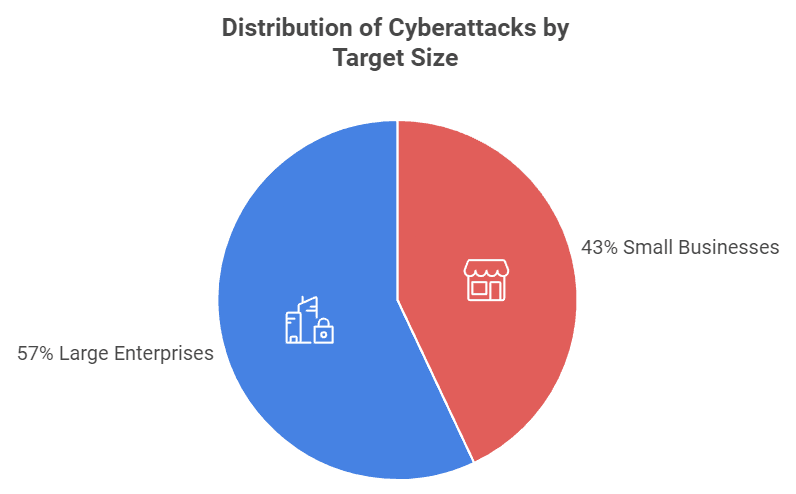

The necessity of cyber insurance for small businesses in Kenya cannot be overstated. As digital operations become more prevalent, so do the risks associated with them. Many small business owners mistakenly believe that they are not targets for cybercriminals, but this is a dangerous misconception. In fact, 43% of cyberattacks target small businesses, according to a report by Verizon. This statistic underscores the vulnerability of smaller enterprises, which often lack the resources to implement comprehensive cybersecurity measures.

Distribution of Cyberattacks by Target Size

Statistics on Cyberattacks Targeting Small Businesses in Kenya

47% increase in cyberattacks on small businesses in Kenya in 2022.

Over 90% of small business owners are unaware of their exposure to cyber threats.

The average cost of a data breach for small businesses can reach up to $200,000, which can be devastating for those operating on tight margins.

The Financial Impact of Cyberattacks

The financial repercussions of a cyberattack can be catastrophic for small businesses. A data breach not only incurs immediate costs—such as forensic investigations, legal fees, and public relations efforts—but also long-term damages, including loss of customer trust and potential regulatory fines.

For example, in 2021, a small retail business in Nairobi suffered a significant data breach that exposed customer payment information. The incident led to a $150,000 loss due to legal fees and compensation claims from affected customers. Additionally, the business experienced a 30% drop in sales over the following months as customers lost trust in their ability to protect sensitive information.

Conclusion: The Need for Proactive Measures

Given the alarming statistics and real-world consequences of cyber incidents, it is clear that small businesses in Kenya must prioritize cybersecurity. Cyber insurance serves as a vital safety net that not only protects against financial losses but also helps businesses recover more quickly from incidents. By understanding the importance of cyber insurance, small business owners can take proactive steps to safeguard their operations and ensure long-term sustainability. This section emphasizes the critical need for cyber insurance among small businesses in Kenya by presenting relevant statistics and real-life examples that illustrate the potential financial impact of cyberattacks.

Types of Cyber Insurance Coverage Available

Understanding the types of cyber insurance coverage available is essential for small businesses in Kenya as they seek to protect themselves from potential cyber threats. Cyber insurance policies typically fall into two main categories: first-party coverage and third-party coverage. Each type offers distinct benefits that can be tailored to the specific needs of a business.

a. First-Party Coverage

First-party coverage is designed to protect a business from direct losses incurred as a result of a cyber incident. This type of coverage typically includes:

Data Restoration Costs: Coverage for expenses related to restoring lost or compromised data, including hiring forensic experts to recover data.

Business Interruption Losses: Compensation for lost income during the downtime caused by a cyber incident, ensuring that the business can continue to operate after an attack.

Cyber Extortion: Protection against ransomware attacks, including costs associated with paying ransoms and negotiating with cybercriminals.

Notification Costs: Expenses related to notifying affected customers and stakeholders about a data breach, which may be required by law.

For example, if a small e-commerce business experiences a ransomware attack that locks them out of their systems, first-party coverage can help cover the costs of data recovery and any lost revenue during the downtime.

b. Third-Party Coverage

Third-party coverage protects businesses from liabilities arising from claims made by customers, partners, or other third parties affected by a cyber incident. This type of coverage typically includes:

Legal Defense Costs: Coverage for legal fees incurred when defending against lawsuits related to data breaches or privacy violations.

Regulatory Fines and Penalties: Protection against fines imposed by regulatory bodies for failing to protect customer data or comply with data protection laws.

Settlements and Damages: Compensation for settlements or damages awarded to third parties as a result of a data breach.

For instance, if a small accounting firm inadvertently exposes client financial information due to a cyberattack, third-party coverage would help cover the legal fees and any potential settlements resulting from lawsuits filed by affected clients.

c. Combined Coverage

Many insurers offer combined policies that include both first-party and third-party coverage. This comprehensive approach allows small businesses to have robust protection against various risks associated with cyber incidents. By opting for combined coverage, businesses can ensure they are safeguarded against both direct losses and liabilities arising from third-party claims.

Conclusion: Tailoring Coverage to Business Needs

When considering cyber insurance, small businesses in Kenya should assess their unique risks and operational needs. Understanding the differences between first-party and third-party coverage is crucial for selecting the right policy. By tailoring their insurance coverage appropriately, small businesses can effectively mitigate potential financial losses stemming from cyber incidents. This section provides an in-depth look at the various types of cyber insurance coverage available to small businesses in Kenya, highlighting their specific benefits and real-world applications.

Key Benefits of Cyber Insurance for Small Businesses

Cyber insurance offers a multitude of benefits that can significantly enhance the resilience and sustainability of small businesses in Kenya. As cyber threats continue to evolve, having a comprehensive insurance policy can provide peace of mind and financial security. Here are some of the key advantages that small businesses can gain from investing in cyber insurance.

Financial Protection

One of the primary benefits of cyber insurance is its ability to provide financial protection against the significant costs associated with cyber incidents. The average cost of a data breach for small businesses can be staggering, often exceeding $200,000 when factoring in legal fees, regulatory fines, and lost revenue. Cyber insurance helps mitigate these costs by covering:

Data recovery expenses, including forensic investigations.

Business interruption losses, ensuring that income is preserved during downtime.

Cyber extortion payments in cases of ransomware attacks.

For example, a small hotel in Kenya that falls victim to a cyberattack may incur substantial costs related to data recovery and customer notification. With cyber insurance, these expenses could be covered, allowing the business to recover more quickly without crippling financial strain.

Legal Support and Compliance

As data protection regulations become more stringent globally, small businesses must navigate complex legal landscapes. Cyber insurance provides essential legal support by covering:

Legal fees associated with defending against lawsuits resulting from data breaches.

Regulatory fines imposed by authorities for non-compliance with data protection laws such as the Data Protection Act in Kenya.

By having a robust cyber insurance policy, small businesses can ensure they are prepared for potential legal challenges arising from cyber incidents. This support not only protects their finances but also helps maintain compliance with evolving regulations.

Risk Management Services

Many cyber insurance policies offer additional risk management services designed to enhance a business’s cybersecurity posture. These services may include:

Cybersecurity assessments to identify vulnerabilities within the organization.

Employee training programs focused on recognizing phishing attempts and other cyber threats.

Incident response planning to ensure a swift and effective reaction to potential breaches.

For instance, a small manufacturing company could benefit from risk management services that help them identify weak points in their cybersecurity strategy, thereby reducing the likelihood of a successful attack.

Business Continuity

In the event of a cyber incident, maintaining business continuity is crucial for minimizing disruption and financial loss. Cyber insurance plays a vital role in ensuring that businesses can recover quickly and resume operations. Coverage for business interruption losses allows companies to continue functioning even when their systems are compromised.For example, if a small retail store experiences a data breach that disrupts its online sales platform, cyber insurance can help cover lost revenue during the downtime while also funding recovery efforts.

Conclusion: Empowering Small Businesses

The benefits of cyber insurance extend far beyond mere financial protection. By providing legal support, risk management services, and ensuring business continuity, cyber insurance empowers small businesses in Kenya to navigate the complexities of the digital landscape with confidence. Investing in this coverage not only safeguards against potential losses but also fosters a proactive approach to cybersecurity. This section outlines the key benefits of cyber insurance for small businesses in Kenya, emphasizing financial protection, legal support, risk management services, and business continuity.

Understanding the Cost of Cyber Insurance

When considering cyber insurance, small businesses in Kenya must also understand the associated costs. The price of a cyber insurance policy can vary widely based on several factors, including the size of the business, the level of coverage required, and the specific risks faced by the industry. This section will explore these factors and provide insights into what small businesses can expect regarding premiums.

Factors Influencing Premium Costs

Several key factors influence the cost of cyber insurance premiums for small businesses:

Business Size: Larger businesses with more extensive operations and higher revenue may face higher premiums due to increased exposure to risk. Conversely, smaller businesses may benefit from lower rates, but they still need adequate coverage to protect against potential losses.

Industry Type: Certain industries are more prone to cyber threats than others. For example, businesses in finance, healthcare, and e-commerce often face higher premiums due to the sensitive nature of the data they handle. In contrast, a small retail store might have lower premiums but still needs coverage for potential risks.

Coverage Limits: The amount of coverage a business chooses will directly impact its premium. Higher coverage limits generally lead to higher costs. Small businesses should carefully assess their needs to strike a balance between adequate protection and affordability.

Claims History: A business’s history of previous claims can significantly affect its premium. Companies that have experienced multiple cyber incidents may face higher rates as insurers perceive them as higher risk.

Security Measures in Place: Insurers often evaluate the cybersecurity measures a business has implemented when determining premiums. Businesses that invest in robust cybersecurity practices—such as firewalls, encryption, and employee training—may qualify for lower rates due to reduced risk exposure.

Average Cost Range for Small Businesses in Kenya

While specific costs can vary widely, small businesses in Kenya can expect to pay anywhere from KES 30,000 to KES 200,000 annually for cyber insurance premiums, depending on the factors mentioned above. For example:

A small retail shop with minimal online transactions might pay around KES 30,000 for basic coverage.

A mid-sized e-commerce business handling sensitive customer data could see premiums rise to KES 100,000 or more, especially if they require extensive coverage.

It’s important for small business owners to shop around and compare quotes from different insurance providers to find the best policy that meets their needs and budget.

Conclusion: Budgeting for Cyber Insurance

Understanding the cost of cyber insurance is crucial for small businesses looking to safeguard themselves against cyber threats. By considering various factors that influence premiums and being aware of average costs, business owners can make informed decisions about their insurance needs. Investing in cyber insurance is not just an expense; it is a strategic move towards protecting their business’s future in an increasingly digital world. This section provides an overview of the costs associated with cyber insurance for small businesses in Kenya, detailing the factors that influence premiums and offering average cost ranges.

Challenges Small Businesses Face in Obtaining Cyber Insurance

While cyber insurance offers significant benefits, small businesses in Kenya often encounter various challenges when trying to obtain coverage. Understanding these obstacles can help business owners navigate the process more effectively and ensure they secure the protection they need. This section will explore common challenges and provide insights on how to overcome them.

Lack of Awareness and Understanding

One of the most significant hurdles small businesses face is a lack of awareness regarding cyber insurance and its importance. Many business owners do not fully understand what cyber insurance entails or how it can protect them from potential risks. This lack of knowledge can lead to hesitancy in pursuing coverage.To address this challenge, small businesses should invest time in educating themselves about cyber insurance. Resources such as industry reports, webinars, and consultations with insurance professionals can provide valuable insights. Additionally, engaging with local business associations or chambers of commerce can help raise awareness about the importance of cybersecurity and insurance.

Navigating the Application Process

The application process for cyber insurance can be complex and intimidating, especially for small business owners who may not have experience with insurance policies. Insurers typically require detailed information about a business’s operations, security measures, and previous claims history. This requirement can be overwhelming for those without a dedicated risk management team.To simplify the application process, small businesses should:

Prepare Thorough Documentation: Gather relevant information about current cybersecurity measures, employee training programs, and any past incidents. This preparation will help demonstrate to insurers that the business takes cybersecurity seriously.

Consult with Insurance Brokers: Working with an experienced insurance broker can streamline the process. Brokers can help small businesses understand their options, navigate complex policy language, and find coverage that meets their needs.

Affordability Concerns

Another challenge is the perception that cyber insurance is too expensive for small businesses operating on tight budgets. While premiums can vary significantly based on several factors, many small business owners may overlook the long-term cost savings that come with having coverage.To address affordability concerns:

Assess Risk vs. Cost: Business owners should evaluate the potential financial impact of a cyber incident compared to the cost of insurance. Understanding that a single data breach could result in losses far exceeding the annual premium may shift perspectives on affordability.

Explore Multiple Quotes: Small businesses should obtain quotes from various insurers to compare coverage options and pricing. This approach allows them to find a policy that fits their budget while still providing adequate protection.

Conclusion: Overcoming Challenges

While challenges exist in obtaining cyber insurance, small businesses in Kenya can take proactive steps to navigate these obstacles effectively. By increasing awareness, preparing for the application process, and understanding the value of coverage relative to potential losses, business owners can secure essential protection against cyber threats. Ultimately, overcoming these challenges is crucial for ensuring long-term business resilience in an increasingly digital landscape. This section discusses the common challenges small businesses face when seeking cyber insurance and provides actionable strategies for overcoming these obstacles.

How to Choose the Right Cyber Insurance Policy

Selecting the appropriate cyber insurance policy is a critical step for small businesses in Kenya looking to protect themselves from cyber threats. With various options available, it’s essential to understand how to evaluate policies effectively. This section will guide business owners through the process of choosing the right coverage tailored to their specific needs.

Assessing Your Business Needs

Before diving into policy comparisons, small business owners should conduct a thorough assessment of their unique risks and operational requirements. Here are key considerations to keep in mind:

Identify Specific Risks: Evaluate the types of data your business handles (e.g., customer personal information, payment details) and the potential vulnerabilities in your operations. For instance, a small retail business with an online store may face different risks compared to a local service provider.

Understand Regulatory Requirements: Familiarize yourself with any legal obligations related to data protection in Kenya, such as the Data Protection Act. Compliance with these regulations can influence the type of coverage needed.

Determine Coverage Needs: Consider what aspects of cyber incidents you want to be covered. Do you need protection against data breaches, cyber extortion, or business interruption? Identifying your priorities will help narrow down policy options.

Comparing Different Providers

Once you have a clear understanding of your needs, it’s time to compare policies from various insurance providers. Here are some steps to ensure you make an informed choice:

Research Insurers: Look for reputable insurance companies that specialize in cyber insurance. Check their financial stability and customer reviews to gauge their reliability.

Request Detailed Quotes: Obtain quotes from multiple insurers and ensure that they include comprehensive details about coverage limits, exclusions, and premium costs. This information will allow for an apples-to-apples comparison.

Evaluate Policy Terms: Carefully read through the policy terms and conditions. Pay attention to coverage limits, deductibles, and any exclusions that may affect your business in case of a claim.

Ask Questions: Don’t hesitate to reach out to insurers or brokers with questions about policy specifics or terms you don’t understand. Clarifying these points can prevent misunderstandings later on.

Engaging with Insurance Brokers

Working with an experienced insurance broker can significantly simplify the process of selecting a cyber insurance policy. Brokers can provide valuable insights into the market and help tailor coverage options based on your business needs. Here’s how brokers can assist:

Expert Guidance: Brokers have expertise in navigating the complexities of cyber insurance and can help identify suitable policies based on your risk profile.

Negotiation Power: Brokers often have established relationships with insurers, which can lead to better terms and pricing for your coverage.

Ongoing Support: A good broker will not only help you select a policy but also provide ongoing support throughout the life of the insurance, including assistance during claims processing.

Conclusion: Making an Informed Decision

Choosing the right cyber insurance policy requires careful consideration and thorough research. By assessing specific business needs, comparing different providers, and potentially engaging with an insurance broker, small businesses in Kenya can secure coverage that effectively mitigates risks associated with cyber threats. This proactive approach is essential for ensuring long-term resilience in an increasingly digital world. This section provides guidance on how small businesses can choose the right cyber insurance policy by assessing their needs, comparing providers, and utilizing brokers’ expertise.

Real-Life Examples of Cyber Insurance in Action

Understanding the practical implications of cyber insurance can be greatly enhanced by examining real-life case studies. These examples illustrate how small businesses in Kenya have successfully utilized cyber insurance to mitigate the impact of cyber incidents, recover from breaches, and reinforce their cybersecurity strategies. Here are two compelling case studies that highlight the benefits and effectiveness of cyber insurance.

Case Study 1: A Small Retail Business

Background: A small retail business in Nairobi, which operated both a physical store and an online platform, experienced a significant data breach when hackers gained access to its customer database. The breach exposed sensitive customer information, including names, addresses, and payment details.Incident: The cyberattack occurred during a peak shopping season, leading to immediate concerns about customer trust and financial losses. The business faced potential lawsuits from affected customers and regulatory scrutiny for failing to protect sensitive data.Response: Fortunately, the retail business had invested in a comprehensive cyber insurance policy that included both first-party and third-party coverage. This policy provided:

Data Restoration Costs: The insurance covered the expenses associated with forensic investigations to determine the breach’s scope and restore compromised data.

Business Interruption Losses: The policy compensated for lost revenue during the downtime caused by the incident, allowing the business to maintain financial stability.

Legal Defense Costs: The insurance covered legal fees associated with defending against lawsuits filed by affected customers.

Outcome: With the support of their cyber insurance policy, the retail business was able to recover quickly from the incident. They restored their systems within a week and launched a customer notification campaign to inform affected individuals. As a result, they managed to rebuild customer trust and resumed operations with improved cybersecurity measures in place.

Case Study 2: A Local Service Provider

Background: A small IT service provider based in Mombasa experienced a ransomware attack that encrypted critical business files and demanded a ransom payment for decryption keys. The attack not only disrupted operations but also threatened client projects and deadlines.Incident: Faced with the prospect of losing access to vital data, the service provider needed to act quickly. They had previously recognized their vulnerability and secured a cyber insurance policy that included coverage for ransomware attacks.Response: Thanks to their cyber insurance policy, the service provider received immediate support in several areas:

Cyber Extortion Coverage: The policy covered the ransom payment demanded by cybercriminals, allowing the business to regain access to its files without incurring significant out-of-pocket costs.

Incident Response Services: The insurer provided access to cybersecurity experts who helped assess the attack’s impact, implement security measures to prevent future incidents, and develop an incident response plan.

Legal Assistance: The policy also included legal support to navigate compliance issues related to data protection laws following the attack.

Outcome: With the assistance of their cyber insurance policy, the service provider was able to recover from the ransomware attack without crippling financial losses. They implemented stronger cybersecurity protocols as recommended by their insurer and regained client confidence by demonstrating their commitment to protecting sensitive information.

Conclusion: Learning from Real-Life Experiences

These case studies illustrate how small businesses in Kenya can benefit significantly from having cyber insurance in place. By providing financial protection, legal support, and access to expert resources, cyber insurance enables businesses to respond effectively to cyber incidents. As cyber threats continue to evolve, investing in such coverage becomes increasingly essential for ensuring long-term resilience and success in a digital world. This section presents real-life examples of how small businesses in Kenya have successfully utilized cyber insurance during cyber incidents. These case studies highlight the practical benefits of having coverage in place.

The Future of Cyber Insurance for Small Businesses in Kenya

As the digital landscape continues to evolve, so too does the importance of cyber insurance for small businesses in Kenya. With increasing reliance on technology and growing cyber threats, the future of cyber insurance is poised for significant transformation. This section will explore emerging trends, the role of technology in enhancing cybersecurity, and what small businesses can expect in the coming years.

Trends in the Cyber Insurance Market

Increased Demand for Coverage: As awareness of cyber threats grows, more small businesses are recognizing the need for cyber insurance. The demand for coverage is expected to rise sharply, especially as regulatory requirements become more stringent. Businesses that previously overlooked cyber insurance are now seeking policies to protect themselves from potential financial losses.

Tailored Policies for Small Businesses: Insurers are increasingly offering tailored policies specifically designed for small businesses. These policies take into account the unique risks faced by smaller enterprises and provide more relevant coverage options at competitive prices. This trend will make it easier for small businesses to find suitable insurance solutions.

Integration of Cybersecurity Services: Many insurers are beginning to bundle cybersecurity services with their insurance policies. This integration may include risk assessments, employee training programs, and incident response planning, providing small businesses with not just financial protection but also practical resources to enhance their cybersecurity posture.

Data-Driven Underwriting: The use of data analytics in underwriting is becoming more prevalent in the cyber insurance market. Insurers are leveraging data to assess risk more accurately, which can lead to more personalized premiums based on a business’s specific cybersecurity measures and claims history.

The Role of Technology in Enhancing Cybersecurity

Technology plays a crucial role in shaping the future of cyber insurance and enhancing overall cybersecurity for small businesses:

Advanced Threat Detection: Innovations in artificial intelligence (AI) and machine learning are enabling businesses to detect and respond to threats more effectively. These technologies can analyze patterns and identify anomalies that may indicate a cyber threat, allowing businesses to take proactive measures before an incident occurs.

Cloud-Based Solutions: Many small businesses are migrating to cloud-based solutions that offer enhanced security features. These solutions often include built-in protections against data breaches and ransomware attacks, reducing overall risk exposure.

Cybersecurity Training Tools: As human error remains a leading cause of security breaches, technology-driven training tools are becoming essential. Interactive training programs can help employees recognize phishing attempts and other cyber threats, fostering a culture of cybersecurity awareness within organizations.

What Small Businesses Can Expect

As the cyber insurance landscape evolves, small businesses in Kenya should prepare for several key developments:

Greater Accessibility: With increased competition among insurers and a growing recognition of the importance of cybersecurity, small businesses can expect more accessible and affordable cyber insurance options.

Emphasis on Risk Management: Insurers will likely place greater emphasis on risk management practices when underwriting policies. Small businesses that demonstrate strong cybersecurity measures may benefit from lower premiums and better coverage terms.

Ongoing Education and Support: The relationship between insurers and policyholders is expected to become more collaborative. Insurers will increasingly offer ongoing education and support to help small businesses stay informed about emerging threats and best practices for cybersecurity.

Conclusion: Preparing for the Future

The future of cyber insurance for small businesses in Kenya looks promising as awareness grows and coverage options expand. By staying informed about emerging trends and leveraging technology to enhance their cybersecurity posture, small business owners can position themselves effectively in an increasingly digital world. Investing in cyber insurance not only provides financial protection but also fosters resilience against evolving cyber threats. This section discusses the future of cyber insurance for small businesses in Kenya, highlighting emerging trends, technological advancements, and what business owners can expect moving forward.

Cyber Insurance in Kenya: Coverage, Trends & Business Protection | Step By Step Insurance

In today’s digital economy, Kenyan businesses increasingly rely on technology to operate, communicate, and serve customers. This growing dependence has also expanded exposure to cyber risks.

According to reports cited by the Communications Authority of Kenya, cyber incidents recorded across networks rose sharply toward the end of 2023, reflecting a rapidly evolving threat environment. Industry and media sources have also estimated that Kenyan organizations lose billions of shillings annually to cybercrime, highlighting the financial stakes involved.

These trends underline why many businesses are now considering cyber insurance as part of broader risk management—alongside cybersecurity controls—not as a replacement for them.

Key Takeaways

Cyber incidents in Kenya are increasing, with significant financial impacts on businesses.

Cyber insurance complements cybersecurity measures but doesn’t replace them.

Coverage varies widely between policies and providers—always review terms carefully.

The Data Protection Act 2019 increases exposure but doesn’t mandate cyber insurance.

The Kenyan cyber insurance market is maturing but faces challenges in product development and awareness.

Connect with other professionals interested in insurance trends, news, and insights in Kenya. Share knowledge, ask questions, and stay updated on the latest developments.

Cyber insurance does not prevent cyber attacks.

Instead, it helps organizations manage the financial and operational impact after an incident, working together with technical safeguards such as firewalls, staff training, backups, and incident response planning.

A well-structured cyber policy may assist with recovery costs following events like data breaches or ransomware attacks, but it should always be viewed as a complement to cybersecurity—not a substitute.

Current Cyber Threat Landscape in Kenya

Kenyan businesses continue to face common digital risks such as:

Ransomware attacks

Phishing and social engineering

Data breaches and unauthorized system access

It’s important to note that coverage for these risks depends entirely on policy wording, sub-limits, exclusions, and insurer conditions, which vary widely between providers.

Not every cyber policy automatically covers every threat.

Financial Impact of Cybercrime (Regional Context)

Cybercrime losses are often compared across countries such as Kenya, Nigeria, and South Africa. However, these figures are drawn from different reporting frameworks and methodologies, meaning they are not directly comparable.

What is clear is that cyber incidents already represent a material financial risk for African businesses—regardless of geography.

How SMEs in Kenya can leverage cyber insurance for financial protection.

What Cyber Insurance May Cover (Subject to Policy Terms)

Cyber policies may provide support for items such as:

Coverage Area

What It May Include

Important Considerations

Data Recovery & System Restoration

Costs to restore lost or corrupted data, repair systems

Often subject to sub-limits; may require proof of regular backups

Forensic Investigations

Identifying the cause, source, and extent of a breach

Usually requires insurer-approved investigators

Legal Defence & Regulatory Response

Legal fees, regulatory fines (where insurable by law), compliance costs

Fines may not be covered in all jurisdictions; check policy wording

Customer Notification & Credit Monitoring

Costs to notify affected individuals, provide credit monitoring services

May be required by law; coverage limits apply

These are not guaranteed inclusions.

Limits, waiting periods, excesses, and specific conditions apply, and some covers may only be available as optional extensions.

Businesses should always review policy schedules carefully.

Business Continuity Support (Illustrative Example)

Consider a hypothetical scenario: a Kenyan SME suffers a ransomware incident that disrupts operations for several days. With cyber insurance in place, the business may receive assistance toward recovery costs and downtime losses—depending on policy terms—helping it resume operations faster than if it were self-funding the entire response.

This example is illustrative only. Actual outcomes depend on individual policy conditions and claim circumstances.

Regulatory Context in Kenya

Kenya’s Data Protection Act 2019 increases organizations’ legal and financial exposure when personal data is compromised.

However, the Act does not mandate cyber insurance.

Instead, it heightens compliance obligations and potential penalties, making cyber insurance a risk management decision, not a legal requirement.

Cybersecurity Skills Gap

Industry estimates and regional cybersecurity studies suggest Kenya has far fewer trained cybersecurity professionals than required, with demand significantly outpacing supply.

These figures are based on market research and global cyber workforce indices—not official government counts—but they highlight a real capacity gap that leaves many organizations underprepared.

As a result, some businesses turn to cyber insurance as an additional layer of financial protection.

Challenges Facing the Cyber Insurance Market in Kenya

Cyber insurance locally is still maturing.

Key challenges include:

Challenge

Impact on Businesses

Slow product development

Limited policy options tailored to Kenyan business realities

May not fully address local regulatory and operational contexts

Many policies offered today are adapted from global insurance frameworks rather than being fully localized for Kenyan operating realities.

This has led to cautious underwriting, narrower coverage, and increasing scrutiny of cybersecurity controls before insurers provide terms.

While awareness and adoption are expected to grow, the market is also likely to tighten.

As claims increase, businesses should expect:

More detailed risk assessments

Stricter exclusions and conditions

Higher premiums for poorly secured organizations

At the same time, insurers are exploring analytics and technology-driven underwriting to better align coverage with real risk profiles.

The direction is positive—but not without increased discipline on both insurer and client sides.

Conclusion

Cyber risk is now a core business issue in Kenya—not just an IT concern.

Cyber insurance offers financial and operational support after incidents, but it works best when combined with strong cybersecurity practices and informed policy selection.

It is not a silver bullet—rather, it is one component of a broader resilience strategy.

In today’s digital landscape, where businesses increasingly rely on technology for their operations, the significance of cyber insurance has never been greater. Cyber insurance, also known as cyber liability insurance, provides essential coverage against a myriad of cyber threats, including data breaches, ransomware attacks, and network security lapses.

As organizations in Kenya embrace digital transformation and expand their online presence, they inadvertently expose themselves to various cyber risks that can lead to significant financial losses and reputational damage.

The urgency for cyber insurance is underscored by alarming statistics.

In 2022, Kenya lost at least $153 million (approximately Sh20.4 billion) due to cybercrime, with projections indicating a 14% annual increase in such incidents. This trend highlights the pressing need for businesses to adopt comprehensive cybersecurity measures, including cyber insurance, to safeguard their assets and operations. For more insights on the financial impact of cybercrime in Kenya, you can refer to the Business Daily Africa.

Moreover, the Computer Society of Kenya reports a severe shortage of cybersecurity expertise in the country, with only about 1,700 professionals available compared to a demand ranging between 40,000 to 50,000. This gap exacerbates the risks businesses face in protecting themselves from cyber threats. The need for effective risk management strategies, including cyber insurance, is more critical than ever.

Cyber insurance plays a vital role by providing coverage for various cyber risks. It alleviates the financial burdens associated with incidents such as data breaches and extortion demands. This specialized form of insurance extends coverage for expenses like legal fees, regulatory fines, costs related to data recovery efforts, and payments demanded by extortionists. For a detailed overview of what cyber insurance entails and its importance in Kenya, check out Divani’s guide on Cyber Risk Insurance.

As we delve deeper into this topic, we will explore the types of cyber threats businesses face and how cyber insurance can play a pivotal role in risk management strategies. Understanding cyber insurance is not just about compliance—it’s about ensuring business continuity in an increasingly perilous digital environment.

Types of Cyber Threats Businesses Face

As businesses in Kenya increasingly adopt digital technologies, they become more vulnerable to a range of cyber threats. Understanding these threats is crucial for implementing effective cybersecurity measures and considering appropriate cyber insurance coverage. Below are some of the most common and emerging cyber threats that organizations should be aware of:

Common Cyber Threats

Data Breaches:

A data breach occurs when unauthorized individuals gain access to sensitive information, such as customer data, financial records, or intellectual property. According to the 2022 Data Breach Investigations Report, 83% of data breaches involved human error, highlighting the need for robust training and awareness programs.

Ransomware Attacks:

Ransomware is a type of malware that encrypts a victim’s files and demands payment for the decryption key. In Kenya, ransomware attacks have increased significantly, with businesses facing demands that can reach millions of shillings. The [Cybersecurity & Infrastructure Security Agency (CISA)](https://www.cisa.gov/ ransomware) emphasizes the importance of regular backups and incident response plans to mitigate these risks.

Phishing Schemes:

Phishing involves tricking individuals into providing sensitive information, such as passwords or credit card numbers, often through deceptive emails or messages. The Anti-Phishing Working Group reported over 200,000 phishing attacks in the first quarter of 2023 alone, underscoring the prevalence of this threat.

Malware and Viruses:

Malware encompasses various malicious software types designed to infiltrate and damage systems. This includes viruses, worms, and spyware. A report by Kaspersky indicates that malware attacks are on the rise globally, affecting businesses of all sizes.

Emerging Threats

Advanced Persistent Threats (APTs):

APTs are prolonged and targeted cyberattacks where an intruder gains access to a network and remains undetected for an extended period. These threats are often state-sponsored or conducted by highly skilled groups aiming to steal sensitive information.

Insider Threats:

Insider threats occur when employees or contractors misuse their access to company data for malicious purposes or unintentionally cause security breaches. According to a study by IBM, insider threats account for 60% of all data breaches.

IoT Vulnerabilities:

The increasing use of Internet of Things (IoT) devices in businesses introduces new vulnerabilities. Many IoT devices lack adequate security measures, making them easy targets for hackers looking to exploit weak points in a network.

The landscape of cyber threats is constantly evolving, making it essential for businesses in Kenya to stay informed about potential risks. By understanding these threats—ranging from common issues like data breaches and ransomware to emerging challenges like APTs and IoT vulnerabilities—organizations can better prepare themselves against cyber incidents.

As we continue exploring cyber insurance in Kenya, it’s crucial to recognize how these threats influence the need for comprehensive coverage that can safeguard businesses from financial losses associated with cyber incidents. In the next section, we will discuss the role of cyber insurance in risk management and how it can help mitigate these threats effectively.

The Role of Cyber Insurance in Risk Management

In an era where cyber threats are increasingly sophisticated and prevalent, businesses must adopt proactive measures to protect their digital assets. One of the most effective strategies is to invest in cyber insurance. This specialized form of insurance not only provides financial protection against cyber incidents but also plays a crucial role in an organization’s overall risk management strategy. Here’s how cyber insurance works and the benefits it offers to businesses in Kenya.

How Cyber Insurance Works

Cyber insurance policies are designed to cover the financial losses that arise from various cyber incidents. These policies typically include several key components:

Coverage Types:

First-Party Coverage: This protects your own business from losses incurred due to a cyber incident. It may cover costs related to data recovery, business interruption, and notification expenses for affected customers.

Third-Party Coverage: This protects against claims made by third parties, such as customers or business partners, who may suffer losses due to your organization’s data breach or security failure. This coverage often includes legal fees, regulatory fines, and settlements.

Claims Process:

When a cyber incident occurs, the business must notify its insurer as soon as possible. The insurance provider will then assess the situation, investigate the claim, and determine the coverage applicable based on the policy terms. It is essential for businesses to maintain detailed records of all related expenses and actions taken during the incident response.

Benefits of Cyber Insurance

Investing in cyber insurance offers numerous advantages for businesses looking to safeguard their operations against digital threats:

Financial Protection Against Losses:

Cyber incidents can result in significant financial losses. Cyber insurance helps mitigate these losses by covering expenses such as data recovery costs, legal fees, and regulatory fines. For instance, a ransomware attack could cost a business millions in ransom payments and recovery efforts.

Support for Legal Fees and Regulatory Fines:

In the event of a data breach, businesses may face lawsuits from affected customers or regulatory penalties for failing to protect sensitive information. Cyber insurance can cover these legal expenses, providing critical support during challenging times.

Coverage for Data Recovery and Notification Costs:

After a data breach, organizations are often required to notify affected individuals and provide credit monitoring services. Cyber insurance can help cover these notification costs, ensuring compliance with legal requirements while maintaining customer trust.

Access to Expert Resources:

Many cyber insurance providers offer access to cybersecurity experts who can assist businesses in managing incidents effectively. This support can include forensic investigations, public relations assistance, and guidance on improving cybersecurity measures post-incident.

Cyber insurance is an essential component of risk management for businesses operating in Kenya’s digital landscape. By understanding how cyber insurance works and recognizing its benefits, organizations can better prepare themselves for potential cyber incidents.

As we continue our exploration of this topic, it is vital for businesses to consider not only purchasing a policy but also implementing robust cybersecurity measures that complement their insurance coverage. In the next section, we will examine the key features of cyber insurance policies that businesses should be aware of when selecting coverage tailored to their needs.

Key Features of Cyber Insurance Policies

When considering cyber insurance, it is essential for businesses to understand the key features and components of policies available in the market. Not all cyber insurance policies are created equal, and selecting the right coverage can significantly impact how well an organization is protected against cyber threats. Here are the primary features to consider:

Coverage Options

First-Party Coverage:

This type of coverage protects the insured organization from its own losses resulting from a cyber incident. Key components of first-party coverage typically include:

Data Breach Response Costs: Covers expenses related to investigating and responding to a data breach, including forensic analysis and notification costs.

Business Interruption Losses: Compensates for lost income during downtime caused by a cyber incident, such as a ransomware attack that disrupts operations.

Cyber Extortion: Provides coverage for ransom payments demanded by cybercriminals, as well as any associated costs incurred during the negotiation process.

Third-Party Coverage:

This coverage protects against claims made by third parties who suffer losses due to a business’s failure to secure their data. Important aspects include:

Legal Defense Costs: Covers legal fees associated with defending against lawsuits resulting from data breaches or privacy violations.

Regulatory Fines and Penalties: Offers protection against fines imposed by regulatory bodies for non-compliance with data protection regulations, such as the Data Protection Act in Kenya.

Settlement Costs: Covers settlements or judgments awarded to affected parties in lawsuits related to data breaches.

Exclusions and Limitations

While cyber insurance policies provide valuable coverage, it is crucial for businesses to be aware of common exclusions and limitations that may apply:

Pre-existing Conditions:

Policies often exclude coverage for incidents that occurred before the policy was purchased or for known vulnerabilities that were not addressed prior to the incident.

Insider Threats:

Some policies may not cover losses resulting from intentional acts by employees or contractors, depending on the specific terms of the policy.

Acts of War or Terrorism:

Many cyber insurance policies exclude coverage for damages resulting from acts of war or terrorism, which can include large-scale cyberattacks carried out by nation-states.

Policy Limits and Deductibles:

Businesses should pay attention to policy limits, which dictate the maximum amount an insurer will pay for a covered loss. Additionally, deductibles—the amount the insured must pay out-of-pocket before insurance kicks in—can vary between policies.

Understanding the key features of cyber insurance policies is critical for businesses looking to protect themselves against digital threats effectively. By evaluating both first-party and third-party coverage options, as well as being aware of exclusions and limitations, organizations can make informed decisions when selecting a policy that aligns with their specific needs.

As we move forward in our discussion on cyber insurance in Kenya, we will explore factors that businesses should consider when choosing the right policy and how to evaluate insurers effectively. This knowledge will empower organizations to secure comprehensive coverage that enhances their resilience against cyber incidents.

Choosing the Right Cyber Insurance Policy

Selecting the right cyber insurance policy is a critical step for businesses aiming to protect themselves from the growing threat of cyber incidents. With various options available, it’s essential to consider several factors to ensure that the chosen policy aligns with the organization’s specific needs and risk profile. Here are key considerations for businesses in Kenya when selecting a cyber insurance policy:

Factors to Consider When Selecting a Policy

Business Size and Industry-Specific Risks:

Different industries face varying levels of cyber risk. For example, healthcare organizations often deal with sensitive patient data, making them prime targets for data breaches. On the other hand, e-commerce businesses may be more vulnerable to payment fraud. Assessing your business’s size and industry-specific risks can help determine the level of coverage required.

Previous Incidents and Claims History:

Insurers typically evaluate an organization’s claims history when underwriting a policy. Businesses with a history of cyber incidents may face higher premiums or restrictions in coverage. It’s essential to be transparent about past incidents while seeking coverage, as this can influence both the availability and cost of insurance.

Coverage Limits and Deductibles:

Carefully review the coverage limits offered by different policies. Ensure that the limits are sufficient to cover potential losses your business may face in the event of a cyber incident. Additionally, consider the deductibles—higher deductibles may lower premiums but could result in significant out-of-pocket expenses during a claim.

Policy Customization:

Look for insurers that offer customizable policies tailored to your business’s unique needs. This flexibility allows you to add specific coverage options that address particular risks your organization may encounter.

How to Evaluate Insurers

Reputation and Financial Stability:

Research potential insurers thoroughly. Look for companies with a strong reputation in the market and positive reviews from other businesses. Financial stability is also crucial; an insurer must be able to pay claims when needed. You can check ratings from agencies like A.M. Best or Moody’s for insights into an insurer’s financial health.

Customer Service and Claims Support:

Evaluate the level of customer service provided by potential insurers. A responsive claims support team can make a significant difference during stressful situations following a cyber incident. Look for insurers that offer 24/7 support and have a clear claims process.

Expertise in Cyber Insurance:

Choose insurers that specialize in cyber insurance and have experience dealing with cyber incidents similar to those your business may face. Their expertise can provide valuable insights into risk management and loss prevention strategies.

Policy Terms and Conditions:

Carefully read through the terms and conditions of each policy before making a decision. Pay attention to exclusions, limitations, and any requirements for maintaining coverage, such as implementing specific cybersecurity measures.

Choosing the right cyber insurance policy is essential for businesses looking to safeguard their operations against digital threats effectively. By considering factors such as business size, industry-specific risks, previous claims history, and evaluating potential insurers based on reputation and expertise, organizations can make informed decisions that enhance their cybersecurity posture.

As we continue our exploration of cyber insurance in Kenya, we will discuss steps businesses can take to mitigate cyber risks beyond insurance policies, ensuring comprehensive protection against digital threats while fostering a culture of cybersecurity awareness within their organizations.

Steps to Mitigate Cyber Risks Beyond Insurance

While cyber insurance provides essential financial protection against cyber incidents, it should not be the sole strategy for safeguarding a business. Organizations must implement proactive measures to mitigate cyber risks effectively. Here are key steps businesses in Kenya can take to enhance their cybersecurity posture beyond purchasing insurance:

Implementing Strong Cybersecurity Measures

Conduct Regular Risk Assessments:

Regularly assess your organization’s cybersecurity risks to identify vulnerabilities and potential threats. This process involves evaluating your IT infrastructure, data handling practices, and employee behaviors. Tools such as vulnerability scanners and penetration testing can provide valuable insights into areas needing improvement.

Employee Training and Awareness Programs:

Human error is often a leading cause of cyber incidents. Implement comprehensive training programs that educate employees about cybersecurity best practices, including recognizing phishing attempts, using strong passwords, and reporting suspicious activities. According to the Cybersecurity & Infrastructure Security Agency (CISA), organizations that invest in employee training significantly reduce their risk of falling victim to cyber attacks.

Implement Access Controls:

Limit access to sensitive data and systems to only those employees who need it for their job functions. Use role-based access controls (RBAC) to ensure that employees have the minimum necessary access to perform their duties. Regularly review and update access permissions as roles change within the organization.

Utilize Multi-Factor Authentication (MFA):

Implement MFA for all critical systems and applications. MFA adds an extra layer of security by requiring users to provide two or more verification factors before gaining access, making it more challenging for unauthorized individuals to breach accounts.

Developing an Incident Response Plan

Key Components of an Effective Incident Response Plan:

An incident response plan outlines the steps your organization will take in the event of a cyber incident. Key components include:

Preparation: Establishing a response team and defining roles and responsibilities.

Detection and Analysis: Procedures for identifying and assessing incidents promptly.

Containment, Eradication, and Recovery: Steps to contain the incident, eliminate threats, and restore normal operations.

Post-Incident Review: Analyzing the incident to identify lessons learned and improve future responses.

Regular Updates and Drills:

Regularly update your incident response plan to reflect changes in technology, business processes, and emerging threats. Conduct drills or tabletop exercises to simulate incidents and test your team’s readiness. This practice helps ensure that everyone knows their roles during an actual event.

Mitigating cyber risks requires a multifaceted approach that goes beyond relying solely on cyber insurance. By implementing strong cybersecurity measures, conducting regular risk assessments, providing employee training, utilizing access controls, and developing a robust incident response plan, businesses can significantly enhance their resilience against cyber threats.

The Future of Cyber Insurance in Kenya

As the digital landscape continues to evolve, so too does the field of cyber insurance. Businesses in Kenya are increasingly recognizing the importance of protecting themselves against cyber threats, leading to a growing demand for cyber insurance products. However, several trends and challenges are shaping the future of cyber insurance in the country. Here’s an overview of what to expect in the coming years.

Trends Influencing the Cyber Insurance Market

Increased Demand for Cyber Insurance Products:

As cyber threats become more sophisticated and prevalent, businesses are more aware of their vulnerabilities. A survey by PwC indicates that 70% of organizations plan to increase their cybersecurity budgets in response to rising threats. This growing awareness is likely to drive demand for comprehensive cyber insurance policies tailored to specific industry needs.

Integration with Risk Management Solutions:

Insurers are increasingly integrating cyber insurance with broader risk management solutions. This approach allows businesses to not only purchase coverage but also gain access to resources that help them improve their cybersecurity posture. Insurers may offer risk assessments, employee training programs, and incident response planning as part of their services.

Use of Advanced Technologies in Underwriting:

The underwriting process for cyber insurance is evolving with the adoption of advanced technologies such as artificial intelligence (AI) and big data analytics. These tools enable insurers to assess risks more accurately by analyzing a company’s cybersecurity practices, historical data breaches, and external threat landscapes. This trend can lead to more personalized policies and pricing structures based on an organization’s specific risk profile.

Regulatory Developments:

The regulatory environment surrounding data protection and cybersecurity is becoming more stringent globally, including in Kenya. The implementation of laws such as the Data Protection Act 2019 emphasizes the need for businesses to safeguard personal data. As regulations evolve, businesses may be required to obtain cyber insurance as part of compliance efforts, further driving demand for coverage.

Challenges Facing the Industry

Shortage of Cybersecurity Expertise:

One of the significant challenges facing businesses in Kenya is the shortage of cybersecurity professionals. According to a report by Cybersecurity Ventures, there will be an estimated 3.5 million unfilled cybersecurity jobs globally by 2025. In Kenya, this shortage can hinder organizations’ ability to implement effective cybersecurity measures, potentially increasing their reliance on cyber insurance without adequate risk mitigation strategies.

Evolving Threat Landscape: