Vince Oremo is a talented web designer and digital marketer from Kenya, who studied journalism at the Technical University of Kenya. With over six years of experience, he specializes in brand identity, graphic design, web development, SEO, and social media management. Oremo focuses on creating tailored solutions that reflect each client's unique story, enhancing their online presence and driving business growth. His collaborative approach ensures meaningful connections between brands and their audiences, resulting in increased engagement and visibility. You can explore his work at vinceoremo.com.

The healthcare system in Kenya is facing a significant challenge, as highlighted by the recent report from the Rural and Urban Private Hospitals Association of Kenya (RUPHA). The report reveals that 9 out of 10 Kenyans are still paying for medical expenses out of pocket, a situation that underscores the urgent need for reform in healthcare financing.

Current Healthcare Financing Landscape

In Kenya, many citizens rely heavily on out-of-pocket payments for medical services. This trend places a substantial financial burden on families, particularly those in low-income communities. The National Hospital Insurance Fund (NHIF) was established to alleviate some of these costs, but issues such as delayed reimbursements and inadequate funding have hindered its effectiveness. RUPHA has reported that at least Sh29 billion is owed to hospitals in historical debts, with an additional Sh6.9 billion frozen within the NHIF.

Challenges for Healthcare Providers

Healthcare facilities across the country are struggling due to these financial constraints. Many hospitals report a lack of essential medications and resources needed to provide adequate care. Dr. Brian Lishenga, chairman of RUPHA, has noted that several facilities are falling behind on rent and salaries, leading to a precarious situation where some hospitals are unable to operate effectively. The expiration of contracts between healthcare providers and NHIF has further complicated matters, leaving many facilities without the necessary agreements to deliver services.

Impact on Patients

The reliance on out-of-pocket expenses has dire consequences for patients. Many individuals are unable to afford necessary treatments, such as renal dialysis or cancer care, which can lead to worsening health conditions or even preventable deaths. The financial strain caused by high medical costs often forces families to make difficult choices about their health care.

Government Response and Reforms

In response to these challenges, RUPHA has called for a two-year phased transition to the Social Health Insurance Fund (SHIF). This transition aims to create a more structured approach to healthcare financing that could ultimately reduce out-of-pocket expenses for patients. However, recent legal challenges have complicated this process. A ruling declared the Social Health Insurance Act unconstitutional, prompting concerns over the speed and execution of reforms.

Recommendations for Improvement

To stabilize the healthcare sector and improve service delivery, several recommendations have been proposed:

Renewal and Re-negotiation of Contracts: RUPHA advocates for immediate renewal of contracts with NHIF and better reimbursement rates for healthcare providers.

Release of Funds: It is crucial for state agencies that owe money to NHIF to release these funds promptly so that payments can be made to healthcare providers.

Abolishment of Private Health Schemes: Redirecting resources from private health schemes back into NHIF could help alleviate financial pressures on the system.

Conclusion

The findings from RUPHA’s report serve as a wake-up call regarding the state of healthcare financing in Kenya. With most Kenyans still paying out of pocket for medical expenses, it is clear that significant changes are needed to ensure equitable access to healthcare services. Stakeholders must work together—government officials, healthcare providers, and civil society—to address these pressing issues and create a more sustainable healthcare system for all Kenyans.

The ongoing legal battles surrounding SK Macharia and Directline Assurance have become a significant issue in Kenya’s insurance sector, particularly affecting public transport operators. The disputes center on ownership and shareholding, raising concerns about the company’s future and the security of its policyholders.

Background

Directline Assurance was founded in 1998 by Macharia’s late son, John Gichia. Since then, it has grown to dominate the Public Service Vehicle (PSV) insurance market, holding nearly 70% of the sector. However, since mid-2019, the company has faced serious operational challenges due to shareholder disputes. These disputes have led to multiple court cases and have significantly disrupted the company’s ability to provide essential insurance services.

Recent Developments

The legal battles have intensified as Macharia has accused other individuals of attempting a hostile takeover of Directline Assurance. His lawyer, Danstan Omari, claims that Macharia and his wife were unlawfully removed from the company, which has led to a series of court filings aimed at reclaiming control. The Insurance Regulatory Authority (IRA) has also been involved, freezing the company’s accounts and investigating allegations of financial misconduct among former directors.

a. Dispute with CS Mbadi

In a recent session before the National Assembly Finance Committee, Treasury Cabinet Secretary John Mbadi addressed the ongoing disputes. He stated that unresolved shareholding issues have led to Directline Assurance’s suspension, leaving many public transport operators unable to access necessary insurance services. Mbadi noted that the ownership documents are currently held by Macharia, who is recognized as the majority shareholder. However, he also acknowledged misunderstandings regarding shareholding that have complicated matters further.

b. Macharia’s Response

Macharia has strongly denied Mbadi’s claims regarding ownership disputes. He asserts that he is indeed the majority shareholder and has taken legal action to reclaim control over Directline Assurance. His efforts include filing petitions in court and seeking recognition as the rightful owner of the company alongside his wife.

c. Legal Proceedings

The legal landscape surrounding Directline Assurance is complex. Ongoing court cases involve various claims related to ownership and management of the company. Recently, a court ordered Macharia to wire back Sh400 million that he had withdrawn from Directline Assurance, highlighting the contentious nature of these proceedings. The outcome of these cases will be crucial in determining the future operations of Directline Assurance.

Implications for Directline Assurance

The ongoing disputes have severely impacted Directline Assurance’s operations and raised alarms among policyholders. Many are concerned about the validity of their insurance policies amid these legal challenges. Macharia has warned that policies issued under Directline may be at risk due to the company’s operational suspension.

1. Financial Implications

Allegations of mismanagement have surfaced amid these disputes, with claims that former directors embezzled funds from Directline Assurance. Investigations by the IRA and other agencies are underway to address these financial irregularities. The fallout from these allegations could further damage market confidence in Directline Assurance and expose policyholders to significant risks.

2. Market Reactions

The turmoil surrounding Directline Assurance has created uncertainty in the insurance market, affecting stakeholders’ confidence in the company’s stability. Policyholders are particularly vulnerable as they face potential disruptions in their coverage and claims processing.

Conclusion

The conflict involving SK Macharia, CS Mbadi, and the IRA highlights critical issues within Directline Assurance regarding ownership and operational stability. As legal proceedings continue, both policyholders and stakeholders await clarity on the future of this essential insurance provider in Kenya’s PSV sector. A resolution is urgently needed to stabilize operations and protect policyholders who depend on Directline for their insurance needs.

Securing your child’s education is a top priority for many parents. With the rising costs of schooling in Kenya, finding effective ways to ensure your child has access to quality education is crucial. One of the best solutions is education insurance. This guide will help you understand how to choose the right education insurance policy for your child in Kenya, ensuring you make an informed decision that protects their educational future.

Understanding Education Insurance

What is Education Insurance?

Education insurance is a financial product designed to help parents save for their children’s future educational expenses. Unlike regular life insurance or savings plans, education insurance combines both savings and protection. It ensures that funds are available for educational purposes, such as tuition fees and school supplies, even if something unexpected happens, like the death or disability of a parent.

Key Features of Education Insurance Policies

When looking at education insurance policies, it’s important to know their key features:

Savings Component: This allows parents to build up funds over time that can be used for their child’s education.

Life Cover: If the policyholder passes away, the policy ensures that the child’s educational expenses are still covered.

Flexible Premium Payments: Many policies let you choose how often you pay premiums—monthly, quarterly, or annually—so you can select what fits your budget best.

Additional Riders: Some policies offer extra benefits like coverage for critical illness or disability, providing more security.

Why You Need Education Insurance for Your Child

a. Financial Security

One of the main reasons to consider education insurance is financial security. If a parent dies or becomes disabled, education insurance guarantees that funds will still be available for the child’s schooling. This safety net can prevent children from having to drop out of school due to sudden financial difficulties.

b. Long-term Savings

Starting early with an education insurance policy helps parents save money over time. As education costs continue to rise—often faster than inflation—having a dedicated savings plan can ease future financial stress. For example, recent statistics show that educational expenses in Kenya have increased significantly over the past decade, making long-term savings essential.

c. Protection Against Inflation

Inflation can greatly affect future expenses. Education insurance policies often include features that adjust benefits according to inflation rates, ensuring that your savings maintain their value over time.

Factors to Consider When Choosing an Education Insurance Policy

1. Assess Your Child’s Educational Needs

Before picking a policy, think about your child’s current and future educational needs. Are you saving for primary school, secondary school, or university? Each level has different costs and timelines.

2. Evaluate Your Financial Situation

Understanding your finances is crucial. Look at your current income and see how much you can comfortably spend on premiums without straining your budget.

3. Inflation and Cost Projections

Projecting future educational costs is vital when choosing a policy. Research current tuition rates and think about how they might rise over time. This will help you set realistic savings goals through your education insurance policy.

Policy Features and Benefits

When comparing policies, pay attention to specific features:

Coverage Amount: Make sure the coverage matches what you expect to spend on your child’s education.

Premium Flexibility: Look for policies that offer flexible payment options based on your financial situation.

Bonus Structures: Some policies provide bonuses at maturity or for continuous premium payments; understanding these can enhance your savings.

Top Education Insurance Providers in Kenya

Several reputable providers offer education insurance policies tailored to meet various needs:

Britam Insurance

Offers the Britam Super Education Plus Policy, which combines savings with insurance protection.

Minimum monthly premium starts at Ksh 3,000.

Cash bonuses payable for the last six consecutive years before maturity.

Jubilee Insurance

The Career Life Plus Plan provides flexible benefits based on sum assured and chosen policy term (5-20 years).

Offers accident and disability cover alongside education savings.

CIC Insurance Group

Their Academia Policy waives premium payments in case of a parent’s demise while ensuring funds remain available for the child’s education.

Monthly premiums start as low as Ksh 3,000.

Old Mutual

The Rafiki Halisi Plan focuses on long-term savings with additional life cover.

Offers various investment options alongside educational coverage.

These providers not only offer diverse plans but also ensure that parents have multiple options tailored to their specific needs.

How to Compare Education Insurance Policies Effectively

a. Comparing Quotes for Education Insurance Policies

When choosing the right education insurance policy for your child, comparing quotes from different providers is essential. This process allows you to evaluate various plans, coverage amounts, and premium costs, ensuring you find the best option that fits your family’s needs and budget.

Companies like Step by Step Insurance offer free quote comparisons, helping you navigate through the available options. They partner with top-tier insurance providers to ensure you receive the best coverage possible. By utilizing their services, you can make informed decisions and choose the right partners for your education insurance needs.

Taking advantage of these resources can simplify the decision-making process and provide peace of mind as you secure your child’s educational future.

b. Create a Comparison Chart

When evaluating different policies, it helps to create a comparison chart that outlines key features side by side:

Responsive Table

Provider

Coverage Amount

Premium Payment Options

Additional Benefits

Britam

Ksh 3 million

Monthly/Annual

Cash bonuses

Jubilee

Flexible

Monthly/Quarterly

Accident cover

CIC

Ksh 2 million

Monthly

Waived premiums upon demise

Old Mutual

Variable

Flexible

Investment options

c. Read Customer Reviews and Testimonials

Customer feedback can provide valuable insights into each provider’s reliability and service quality. Look for reviews on reputable websites or forums where current policyholders share their experiences. Hearing from others who have navigated similar choices can help guide your decision-making process.

Common Questions About Education Insurance Policies

What happens if I miss a premium payment?

If you miss a premium payment, most policies offer a grace period during which you can still make payments without losing coverage. However, if payments are not made within this period, your policy may lapse. Always check with your provider about their specific grace period policies.

Can I change my education insurance policy later?

Yes! Many providers allow you to modify your policy as your needs change. This could include adjusting coverage amounts or adding riders based on new circumstances in your life.

Is education insurance worth the investment?

Education insurance can be a valuable investment for parents looking to secure their child’s future. It provides financial protection and peace of mind against unforeseen circumstances that could disrupt educational plans.

Conclusion

Choosing the right education insurance policy for your child in Kenya is an important step toward securing their educational future amid rising costs and uncertainties. By understanding the key features of these policies and evaluating your family’s needs and financial situation, you can make an informed decision that ensures your child receives quality education regardless of life’s challenges.

For personalized guidance or further information about specific policies, consider consulting with an insurance advisor who can help tailor a plan suited to your family’s unique situation.

Heritage Insurance Company has recently appointed Rosalyn Mugoh as the new Managing Director, marking a significant shift in the company’s leadership. This change comes at a crucial time as the organization seeks to bolster its market presence and enhance operational efficiency in a competitive insurance landscape.

This article will explore the implications of this leadership transition, the strategic goals of Heritage Insurance under Mugoh’s direction, and the broader context of the insurance industry in Kenya.

Background of Heritage Insurance

Founded as a subsidiary of Liberty Kenya Insurance, Heritage Insurance is a prominent player in Kenya’s non-life insurance sector. The company is backed by Liberty Holdings Limited, which operates across 25 countries in Africa and is majority-owned by Standard Bank Group Limited, the largest African banking group by assets. Heritage Insurance has built its reputation on providing innovative and customer-centric services, particularly in motor insurance and micro-insurance.

Challenges Faced by Heritage Insurance

The company has navigated various challenges over the years, particularly during the COVID-19 pandemic, which drastically altered consumer behavior and market dynamics. With restrictions limiting movement, there was a notable decline in vehicle usage among insured motorists, leading to increased customer concerns regarding premium payments. In response, Heritage Insurance adapted its services to maintain customer satisfaction while ensuring operational efficiency.

Rosalyn Mugoh’s Vision and Strategic Goals

Rosalyn Mugoh

a. Enhancing Market Presence

Under Rosalyn Mugoh’s leadership, Heritage Insurance aims to strengthen its market presence through strategic initiatives that focus on innovation and technology integration. The company plans to leverage advanced technologies such as telematics and APIs to improve service delivery and customer experience. This includes launching innovative products like usage-based insurance policies that adjust premiums according to driving behavior.

b. Operational Efficiency

Mugoh’s appointment comes with an emphasis on enhancing operational efficiency. The implementation of the TurnQuest General Insurance platform has already shown promising results by streamlining operations and improving customer service capabilities. This platform allows for better management of resources and enables Heritage to expand its reach into underserved regions while maintaining control over operations.

c. Fostering Innovation

Innovation will be a cornerstone of Mugoh’s strategy. By fostering a culture that embraces technological advancements and new product development, Heritage aims to remain competitive in an evolving market. This includes exploring micro-insurance offerings and enhancing customer experience through personalized services.

d. Industry Context

The Kenyan insurance market is characterized by intense competition and evolving regulatory requirements. Companies are increasingly focusing on digital transformation to meet changing customer expectations and improve service delivery. Analysts predict that Heritage Insurance’s revenue could grow by approximately 9.9% annually over the next three years, driven by strategic underwriting initiatives and investments in technology. However, challenges remain, including managing operational costs and ensuring compliance with regulatory standards.

Competitive Landscape

Heritage Insurance faces competition from both established players and new entrants in the market. To maintain its competitive edge, the company must continue to innovate while also addressing potential risks associated with over-reliance on specific segments or geographic areas for growth. The company’s focus on commercial lines and Excess & Surplus (E&S) products may limit diversification but could enhance profitability if managed effectively.

Regulatory Environment

The regulatory landscape for insurance companies in Kenya is dynamic, requiring continuous adaptation to ensure compliance while pursuing growth objectives. Heritage Insurance’s ability to navigate these challenges will be crucial for its long-term success under Mugoh’s leadership.

Future Outlook

Looking ahead, Heritage Insurance is poised for growth under Rosalyn Mugoh’s leadership. The company’s commitment to innovation, operational efficiency, and enhanced customer experience positions it well within the competitive insurance landscape. As it continues to implement strategic initiatives aimed at expanding its market presence and improving profitability, Heritage Insurance will likely play a pivotal role in shaping the future of non-life insurance in Kenya.

Conclusion

The appointment of Rosalyn Mugoh as Managing Director represents a strategic move for Heritage Insurance as it seeks to enhance its operational capabilities and market presence. With a focus on innovation and efficiency, the company is well-equipped to navigate the challenges of the insurance industry while meeting the evolving needs of its customers.

As Heritage Insurance embarks on this new chapter under Mugoh’s guidance, it remains committed to delivering quality services and maintaining its reputation as a leader in the Kenyan insurance sector.

In today’s digital landscape, where technology plays an integral role in business operations, the threat of cyberattacks looms larger than ever. Cyber insurance has emerged as a critical tool for small businesses in Kenya, providing essential protection against the financial repercussions of data breaches and cyber incidents.

As the reliance on digital infrastructure grows, so does the need for robust risk management strategies, making understanding how small businesses in Kenya benefit from cyber insurance more important than ever.

What is Cyber Insurance?

Cyber insurance, also known as cyber liability insurance, is a type of coverage designed to protect businesses from financial losses resulting from cyberattacks or data breaches. This insurance can cover a variety of incidents, including malware attacks, phishing scams, ransomware incidents, and denial-of-service attacks. For small businesses in Kenya, where digital transactions and online services are increasingly common, having a cyber insurance policy can mean the difference between recovery and financial ruin following a cyber incident.

The increasing frequency of cyberattacks is alarming. According to data from the Central Bank of Kenya (CBK), hacking incidents targeting financial institutions rose nearly three-fold to 444 million in the year ending June 2022. This surge highlights the urgent need for small businesses to safeguard their operations through effective risk management solutions like cyber insurance.

Overview of Increasing Cyber Threats

Small businesses are particularly vulnerable to cyber threats due to limited resources and cybersecurity expertise. A report by Kaspersky indicates that small businesses in Kenya experienced a 47% increase in cyberattacks in 2022. Unfortunately, many business owners remain unaware of the risks they face; over 90% reportedly do not recognize their exposure to growing cyber threats. This lack of awareness can lead to devastating consequences when an attack occurs.

By investing in cyber insurance, small businesses can not only protect themselves financially but also enhance their overall cybersecurity posture through access to risk management services often included in these policies. This introduction sets the stage for understanding how small businesses in Kenya benefit from cyber insurance by defining key terms and highlighting the relevance of this coverage in the context of increasing cyber threats.

The Importance of Cyber Insurance for Small Businesses

Why Do Small Businesses Need Cyber Insurance?

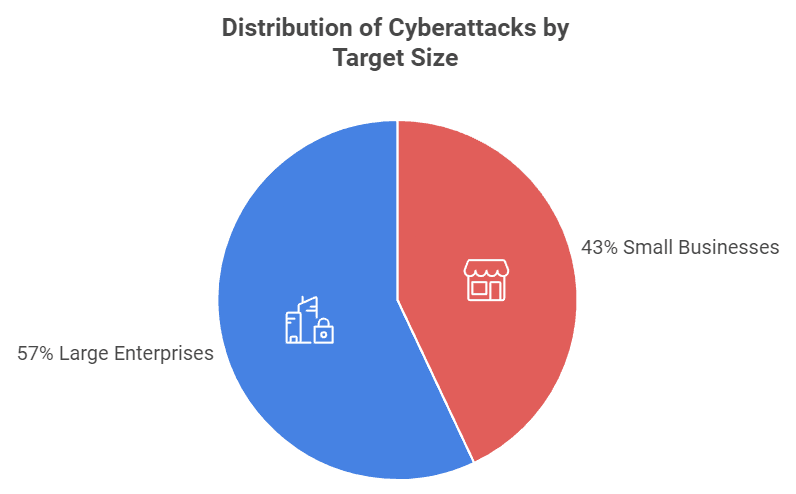

The necessity of cyber insurance for small businesses in Kenya cannot be overstated. As digital operations become more prevalent, so do the risks associated with them. Many small business owners mistakenly believe that they are not targets for cybercriminals, but this is a dangerous misconception. In fact, 43% of cyberattacks target small businesses, according to a report by Verizon. This statistic underscores the vulnerability of smaller enterprises, which often lack the resources to implement comprehensive cybersecurity measures.

Distribution of Cyberattacks by Target Size

Statistics on Cyberattacks Targeting Small Businesses in Kenya

47% increase in cyberattacks on small businesses in Kenya in 2022.

Over 90% of small business owners are unaware of their exposure to cyber threats.

The average cost of a data breach for small businesses can reach up to $200,000, which can be devastating for those operating on tight margins.

The Financial Impact of Cyberattacks

The financial repercussions of a cyberattack can be catastrophic for small businesses. A data breach not only incurs immediate costs—such as forensic investigations, legal fees, and public relations efforts—but also long-term damages, including loss of customer trust and potential regulatory fines.

For example, in 2021, a small retail business in Nairobi suffered a significant data breach that exposed customer payment information. The incident led to a $150,000 loss due to legal fees and compensation claims from affected customers. Additionally, the business experienced a 30% drop in sales over the following months as customers lost trust in their ability to protect sensitive information.

Conclusion: The Need for Proactive Measures

Given the alarming statistics and real-world consequences of cyber incidents, it is clear that small businesses in Kenya must prioritize cybersecurity. Cyber insurance serves as a vital safety net that not only protects against financial losses but also helps businesses recover more quickly from incidents. By understanding the importance of cyber insurance, small business owners can take proactive steps to safeguard their operations and ensure long-term sustainability. This section emphasizes the critical need for cyber insurance among small businesses in Kenya by presenting relevant statistics and real-life examples that illustrate the potential financial impact of cyberattacks.

Types of Cyber Insurance Coverage Available

Understanding the types of cyber insurance coverage available is essential for small businesses in Kenya as they seek to protect themselves from potential cyber threats. Cyber insurance policies typically fall into two main categories: first-party coverage and third-party coverage. Each type offers distinct benefits that can be tailored to the specific needs of a business.

a. First-Party Coverage

First-party coverage is designed to protect a business from direct losses incurred as a result of a cyber incident. This type of coverage typically includes:

Data Restoration Costs: Coverage for expenses related to restoring lost or compromised data, including hiring forensic experts to recover data.

Business Interruption Losses: Compensation for lost income during the downtime caused by a cyber incident, ensuring that the business can continue to operate after an attack.

Cyber Extortion: Protection against ransomware attacks, including costs associated with paying ransoms and negotiating with cybercriminals.

Notification Costs: Expenses related to notifying affected customers and stakeholders about a data breach, which may be required by law.

For example, if a small e-commerce business experiences a ransomware attack that locks them out of their systems, first-party coverage can help cover the costs of data recovery and any lost revenue during the downtime.

b. Third-Party Coverage

Third-party coverage protects businesses from liabilities arising from claims made by customers, partners, or other third parties affected by a cyber incident. This type of coverage typically includes:

Legal Defense Costs: Coverage for legal fees incurred when defending against lawsuits related to data breaches or privacy violations.

Regulatory Fines and Penalties: Protection against fines imposed by regulatory bodies for failing to protect customer data or comply with data protection laws.

Settlements and Damages: Compensation for settlements or damages awarded to third parties as a result of a data breach.

For instance, if a small accounting firm inadvertently exposes client financial information due to a cyberattack, third-party coverage would help cover the legal fees and any potential settlements resulting from lawsuits filed by affected clients.

c. Combined Coverage

Many insurers offer combined policies that include both first-party and third-party coverage. This comprehensive approach allows small businesses to have robust protection against various risks associated with cyber incidents. By opting for combined coverage, businesses can ensure they are safeguarded against both direct losses and liabilities arising from third-party claims.

Conclusion: Tailoring Coverage to Business Needs

When considering cyber insurance, small businesses in Kenya should assess their unique risks and operational needs. Understanding the differences between first-party and third-party coverage is crucial for selecting the right policy. By tailoring their insurance coverage appropriately, small businesses can effectively mitigate potential financial losses stemming from cyber incidents. This section provides an in-depth look at the various types of cyber insurance coverage available to small businesses in Kenya, highlighting their specific benefits and real-world applications.

Key Benefits of Cyber Insurance for Small Businesses

Cyber insurance offers a multitude of benefits that can significantly enhance the resilience and sustainability of small businesses in Kenya. As cyber threats continue to evolve, having a comprehensive insurance policy can provide peace of mind and financial security. Here are some of the key advantages that small businesses can gain from investing in cyber insurance.

Financial Protection

One of the primary benefits of cyber insurance is its ability to provide financial protection against the significant costs associated with cyber incidents. The average cost of a data breach for small businesses can be staggering, often exceeding $200,000 when factoring in legal fees, regulatory fines, and lost revenue. Cyber insurance helps mitigate these costs by covering:

Data recovery expenses, including forensic investigations.

Business interruption losses, ensuring that income is preserved during downtime.

Cyber extortion payments in cases of ransomware attacks.

For example, a small hotel in Kenya that falls victim to a cyberattack may incur substantial costs related to data recovery and customer notification. With cyber insurance, these expenses could be covered, allowing the business to recover more quickly without crippling financial strain.

Legal Support and Compliance

As data protection regulations become more stringent globally, small businesses must navigate complex legal landscapes. Cyber insurance provides essential legal support by covering:

Legal fees associated with defending against lawsuits resulting from data breaches.

Regulatory fines imposed by authorities for non-compliance with data protection laws such as the Data Protection Act in Kenya.

By having a robust cyber insurance policy, small businesses can ensure they are prepared for potential legal challenges arising from cyber incidents. This support not only protects their finances but also helps maintain compliance with evolving regulations.

Risk Management Services

Many cyber insurance policies offer additional risk management services designed to enhance a business’s cybersecurity posture. These services may include:

Cybersecurity assessments to identify vulnerabilities within the organization.

Employee training programs focused on recognizing phishing attempts and other cyber threats.

Incident response planning to ensure a swift and effective reaction to potential breaches.

For instance, a small manufacturing company could benefit from risk management services that help them identify weak points in their cybersecurity strategy, thereby reducing the likelihood of a successful attack.

Business Continuity

In the event of a cyber incident, maintaining business continuity is crucial for minimizing disruption and financial loss. Cyber insurance plays a vital role in ensuring that businesses can recover quickly and resume operations. Coverage for business interruption losses allows companies to continue functioning even when their systems are compromised.For example, if a small retail store experiences a data breach that disrupts its online sales platform, cyber insurance can help cover lost revenue during the downtime while also funding recovery efforts.

Conclusion: Empowering Small Businesses

The benefits of cyber insurance extend far beyond mere financial protection. By providing legal support, risk management services, and ensuring business continuity, cyber insurance empowers small businesses in Kenya to navigate the complexities of the digital landscape with confidence. Investing in this coverage not only safeguards against potential losses but also fosters a proactive approach to cybersecurity. This section outlines the key benefits of cyber insurance for small businesses in Kenya, emphasizing financial protection, legal support, risk management services, and business continuity.

Understanding the Cost of Cyber Insurance

When considering cyber insurance, small businesses in Kenya must also understand the associated costs. The price of a cyber insurance policy can vary widely based on several factors, including the size of the business, the level of coverage required, and the specific risks faced by the industry. This section will explore these factors and provide insights into what small businesses can expect regarding premiums.

Factors Influencing Premium Costs

Several key factors influence the cost of cyber insurance premiums for small businesses:

Business Size: Larger businesses with more extensive operations and higher revenue may face higher premiums due to increased exposure to risk. Conversely, smaller businesses may benefit from lower rates, but they still need adequate coverage to protect against potential losses.

Industry Type: Certain industries are more prone to cyber threats than others. For example, businesses in finance, healthcare, and e-commerce often face higher premiums due to the sensitive nature of the data they handle. In contrast, a small retail store might have lower premiums but still needs coverage for potential risks.

Coverage Limits: The amount of coverage a business chooses will directly impact its premium. Higher coverage limits generally lead to higher costs. Small businesses should carefully assess their needs to strike a balance between adequate protection and affordability.

Claims History: A business’s history of previous claims can significantly affect its premium. Companies that have experienced multiple cyber incidents may face higher rates as insurers perceive them as higher risk.

Security Measures in Place: Insurers often evaluate the cybersecurity measures a business has implemented when determining premiums. Businesses that invest in robust cybersecurity practices—such as firewalls, encryption, and employee training—may qualify for lower rates due to reduced risk exposure.

Average Cost Range for Small Businesses in Kenya

While specific costs can vary widely, small businesses in Kenya can expect to pay anywhere from KES 30,000 to KES 200,000 annually for cyber insurance premiums, depending on the factors mentioned above. For example:

A small retail shop with minimal online transactions might pay around KES 30,000 for basic coverage.

A mid-sized e-commerce business handling sensitive customer data could see premiums rise to KES 100,000 or more, especially if they require extensive coverage.

It’s important for small business owners to shop around and compare quotes from different insurance providers to find the best policy that meets their needs and budget.

Conclusion: Budgeting for Cyber Insurance

Understanding the cost of cyber insurance is crucial for small businesses looking to safeguard themselves against cyber threats. By considering various factors that influence premiums and being aware of average costs, business owners can make informed decisions about their insurance needs. Investing in cyber insurance is not just an expense; it is a strategic move towards protecting their business’s future in an increasingly digital world. This section provides an overview of the costs associated with cyber insurance for small businesses in Kenya, detailing the factors that influence premiums and offering average cost ranges.

Challenges Small Businesses Face in Obtaining Cyber Insurance

While cyber insurance offers significant benefits, small businesses in Kenya often encounter various challenges when trying to obtain coverage. Understanding these obstacles can help business owners navigate the process more effectively and ensure they secure the protection they need. This section will explore common challenges and provide insights on how to overcome them.

Lack of Awareness and Understanding

One of the most significant hurdles small businesses face is a lack of awareness regarding cyber insurance and its importance. Many business owners do not fully understand what cyber insurance entails or how it can protect them from potential risks. This lack of knowledge can lead to hesitancy in pursuing coverage.To address this challenge, small businesses should invest time in educating themselves about cyber insurance. Resources such as industry reports, webinars, and consultations with insurance professionals can provide valuable insights. Additionally, engaging with local business associations or chambers of commerce can help raise awareness about the importance of cybersecurity and insurance.

Navigating the Application Process

The application process for cyber insurance can be complex and intimidating, especially for small business owners who may not have experience with insurance policies. Insurers typically require detailed information about a business’s operations, security measures, and previous claims history. This requirement can be overwhelming for those without a dedicated risk management team.To simplify the application process, small businesses should:

Prepare Thorough Documentation: Gather relevant information about current cybersecurity measures, employee training programs, and any past incidents. This preparation will help demonstrate to insurers that the business takes cybersecurity seriously.

Consult with Insurance Brokers: Working with an experienced insurance broker can streamline the process. Brokers can help small businesses understand their options, navigate complex policy language, and find coverage that meets their needs.

Affordability Concerns

Another challenge is the perception that cyber insurance is too expensive for small businesses operating on tight budgets. While premiums can vary significantly based on several factors, many small business owners may overlook the long-term cost savings that come with having coverage.To address affordability concerns:

Assess Risk vs. Cost: Business owners should evaluate the potential financial impact of a cyber incident compared to the cost of insurance. Understanding that a single data breach could result in losses far exceeding the annual premium may shift perspectives on affordability.

Explore Multiple Quotes: Small businesses should obtain quotes from various insurers to compare coverage options and pricing. This approach allows them to find a policy that fits their budget while still providing adequate protection.

Conclusion: Overcoming Challenges

While challenges exist in obtaining cyber insurance, small businesses in Kenya can take proactive steps to navigate these obstacles effectively. By increasing awareness, preparing for the application process, and understanding the value of coverage relative to potential losses, business owners can secure essential protection against cyber threats. Ultimately, overcoming these challenges is crucial for ensuring long-term business resilience in an increasingly digital landscape. This section discusses the common challenges small businesses face when seeking cyber insurance and provides actionable strategies for overcoming these obstacles.

How to Choose the Right Cyber Insurance Policy

Selecting the appropriate cyber insurance policy is a critical step for small businesses in Kenya looking to protect themselves from cyber threats. With various options available, it’s essential to understand how to evaluate policies effectively. This section will guide business owners through the process of choosing the right coverage tailored to their specific needs.

Assessing Your Business Needs

Before diving into policy comparisons, small business owners should conduct a thorough assessment of their unique risks and operational requirements. Here are key considerations to keep in mind:

Identify Specific Risks: Evaluate the types of data your business handles (e.g., customer personal information, payment details) and the potential vulnerabilities in your operations. For instance, a small retail business with an online store may face different risks compared to a local service provider.

Understand Regulatory Requirements: Familiarize yourself with any legal obligations related to data protection in Kenya, such as the Data Protection Act. Compliance with these regulations can influence the type of coverage needed.

Determine Coverage Needs: Consider what aspects of cyber incidents you want to be covered. Do you need protection against data breaches, cyber extortion, or business interruption? Identifying your priorities will help narrow down policy options.

Comparing Different Providers

Once you have a clear understanding of your needs, it’s time to compare policies from various insurance providers. Here are some steps to ensure you make an informed choice:

Research Insurers: Look for reputable insurance companies that specialize in cyber insurance. Check their financial stability and customer reviews to gauge their reliability.

Request Detailed Quotes: Obtain quotes from multiple insurers and ensure that they include comprehensive details about coverage limits, exclusions, and premium costs. This information will allow for an apples-to-apples comparison.

Evaluate Policy Terms: Carefully read through the policy terms and conditions. Pay attention to coverage limits, deductibles, and any exclusions that may affect your business in case of a claim.

Ask Questions: Don’t hesitate to reach out to insurers or brokers with questions about policy specifics or terms you don’t understand. Clarifying these points can prevent misunderstandings later on.

Engaging with Insurance Brokers

Working with an experienced insurance broker can significantly simplify the process of selecting a cyber insurance policy. Brokers can provide valuable insights into the market and help tailor coverage options based on your business needs. Here’s how brokers can assist:

Expert Guidance: Brokers have expertise in navigating the complexities of cyber insurance and can help identify suitable policies based on your risk profile.

Negotiation Power: Brokers often have established relationships with insurers, which can lead to better terms and pricing for your coverage.

Ongoing Support: A good broker will not only help you select a policy but also provide ongoing support throughout the life of the insurance, including assistance during claims processing.

Conclusion: Making an Informed Decision

Choosing the right cyber insurance policy requires careful consideration and thorough research. By assessing specific business needs, comparing different providers, and potentially engaging with an insurance broker, small businesses in Kenya can secure coverage that effectively mitigates risks associated with cyber threats. This proactive approach is essential for ensuring long-term resilience in an increasingly digital world. This section provides guidance on how small businesses can choose the right cyber insurance policy by assessing their needs, comparing providers, and utilizing brokers’ expertise.

Real-Life Examples of Cyber Insurance in Action

Understanding the practical implications of cyber insurance can be greatly enhanced by examining real-life case studies. These examples illustrate how small businesses in Kenya have successfully utilized cyber insurance to mitigate the impact of cyber incidents, recover from breaches, and reinforce their cybersecurity strategies. Here are two compelling case studies that highlight the benefits and effectiveness of cyber insurance.

Case Study 1: A Small Retail Business

Background: A small retail business in Nairobi, which operated both a physical store and an online platform, experienced a significant data breach when hackers gained access to its customer database. The breach exposed sensitive customer information, including names, addresses, and payment details.Incident: The cyberattack occurred during a peak shopping season, leading to immediate concerns about customer trust and financial losses. The business faced potential lawsuits from affected customers and regulatory scrutiny for failing to protect sensitive data.Response: Fortunately, the retail business had invested in a comprehensive cyber insurance policy that included both first-party and third-party coverage. This policy provided:

Data Restoration Costs: The insurance covered the expenses associated with forensic investigations to determine the breach’s scope and restore compromised data.

Business Interruption Losses: The policy compensated for lost revenue during the downtime caused by the incident, allowing the business to maintain financial stability.

Legal Defense Costs: The insurance covered legal fees associated with defending against lawsuits filed by affected customers.

Outcome: With the support of their cyber insurance policy, the retail business was able to recover quickly from the incident. They restored their systems within a week and launched a customer notification campaign to inform affected individuals. As a result, they managed to rebuild customer trust and resumed operations with improved cybersecurity measures in place.

Case Study 2: A Local Service Provider

Background: A small IT service provider based in Mombasa experienced a ransomware attack that encrypted critical business files and demanded a ransom payment for decryption keys. The attack not only disrupted operations but also threatened client projects and deadlines.Incident: Faced with the prospect of losing access to vital data, the service provider needed to act quickly. They had previously recognized their vulnerability and secured a cyber insurance policy that included coverage for ransomware attacks.Response: Thanks to their cyber insurance policy, the service provider received immediate support in several areas:

Cyber Extortion Coverage: The policy covered the ransom payment demanded by cybercriminals, allowing the business to regain access to its files without incurring significant out-of-pocket costs.

Incident Response Services: The insurer provided access to cybersecurity experts who helped assess the attack’s impact, implement security measures to prevent future incidents, and develop an incident response plan.

Legal Assistance: The policy also included legal support to navigate compliance issues related to data protection laws following the attack.

Outcome: With the assistance of their cyber insurance policy, the service provider was able to recover from the ransomware attack without crippling financial losses. They implemented stronger cybersecurity protocols as recommended by their insurer and regained client confidence by demonstrating their commitment to protecting sensitive information.

Conclusion: Learning from Real-Life Experiences

These case studies illustrate how small businesses in Kenya can benefit significantly from having cyber insurance in place. By providing financial protection, legal support, and access to expert resources, cyber insurance enables businesses to respond effectively to cyber incidents. As cyber threats continue to evolve, investing in such coverage becomes increasingly essential for ensuring long-term resilience and success in a digital world. This section presents real-life examples of how small businesses in Kenya have successfully utilized cyber insurance during cyber incidents. These case studies highlight the practical benefits of having coverage in place.

The Future of Cyber Insurance for Small Businesses in Kenya

As the digital landscape continues to evolve, so too does the importance of cyber insurance for small businesses in Kenya. With increasing reliance on technology and growing cyber threats, the future of cyber insurance is poised for significant transformation. This section will explore emerging trends, the role of technology in enhancing cybersecurity, and what small businesses can expect in the coming years.

Trends in the Cyber Insurance Market

Increased Demand for Coverage: As awareness of cyber threats grows, more small businesses are recognizing the need for cyber insurance. The demand for coverage is expected to rise sharply, especially as regulatory requirements become more stringent. Businesses that previously overlooked cyber insurance are now seeking policies to protect themselves from potential financial losses.

Tailored Policies for Small Businesses: Insurers are increasingly offering tailored policies specifically designed for small businesses. These policies take into account the unique risks faced by smaller enterprises and provide more relevant coverage options at competitive prices. This trend will make it easier for small businesses to find suitable insurance solutions.

Integration of Cybersecurity Services: Many insurers are beginning to bundle cybersecurity services with their insurance policies. This integration may include risk assessments, employee training programs, and incident response planning, providing small businesses with not just financial protection but also practical resources to enhance their cybersecurity posture.

Data-Driven Underwriting: The use of data analytics in underwriting is becoming more prevalent in the cyber insurance market. Insurers are leveraging data to assess risk more accurately, which can lead to more personalized premiums based on a business’s specific cybersecurity measures and claims history.

The Role of Technology in Enhancing Cybersecurity

Technology plays a crucial role in shaping the future of cyber insurance and enhancing overall cybersecurity for small businesses:

Advanced Threat Detection: Innovations in artificial intelligence (AI) and machine learning are enabling businesses to detect and respond to threats more effectively. These technologies can analyze patterns and identify anomalies that may indicate a cyber threat, allowing businesses to take proactive measures before an incident occurs.

Cloud-Based Solutions: Many small businesses are migrating to cloud-based solutions that offer enhanced security features. These solutions often include built-in protections against data breaches and ransomware attacks, reducing overall risk exposure.

Cybersecurity Training Tools: As human error remains a leading cause of security breaches, technology-driven training tools are becoming essential. Interactive training programs can help employees recognize phishing attempts and other cyber threats, fostering a culture of cybersecurity awareness within organizations.

What Small Businesses Can Expect

As the cyber insurance landscape evolves, small businesses in Kenya should prepare for several key developments:

Greater Accessibility: With increased competition among insurers and a growing recognition of the importance of cybersecurity, small businesses can expect more accessible and affordable cyber insurance options.

Emphasis on Risk Management: Insurers will likely place greater emphasis on risk management practices when underwriting policies. Small businesses that demonstrate strong cybersecurity measures may benefit from lower premiums and better coverage terms.

Ongoing Education and Support: The relationship between insurers and policyholders is expected to become more collaborative. Insurers will increasingly offer ongoing education and support to help small businesses stay informed about emerging threats and best practices for cybersecurity.

Conclusion: Preparing for the Future

The future of cyber insurance for small businesses in Kenya looks promising as awareness grows and coverage options expand. By staying informed about emerging trends and leveraging technology to enhance their cybersecurity posture, small business owners can position themselves effectively in an increasingly digital world. Investing in cyber insurance not only provides financial protection but also fosters resilience against evolving cyber threats. This section discusses the future of cyber insurance for small businesses in Kenya, highlighting emerging trends, technological advancements, and what business owners can expect moving forward.

In recent years, the banking and insurance sectors in Kenya have witnessed a significant transformation, with banks increasingly entering the insurance market through a model known as bancassurance. This innovative partnership allows banks to sell insurance products alongside their traditional financial services, effectively diversifying their offerings and enhancing customer loyalty.

Currently, bancassurance accounts for approximately 10% of the insurance market in Kenya, reflecting a growing trend driven by the insuring of vehicles, loans, and mortgages. This article delves into the rise of bancassurance in Kenya, exploring its benefits, current market dynamics, and the factors fueling its growth.

Understanding Bancassurance

Definition of Bancassurance

Bancassurance is a strategic alliance between banks and insurance companies that enables banks to distribute insurance products to their customers. This partnership allows banks to leverage their existing customer base and distribution channels to offer a range of insurance products, including life, health, property, and motor insurance. By integrating insurance into their service portfolio, banks can provide a more comprehensive financial solution to their clients.

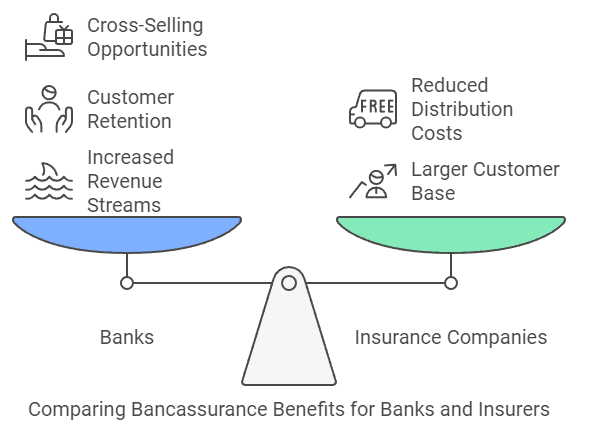

Benefits of Bancassurance for Banks

Increased Revenue Streams: Bancassurance provides banks with an additional source of income through commissions earned on insurance sales. This diversification helps banks mitigate risks associated with fluctuations in traditional banking revenue.

Customer Retention: By offering a one-stop-shop for financial services, banks enhance customer loyalty. Clients are more likely to stay with a bank that meets multiple financial needs, including insurance.

Cross-Selling Opportunities: Banks can utilize their existing relationships with customers to cross-sell insurance products. For instance, when a customer applies for a loan or mortgage, the bank can offer relevant insurance products simultaneously.

Benefits of Bancassurance for Insurance Companies

Access to a Larger Customer Base: Insurance companies benefit from banks’ extensive networks and customer databases, allowing them to reach more potential clients than they could through traditional distribution channels.

Reduced Distribution Costs: By partnering with banks, insurers can lower their marketing and distribution expenses. Banks already have established infrastructure and client relationships that insurers can leverage.

Current State of the Insurance Market in Kenya

Overview of the Kenyan Insurance Market

The Kenyan insurance market has experienced steady growth over the past decade. As of 2023, the market is valued at approximately KES 300 billion (around USD 2.5 billion), with various segments including life insurance, health insurance, and general insurance contributing to this figure. The penetration rate remains low compared to global standards; however, there is significant potential for growth as awareness increases and new products are introduced.

Role of Banks in the Insurance Market

Historically, banks in Kenya have engaged with the insurance sector primarily through referrals or partnerships without significant involvement in selling policies directly. However, recent trends indicate a shift toward active participation in bancassurance as banks recognize the potential for increased profitability and customer engagement.

Drivers of Growth in Bancassurance

a. Insuring Vehicles

The rise in vehicle ownership in Kenya has led to increased demand for motor insurance. According to recent statistics from the Kenya National Bureau of Statistics (KNBS), vehicle registrations have surged by over 20% annually. Banks are capitalizing on this trend by integrating motor insurance into vehicle financing packages, ensuring that borrowers are adequately insured while also protecting their loan investments.

b. Loans and Mortgages

As personal and business loans become more prevalent among Kenyans seeking financial support for various projects, insuring these loans has become essential. Banks offer loan-linked insurance policies that protect both the borrower and the lender from potential losses due to defaults or unforeseen circumstances such as death or disability. This integration not only safeguards the bank’s interests but also provides peace of mind for borrowers.

c. Digital Transformation

The digital revolution is reshaping how bancassurance operates in Kenya. Many banks are adopting technology-driven solutions that facilitate seamless integration between banking services and insurance products. Mobile banking applications now often include options for purchasing or managing insurance policies directly from users’ smartphones. This convenience is attracting tech-savvy customers who prefer managing their finances digitally.

d. Regulatory Environment

The regulatory framework surrounding bancassurance in Kenya has evolved to encourage collaboration between banks and insurers. The Insurance Regulatory Authority (IRA) has implemented guidelines that facilitate these partnerships while ensuring consumer protection. These regulations help create a conducive environment for bancassurance growth by establishing clear standards for product offerings and sales practices.

Case Studies: Successful Bancassurance Models in Kenya

Case Study 1: KCB Bank and its Insurance Offerings

KCB Bank has emerged as a leader in the bancassurance space in Kenya. Through its partnership with various insurance providers, KCB offers a wide range of products including life insurance, health coverage, and motor insurance. The bank’s approach focuses on integrating these offerings into its loan products—ensuring that customers are informed about relevant insurance options when they apply for financing.As a result of these initiatives, KCB has reported significant growth in its market share within the bancassurance sector. In 2023 alone, KCB’s bancassurance revenue increased by 25%, highlighting the effectiveness of this model in enhancing customer engagement and profitability.

Case Study 2: Equity Bank’s Innovative Insurance Products

Equity Bank has also successfully leveraged bancassurance to expand its service offerings. The bank collaborates with leading insurers to provide tailored products such as microinsurance aimed at low-income earners and smallholder farmers. By bundling these products with loans or savings accounts, Equity Bank has been able to attract new customers while retaining existing ones.This innovative approach has resulted in a notable increase in customer acquisition rates—particularly among underserved populations who previously lacked access to affordable insurance options.

Challenges Facing Bancassurance in Kenya

1. Customer Awareness and Education

Despite its growth potential, one of the significant challenges facing bancassurance is low customer awareness about available products. Many consumers do not fully understand how bancassurance works or the benefits it offers. Educational initiatives are crucial for increasing uptake among potential clients.

2. Competition from Traditional Insurance Channels

Traditional insurers view bancassurance as competition that threatens their market share. As banks continue to expand their presence in this space, traditional insurers may respond by enhancing their own distribution strategies or developing competitive products tailored specifically for direct sales.

3. Regulatory Hurdles

While regulations have generally supported bancassurance growth, changes in policy can present challenges for both banks and insurers. Adapting to new regulatory requirements can be resource-intensive and may slow down product development cycles.

Future Outlook for Bancassurance in Kenya

Trends Shaping the Future

The future of bancassurance in Kenya looks promising as more banks recognize its potential benefits. Predictions suggest that by 2025, bancassurance could account for up to 15% of the total insurance market share due to increasing consumer demand for integrated financial services.

Strategic Recommendations for Banks and Insurers

To maximize opportunities within this growing sector, it is essential for banks and insurers to collaborate closely on product development and marketing strategies. Joint training programs can help staff from both sectors understand each other’s offerings better—ultimately leading to improved customer service and satisfaction.

Conclusion

Bancassurance represents an exciting opportunity for both banks and insurers in Kenya as they work together to meet evolving consumer needs within an increasingly competitive landscape. By integrating banking services with comprehensive insurance offerings—particularly in areas like vehicle financing and loan protection—these institutions can enhance customer loyalty while driving revenue growth.

As awareness around bancassurance continues to grow among consumers and regulatory frameworks evolve to support this model further, it is clear that this partnership will play an integral role in shaping the future of financial services in Kenya.

FAQs about Bancassurance in Kenya

What is bancassurance?

Bancassurance is a partnership between banks and insurance companies that allows banks to sell insurance products alongside traditional banking services.

How does bancassurance benefit consumers?

It provides consumers with convenient access to various financial services under one roof while often offering competitive pricing on bundled products.

What types of insurance can be accessed through bancassurance?

Consumers can access various types of insurance through bancassurance including life insurance, health coverage, motor insurance, property insurance, and loan-linked policies.

Are there any risks associated with bancassurance?

Risks include potential conflicts of interest where banks may prioritize selling certain products over others based on profitability rather than consumer needs.

Microinsurance is a vital tool for smallholder farmers in Kenya, offering them a safety net against the unpredictable risks associated with agriculture. With agriculture and livestock contributing significantly to Kenya’s economy—accounting for about one-third of its annual output—farmers face increasing challenges due to climate change, market fluctuations, and natural disasters. Microinsurance products are designed to be affordable and accessible, providing essential coverage for farmers who often operate on tight budgets.

In this article, we will explore the various microinsurance products available for farmers in Kenya, their benefits, challenges, and how they can enhance financial security and resilience in the agricultural sector.

What is Microinsurance?

Definition of Microinsurance

Microinsurance refers to insurance products specifically designed to be affordable for low-income individuals or groups, particularly those who are often excluded from traditional insurance markets. Unlike conventional insurance, which may require high premiums and complex policies, microinsurance aims to provide simple, low-cost coverage that meets the unique needs of smallholder farmers.

Importance of Microinsurance for Farmers

Microinsurance plays a crucial role in enhancing financial security for farmers. It allows them to manage risks effectively and encourages them to invest in better agricultural practices and inputs. By mitigating the financial impact of crop failures or livestock losses, microinsurance helps stabilize farmers’ incomes and promotes sustainable agricultural practices.

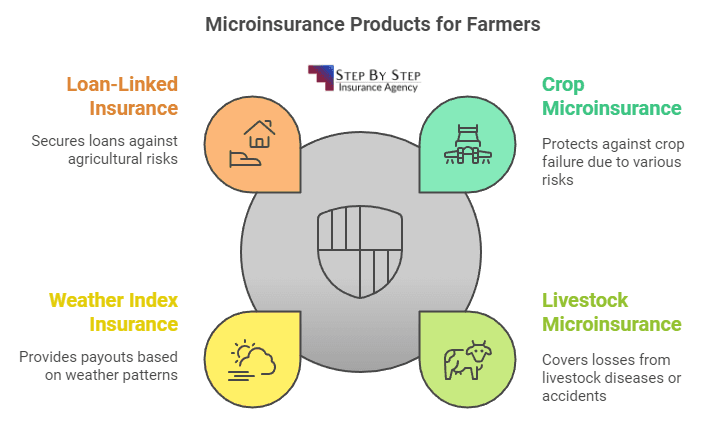

Types of Microinsurance Products Available for Farmers in Kenya

Microinsurance Products for Farmers

1. Crop Microinsurance

Crop microinsurance is tailored to protect farmers against losses due to adverse weather conditions, pests, and diseases. Notable products include:

Kilimo Salama: This program offers weather-indexed crop insurance that compensates farmers based on rainfall data rather than actual crop damage assessments. By using automated weather stations and mobile technology, Kilimo Salama has insured over 187,000 farmers since its inception.

Bima Pima: Translated as “insurance in affordable bits,” Bima Pima allows farmers to purchase scratch cards that provide insurance coverage when they buy seeds or fertilizers. The initial premium can be as low as KES 50 (approximately $0.50), making it accessible for many smallholders.

2. Livestock Microinsurance

Livestock microinsurance protects farmers from losses related to their animals due to diseases or accidents. Key offerings include:

Dairy Livestock Insurance: This product is designed for dairy farmers who supply milk to cooperatives. It covers losses due to illness or death of high-yield cows and is often bundled with veterinary services

.

Loan-Linked Insurance: This type of insurance is linked to loans taken by farmers for purchasing livestock. It ensures that if the farmer suffers a loss, the insurance covers the loan repayment, thus protecting both the farmer and the lending institution.

3. Weather Index Insurance

Weather index insurance is an innovative product that provides payouts based on specific weather conditions rather than actual losses. This type of insurance is particularly beneficial in areas prone to drought or excessive rainfall. Farmers receive compensation based on data collected from weather stations or satellite imagery. This approach reduces the need for costly loss verification processes.

4. Loan-Linked Insurance

Loan-linked insurance products are designed specifically for smallholders who have taken out loans for agricultural inputs. These products ensure that if a farmer suffers a loss due to adverse conditions, the insurance compensates them enough to cover their loan obligations.

Key Providers of Microinsurance in Kenya

a. ACRE Africa

ACRE Africa is one of the largest micro-insurance providers in Africa and plays a significant role in offering tailored solutions for Kenyan farmers. Their innovative approach includes using satellite data and mobile technology to assess risks and provide timely payouts.

b. Kilimo Salama

Kilimo Salama has been a pioneer in providing accessible crop insurance through its unique model that combines technology with traditional farming practices. By eliminating on-site inspections through automated weather data collection, Kilimo Salama has made it possible for more farmers to access insurance.

c. Pula Advisors

Pula Advisors focuses on bundling agricultural inputs with insurance products. They work closely with seed companies and other suppliers to offer free insurance coverage as part of their product offerings. This model not only protects farmers but also encourages them to invest in quality seeds and fertilizers.

Benefits of Microinsurance for Farmers

Microinsurance provides numerous advantages that can significantly impact smallholder farmers:

1. Financial Protection

Microinsurance acts as a safety net against unexpected losses. By providing compensation during adverse conditions, it helps stabilize farmers’ incomes and reduces vulnerability.

2. Increased Investment in Agriculture

With the assurance that they will be compensated for losses, farmers are more likely to invest in high-quality seeds, fertilizers, and modern farming techniques. This investment can lead to increased productivity and better yields.

3. Improved Food Security

By protecting farmers’ livelihoods, microinsurance contributes to overall food security within communities. When farmers can sustain their production levels despite challenges, it ensures a steady supply of food.

Challenges Facing Microinsurance Uptake in Kenya

Despite its benefits, several challenges hinder the widespread adoption of microinsurance among Kenyan farmers:

1. Awareness and Education

Many farmers are unaware of available microinsurance products or do not understand how they work. Education initiatives are crucial for increasing uptake.

2. Affordability Concerns

While microinsurance is designed to be affordable, some farmers still find it challenging to pay premiums due to their limited income.

3. Accessibility Issues

Geographic barriers can limit access to microinsurance products. Farmers in remote areas may struggle to find providers or may not have access to mobile technology necessary for purchasing policies.

How to Access Microinsurance Products in Kenya

Farmers interested in accessing microinsurance products can follow these steps:

Research Available Products: Start by researching different microinsurance options that suit your farming needs.

Contact Local Providers: Reach out to local agribusinesses or cooperatives that offer microinsurance.

Complete Necessary Documentation: Fill out any required forms and provide necessary information about your farm.

Pay Premiums: Make sure you understand the premium payment process—many providers allow payments through mobile money platforms.

Case Studies: Success Stories from Kenyan Farmers

Example 1: Jacob Wambua’s Dairy Farm Success

Jacob Wambua is a successful dairy farmer who has benefited significantly from taking up livestock microinsurance. Operating in Machakos County—a region prone to drought—Wambua faced numerous challenges due to climate variability. However, by enrolling in an insurance program offered through his cooperative, he was compensated when he lost cows due to disease. This financial support allowed him not only to recover but also expand his herd size and increase milk production.

“Insurance has given me peace of mind,” says Wambua. “I know I can invest confidently knowing I have protection against unforeseen events.”

Example 2: Impact of Bima Pima on Smallholder Farmers

Farmers using Bima Pima have reported substantial improvements in their farming outcomes. For instance, Mary Mate from Embu County shared her experience after receiving compensation through her Bima Pima policy when drought affected her crops. The quick payout allowed her to replant immediately, resulting in a successful harvest later that season.

Conclusion

Microinsurance products available for farmers in Kenya represent a transformative solution aimed at enhancing resilience against climate change and financial instability. By providing affordable coverage tailored specifically for smallholder needs, these products empower farmers like Jacob Wambua and Mary Mate to manage risks effectively while investing confidently in their agricultural practices.

As awareness grows around these innovative solutions, it is crucial for stakeholders—including government agencies, NGOs, and private sector players—to collaborate further in promoting microinsurance uptake among Kenyan farmers.

Maternity health insurance is a crucial aspect of healthcare coverage for expectant mothers in Kenya. As families prepare for the arrival of a new member, having the right insurance plan can ease financial burdens and ensure access to quality medical care.

This article will delve into the various maternity health insurance plans available in Kenya, their benefits, and essential considerations for selecting the best coverage.

The costs associated with maternity care can be significant, often ranging from KSh 50,000 to KSh 200,000 or more. This makes maternity health insurance not just a luxury but a necessity for many families. Understanding the specifics of what each plan offers is vital for making informed decisions that align with personal needs and circumstances.

What is Maternity Health Insurance?

Definition and Purpose

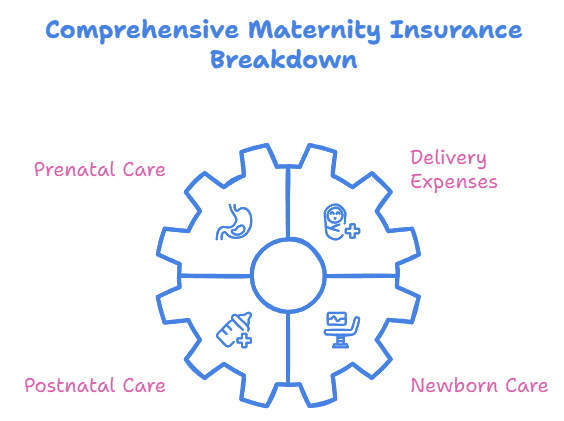

Maternity health insurance specifically provides financial support for medical expenses related to pregnancy and childbirth. This type of insurance typically covers a range of services, including prenatal care, delivery costs, postnatal care, and sometimes even newborn care. The primary purpose is to alleviate the financial burden associated with childbirth, allowing families to focus on welcoming their new child without the stress of unexpected medical expenses.

How It Differs from Regular Health Insurance

While standard health insurance plans may offer some coverage for maternity-related expenses, they often lack comprehensive maternity benefits. Maternity health insurance focuses on the unique needs of pregnant women, offering tailored coverage that includes:

Prenatal Visits: Regular check-ups and screenings during pregnancy.

Delivery Costs: Hospital stays, doctor fees, and surgical procedures (if necessary).

Postnatal Care: Follow-up visits and support after childbirth.

Newborn Care: Coverage for vaccinations and initial medical assessments.

In contrast, regular health insurance may impose waiting periods or limits on maternity coverage, making it essential for expectant mothers to seek out specific maternity plans that cater to their needs.

Why You Need Maternity Health Insurance in Kenya

Financial Protection

The financial implications of childbirth can be daunting. Without maternity health insurance, families may face significant out-of-pocket expenses that could lead to financial strain. Having a maternity health insurance plan helps mitigate these costs by covering most or all expenses related to pregnancy and childbirth. For instance:

Vaginal Delivery Costs: Typically covered under most plans.

Cesarean Section Costs: Often included but may require additional premiums.

Hospital Stay: Length of stay covered varies by plan.

Access to Quality Healthcare

Another critical reason for obtaining maternity health insurance is the access it provides to quality healthcare services. With an insurance plan in place, expectant mothers can choose healthcare providers and facilities that meet their standards without worrying about affordability. This access ensures that mothers receive appropriate prenatal care, which is vital for both maternal and fetal health.

Many maternity plans offer networks with reputable hospitals and specialists experienced in maternal care. This network can significantly enhance the quality of care received during pregnancy and delivery.

Types of Maternity Health Insurance Plans Available in Kenya

1. Comprehensive Maternity Plans

Comprehensive maternity plans offer extensive coverage for all aspects of maternity care. These plans typically include:

Unlimited prenatal visits

Coverage for both vaginal and cesarean deliveries

Extended postnatal care

Newborn care benefits

These plans are ideal for expectant mothers seeking thorough protection throughout their pregnancy journey.

comprehensive maternity coverage

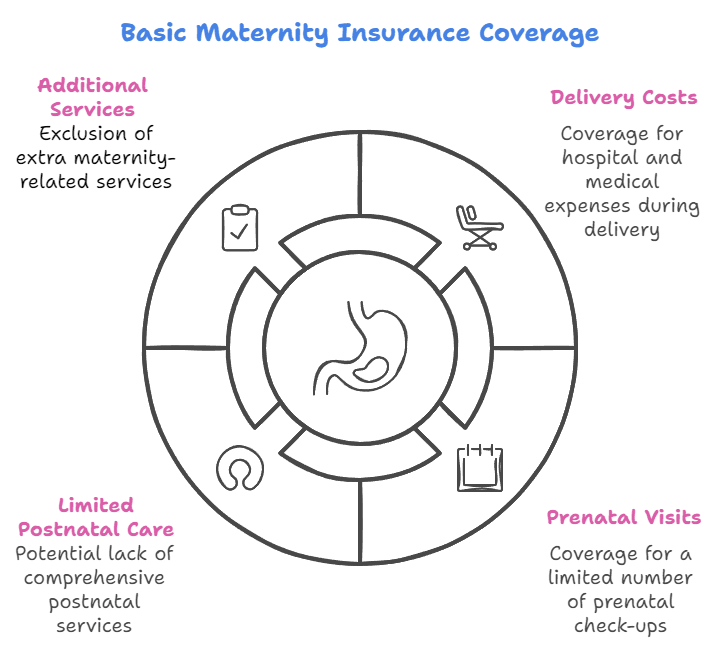

2. Basic Maternity Plans

Basic maternity insurance plans offer essential coverage for maternity-related expenses but may have limitations compared to comprehensive plans. These plans typically cover the costs of delivery and a few prenatal visits but may not include extensive postnatal care or additional services.

Basic Maternity Insurance Coverage

Features:

Coverage for hospital delivery

Limited prenatal visits

Basic postnatal care

Benefits:

More affordable premiums compared to comprehensive plans

Suitable for families with limited maternity care needs

While these plans are more affordable, they may not cover all potential expenses associated with childbirth.

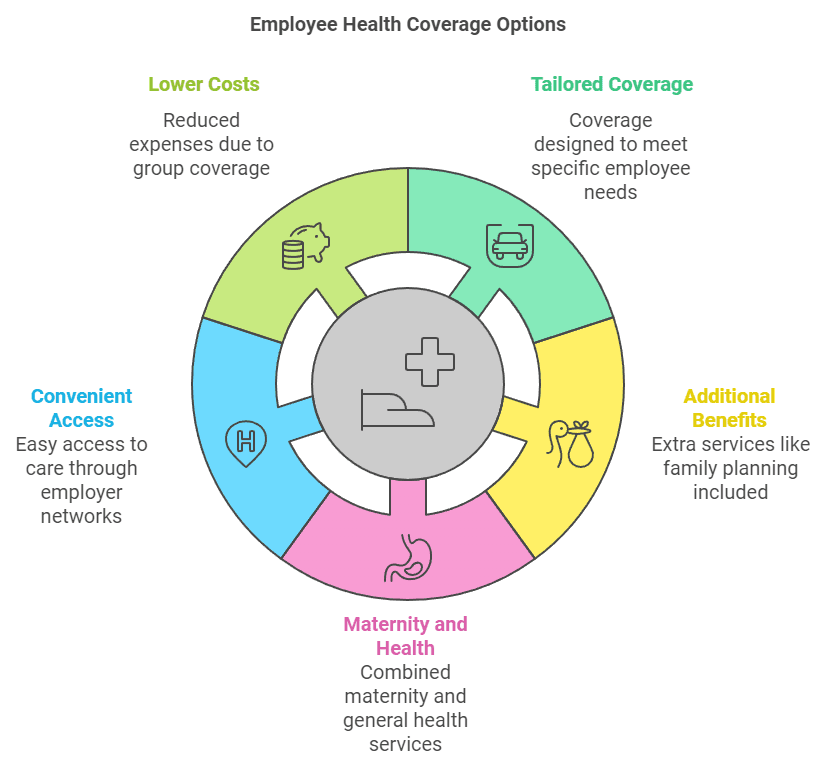

3. Employer-Sponsored Maternity Insurance

Many employers in Kenya offer maternity health insurance as part of their employee benefits package. These plans can vary significantly in terms of coverage and benefits. Employees should review their employer’s offerings carefully to understand what is included:

Coverage details (prenatal, delivery, postnatal)

Any waiting periods before benefits kick in

Whether dependents (newborns) are covered under the policy

Employee Sponsored Maternity Coverage Options